Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.S. Average Hourly Wage MoM (SA) (Dec)

U.S. Average Hourly Wage MoM (SA) (Dec)A:--

F: --

U.S. Average Weekly Working Hours (SA) (Dec)A:--

F: --

P: --

U.S. New Housing Starts Annualized MoM (SA) (Oct)A:--

F: --

U.S. Total Building Permits (SA) (Oct)A:--

F: --

P: --

U.S. Building Permits MoM (SA) (Oct)A:--

F: --

P: --

U.S. Annual New Housing Starts (SA) (Oct)A:--

F: --

U.S. U6 Unemployment Rate (SA) (Dec)A:--

F: --

P: --

U.S. Manufacturing Employment (SA) (Dec)A:--

F: --

U.S. Labor Force Participation Rate (SA) (Dec)A:--

F: --

P: --

U.S. Private Nonfarm Payrolls (SA) (Dec)A:--

F: --

U.S. Unemployment Rate (SA) (Dec)A:--

F: --

U.S. Nonfarm Payrolls (SA) (Dec)A:--

F: --

U.S. Average Hourly Wage YoY (Dec)A:--

F: --

Canada Full-time Employment (SA) (Dec)

Canada Full-time Employment (SA) (Dec)A:--

F: --

P: --

Canada Part-Time Employment (SA) (Dec)A:--

F: --

P: --

Canada Unemployment Rate (SA) (Dec)A:--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Dec)A:--

F: --

P: --

U.S. Government Employment (Dec)A:--

F: --

P: --

Canada Employment (SA) (Dec)A:--

F: --

P: --

U.S. UMich Consumer Expectations Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich Consumer Sentiment Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich Current Economic Conditions Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich 1-Year-Ahead Inflation Expectations Prelim (Jan)A:--

F: --

P: --

U.S. UMich 5-Year-Ahead Inflation Expectations Prelim YoY (Jan)A:--

F: --

P: --

U.S. 5-10 Year-Ahead Inflation Expectations (Jan)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Dec)

China, Mainland M1 Money Supply YoY (Dec)--

F: --

P: --

China, Mainland M0 Money Supply YoY (Dec)--

F: --

P: --

China, Mainland M2 Money Supply YoY (Dec)--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

Indonesia Retail Sales YoY (Nov)

Indonesia Retail Sales YoY (Nov)--

F: --

P: --

Euro Zone Sentix Investor Confidence Index (Jan)

Euro Zone Sentix Investor Confidence Index (Jan)--

F: --

P: --

India CPI YoY (Dec)

India CPI YoY (Dec)--

F: --

P: --

Germany Current Account (Not SA) (Nov)

Germany Current Account (Not SA) (Nov)--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

FOMC Member Barkin Speaks U.S. 3-Year Note Auction Yield--

F: --

P: --

U.S. 10-Year Note Auction Avg. Yield--

F: --

P: --

Japan Trade Balance (Customs Data) (SA) (Nov)

Japan Trade Balance (Customs Data) (SA) (Nov)--

F: --

P: --

Japan Trade Balance (Nov)--

F: --

P: --

U.K. BRC Overall Retail Sales YoY (Dec)

U.K. BRC Overall Retail Sales YoY (Dec)--

F: --

P: --

U.K. BRC Like-For-Like Retail Sales YoY (Dec)--

F: --

P: --

Turkey Retail Sales YoY (Nov)

Turkey Retail Sales YoY (Nov)--

F: --

P: --

U.S. NFIB Small Business Optimism Index (SA) (Dec)--

F: --

P: --

Brazil Services Growth YoY (Nov)

Brazil Services Growth YoY (Nov)--

F: --

P: --

Canada Building Permits MoM (SA) (Nov)--

F: --

P: --

U.S. CPI MoM (SA) (Dec)--

F: --

P: --

U.S. CPI YoY (Not SA) (Dec)--

F: --

P: --

U.S. Real Income MoM (SA) (Dec)--

F: --

P: --

U.S. CPI MoM (Not SA) (Dec)--

F: --

P: --

U.S. Core CPI (SA) (Dec)--

F: --

P: --

U.S. Core CPI YoY (Not SA) (Dec)--

F: --

P: --

U.S. Core CPI MoM (SA) (Dec)--

F: --

P: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. New Home Sales Annualized MoM (Oct)--

F: --

P: --

U.S. Annual Total New Home Sales (Oct)--

F: --

P: --

U.S. Cleveland Fed CPI MoM (SA) (Dec)--

F: --

P: --

China, Mainland Imports YoY (CNH) (Dec)--

F: --

P: --

China, Mainland Trade Balance (CNH) (Dec)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Trump's 'hard way' Greenland threat alarms allies, straining NATO relations amid Danish defiance and geopolitical concerns.

President Donald Trump has escalated his campaign to acquire Greenland, stating he is prepared to secure the Danish territory "the hard way" if a deal cannot be reached.

“I would like to make a deal, you know, the easy way. But if we don't do it the easy way, we're going to do it the hard way,” Trump told reporters at the White House on Friday.

The president's focus on Greenland, which he frames as a national security imperative, has sharpened following a recent U.S. raid targeting Venezuelan leader Nicolas Maduro. The move has heightened concerns among allies about the potential use of U.S. military force to achieve foreign policy objectives.

When asked about a potential financial offer for the island, Trump dismissed the idea for now.

"I'm not talking about money for Greenland yet," he said. "I might talk about that, but right now, we are going to do something on Greenland, whether they like it or not."

The president justified his stance by pointing to geopolitical competition with Russia and China, arguing that U.S. action is necessary to prevent them from establishing a presence in the region. “We’re not going to have Russia or China as a neighbor,” Trump stated.

The comments have strained relations with Denmark, a key NATO member. Danish Prime Minister Mette Frederiksen issued a stark warning, stating that a U.S. attack on Greenland would signify the end of the NATO alliance.

Other European leaders echoed this sentiment, calling on Trump to respect the island’s territorial integrity and affirming that it is protected under the bloc's collective security framework.

While the president has not ruled out using military force, the official U.S. position appears to be focused on a transaction.

On Tuesday, U.S. Secretary of State Marco Rubio told lawmakers that the administration’s goal is to buy the island. Rubio is scheduled to meet with Danish officials next week to discuss the matter.

The massive spending on artificial intelligence that drove stocks to record highs last year may not need an encore to keep the rally going. According to a report from BCA Research, potential interest rate cuts from the Federal Reserve could be enough to support tech stocks, even if AI infrastructure investment slows down.

This combination of lower rates and persistent inflation could delay or prevent a market crash reminiscent of the Dotcom Bubble.

America's largest tech companies—Microsoft, Alphabet, Amazon, Meta, and Oracle—are on track to spend over $500 billion on infrastructure this year, with a significant portion dedicated to AI.

According to Dhaval Joshi, chief strategist at BCA Research, this level of capital expenditure as a percentage of GDP is approaching a threshold that historically marked the peak of major tech investment cycles. Previous cycles include the personal computing boom of the 1980s, the dot-com boom of the 1990s, and the post-pandemic "Zoom boom."

In past cycles, tech stocks typically started to underperform the broader market about a year before capital spending peaked. If history repeats itself, Joshi noted, "AI-plays in the stock market are in imminent danger."

Despite historical parallels, the current environment may have more in common with the recent "Zoom boom" than the dot-com crash, primarily due to the Federal Reserve's monetary policy stance.

"Even if the AI capex boom ends, an ultra-accommodative Fed can prolong the stock market rally," Joshi wrote.

This matters because fears of slowing AI spending already caused tech stocks to hesitate in late 2025. The key difference lies in the behavior of real interest rates.

The Critical Role of Real Bond Yields

For stock valuations, what truly matters is not the nominal interest rate but the real bond yield—a bond's return after adjusting for inflation.

Joshi points out that the tech sector held its ground in 2021 because while inflation was rising, real bond yields continued to fall. Tech stocks only began to falter in 2022 when the Federal Reserve’s aggressive rate hikes sent real rates soaring.

Today, the situation is reversed. "Fast forward to today, and rate hikes are not on the Fed's agenda. Quite the contrary, the Fed is signalling more rate cuts," Joshi explained. If inflation remains around 3% while the central bank cuts rates, real yields would decline, providing crucial support for stock valuations.

Of course, an "ultra-accommodative" Fed is not guaranteed. Several factors could force policymakers to delay or limit rate cuts, including:

• Persistently sticky or resurgent inflation

• A surprisingly stable job market

• Robust overall economic growth

Following a mixed jobs report on Friday, the probability of the Fed holding rates steady through the first half of the year rose to a one-month high.

While most Wall Street analysts remain optimistic about the stock market's prospects for 2026, the sustainability of the AI rally is a primary concern. Mega-cap tech stocks now represent an unusually large portion of the S&P 500, making the entire index vulnerable to a downturn in the tech sector.

However, lower interest rates could also boost market liquidity, while tax cuts from last year's One Bi Beautiful Bill could stimulate economic growth, potentially offsetting any drag from a slowdown in tech investment.

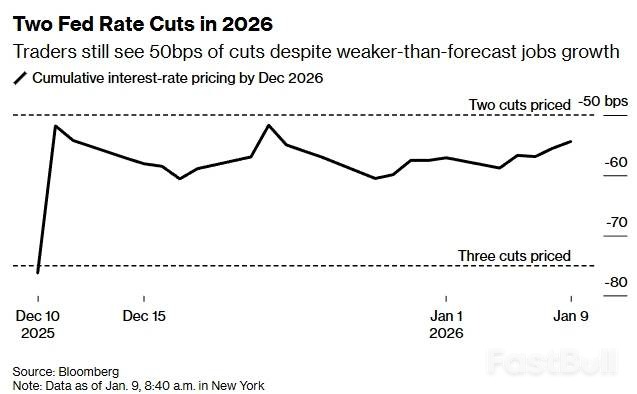

Wall Street is bracing for the Federal Reserve to continue cutting interest rates in 2026, with analysts now forecasting at least a 50 basis point reduction. The expectation comes as President Donald Trump prepares to name a successor to Fed Chair Jerome Powell, signaling a potential policy shift.

Leading financial institutions have revised their outlooks, anticipating a more aggressive easing cycle. According to recent client notes:

• Morgan Stanley now projects two 25-bps rate cuts in 2026, shifting its timeline from January and April to June and September.

• Citigroup has also adjusted its forecast, now expecting rate cuts in March, July, and September. This outlook implies a total reduction of up to 75 bps in 2026, which would push the federal funds rate range below 3%.

The market's dovish sentiment is building on the three rate cuts already anticipated for 2025. The primary driver is the expected appointment of a new Fed Chair by President Trump, which investors believe will lead to a more accommodative monetary policy.

This view is supported by officials like Treasury Secretary Scott Bessent, who has advocated for lower interest rates to stimulate economic growth, despite weaker-than-expected jobs data.

This macroeconomic environment is seen as highly favorable for digital assets. The expected rate cuts align with other expansionary policies, including the Federal Reserve's Quantitative Easing (QE) program that began in early December 2025 and a planned $200 billion injection into the housing industry by President Trump.

These dovish signals are prompting Wall Street investors to adopt a "risk-on" appetite. As the stock market continues its bull rally, a capital rotation away from precious metals and into riskier assets is expected. Consequently, Bitcoin and the wider altcoin industry appear poised to benefit, potentially triggering a strong bull run in 2026.

Despite the escalating war in Ukraine and shattered relations between Russia and the European Union, a small window for cooperation between Washington and Moscow appears to remain open. In a rare instance of de-escalation, the United States agreed to release Russian crew members from a tanker seized in a high-stakes naval operation.

The incident began when the United States intercepted the Russian-flagged oil tanker Marinera in the North Atlantic. The vessel is allegedly part of a "shadow fleet" used to transport oil for sanctioned nations like Venezuela, Russia, and Iran.

The seizure was a particularly bold move ordered by the Trump administration because the Marinera was reportedly being escorted by the Russian Navy, including a submarine. This direct action raised fears of a potential exchange of fire between US and Russian naval forces, creating a tense standoff on the high seas. The vessel, previously named Bella 1, had reportedly been reflagged from Guyanese to Russian before its journey across the Atlantic.

Instead of spiraling into a military conflict, the crisis was resolved through direct appeals. Russia’s Foreign Ministry spokeswoman, Maria Zakharova, confirmed that the Kremlin had reached out to the White House to secure the release of its citizens.

"At our request, U.S. President Donald Trump has decided to release two Russian citizens aboard the Marinera tanker, who were previously detained by the United States," Zakharova stated.

Kirill Dmitriev, a special envoy for President Putin, also noted on Telegram that Trump had ordered the release of "all Russians" from the vessel.

The Russian government expressed public appreciation for the decision. "We welcome this decision and express our gratitude to the US leadership," Zakharova added.

The release averted what could have become a serious international incident. Moscow had previously warned that any attempt to prosecute the Russian nationals would be "categorically unacceptable" and would "only result in further military and political tensions." The Kremlin voiced alarm over "Washington's willingness to generate acute international crisis situations."

By resolving the matter diplomatically, both sides stepped back from a potentially explosive confrontation, signaling that even in an environment of deep hostility, channels for communication and de-escalation between the US and Russia still exist.

Myanmar's military regime is staging fraudulent, tightly controlled elections across the country, even as its airstrikes continue to terrorize the population. The largest opposition party, the National League for Democracy (NLD), has been banned from participating. Yet, troubling signs suggest that some world governments, including the United States, may be preparing to re-engage with the junta.

This is a critical moment. For the Trump administration to overhaul its Myanmar policy now would be a strategic error, rewarding a military that controls less than half the nation's territory and granting it the political legitimacy it desperately craves.

Since the military coup in 2021 that ousted the democratically elected government of Aung San Suu Kyi, U.S. policy has centered on diplomatic isolation and targeted economic sanctions, often coordinated with allies like the UK, EU, and Canada. Now, that approach appears to be under review.

The first major signal of a shift came last November when U.S. Secretary of Homeland Security Kristi Noem announced the termination of Temporary Protected Status (TPS) for thousands of Burmese refugees in the U.S. Her justification was starkly disconnected from reality.

Noem declared that the "situation in Burma has improved enough that it is safe for Burmese citizens to return home," citing supposed progress in governance, stability, and national reconciliation. Human rights advocates found their requests for meetings with DHS officials turned down, with the department stating that current policy was "under review." In response, the Asian American Legal Defense and Education Fund (AALDEF) and the International Refugee Assistance Project (IRAP) have filed a lawsuit challenging the TPS revocation.

Further fueling concerns, the U.S. recently remained silent on International Human Rights Day, failing to join allies like Canada, Norway, and the United Kingdom in a joint statement calling for an end to violence against civilians in Myanmar. The administration has also refrained from commenting on the junta's multi-phase election process, citing a policy directive from Secretary of State Marco Rubio to avoid criticizing foreign elections, with notable exceptions for Latin America and Europe.

The administration's actions have left Myanmar observers questioning whether these are isolated decisions or part of a coherent strategy to court the country's generals.

Last summer, proposals were reportedly floated for U.S. investment in Myanmar’s rare-earth mining sector. While these plans went nowhere—China dominates the industry, sourcing 57% of its rare-earth imports from Myanmar—they raised concerns that the administration is open to engaging the junta when an opportunity arises.

The confusion deepened in July when President Trump sent a letter to junta leader Min Aung Hlaing, addressing him as "His Excellency," to announce a 40% tariff on Myanmar's exports. This tariff is among the highest the U.S. imposes globally. Instead of protesting, Min Aung Hlaing responded with an enthusiastic letter of his own, thanking Trump and requesting sanctions relief.

Just two weeks later, the U.S. Treasury Department quietly lifted sanctions on several businesses and individuals close to the military regime. While analysts familiar with the move described it as "technical, not political," the junta immediately celebrated it as a major diplomatic victory, using it in propaganda to portray the democratic resistance as a losing cause.

In one area, the U.S. has acted decisively. In late 2025, the Justice Department created a new Scam Center Strike Force, and Congress passed legislation to dismantle the massive cyberscam industry flourishing in Myanmar and its border regions. These scam centers cost Americans over $10 billion in 2024 alone, demonstrating that Washington can act forcefully when it perceives a direct threat.

However, the Myanmar military is not a reliable partner in this fight. Despite staging symbolic crackdowns on notorious sites like KK Park, the junta cannot be trusted as long as its own corrupt officers and high-level officials benefit from the illicit industry.

The Trump administration's National Security Strategy explicitly states its willingness to work with authoritarian countries if it serves U.S. interests. But in Myanmar, there is no clear upside.

• Economic Interests: It is virtually impossible for Washington to break Beijing's dominance over Myanmar's rare-earth supply chain.

• Shared Goals: The U.S. has no conceivable shared interests with the Tatmadaw, as Myanmar's military is known.

While neighboring countries like China, India, and Thailand maintain working relations with the junta for their own strategic reasons—from border stability and infrastructure security to counter-insurgency operations—their logic does not apply to the United States.

Arguments that Washington is losing influence to Beijing and must therefore engage the junta are short-sighted. A better strategy would be to support Myanmar's democratic resistance. When military rule eventually collapses, the U.S. will have retained the goodwill of the people, who remain deeply distrustful of China.

A peaceful, democratic Myanmar is a far more sustainable partner for the U.S. than a corrupt and unstable military regime. Instead of pivoting toward the generals in Naypyidaw, Washington should focus on the long game.

This means increasing support for Myanmar’s opposition and civil society leaders, who are the architects of the country's future democracy. It also requires expanding coordination with like-minded allies such as Australia, Canada, the EU, and the UK, who share U.S. concerns about regional and global security.

The junta's sham election will not solve Myanmar’s deep political divisions; it will only exacerbate them. Washington should ignore the political theater and instead lay the groundwork for a future where a democratic Myanmar can become a meaningful American partner in the Indo-Pacific.

U.S. President Donald Trump met with executives from the world's largest oil companies on Friday, January 9, to outline a strategy for Venezuela, stating that boosting the nation's crude production would directly benefit the United States.

The high-stakes meeting at the White House follows the seizure of Venezuelan leader Nicolas Maduro by U.S. forces during a raid on the capital on January 3, underscoring oil's central role in the administration's plan for the OPEC member.

President Trump opened the meeting by framing the objective clearly: leveraging American corporate power to quickly rebuild Venezuela’s failing oil industry. The goal, he stated, is to restore millions of barrels of production to the global market, benefiting the U.S., Venezuela, and the world.

"We're going to be making the decision as to which oil companies are going to go in, that we're going to allow to go in," Trump announced.

Administration officials have emphasized the need to control Venezuela's oil sales and revenue streams indefinitely to ensure the country's alignment with American interests. Central to this strategy is the expectation that major oil companies will inject billions of dollars into rehabilitating the nation's oilfields.

Despite the administration's clear intentions, a significant gap exists between Washington's ambitions and the risk appetite of major energy firms. Investors remain skeptical about committing to large-scale, long-term projects in Venezuela.

Key sources of hesitation for oil majors include:

• Political Instability: The uncertain political future of the country poses a major risk to long-term capital investments.

• High Costs: Rebuilding Venezuela's dilapidated energy infrastructure would require massive financial outlays.

While firms like Chevron, Vitol, and Trafigura are reportedly competing for U.S. licenses to market Venezuela's existing crude oil, this short-term opportunism does not extend to the deeper commitments the White House is seeking. According to sources, industry giants like Chevron and ConocoPhillips are cautious about rushing into major investments.

The meeting's guest list highlighted the administration's focus on mobilizing the entire U.S. energy sector. Attendees included not only industry leaders like Chevron, Exxon Mobil, and ConocoPhillips but also several smaller independent and private equity-backed players.

Notably, some of these smaller firms have connections to Colorado, the home state of Energy Secretary Chris Wright, suggesting a broad-based effort to bring American oil expertise to bear on Venezuela's future.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up