Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Japan's central bank signals further rate hikes, driven by a weak yen and inflation, navigating political pressure.

The Bank of Japan is poised to signal its willingness to raise interest rates again, driven by a falling yen and the prospect of solid wage growth that could fuel inflation. While an immediate rate change is unlikely, the central bank is expected to upgrade its growth forecast at its policy meeting concluding Friday.

All eyes will be on Governor Kazuo Ueda’s post-meeting press conference for hints about the timing of the next hike. The decision is complicated by rising bond yields and Prime Minister Sanae Takaichi’s recent call for a snap election in February, creating a delicate balancing act for policymakers. After raising interest rates to a 30-year high of 0.75% in December, the BOJ is expected to hold borrowing costs steady for now.

Prime Minister Takaichi’s political maneuvers have introduced a significant variable. On Monday, she announced proposals to cut Japan’s consumption tax and vowed to end what she called "excessively tight fiscal policy." Such expansionary fiscal measures could increase inflationary pressures, giving the BOJ another reason to tighten monetary policy.

However, a victory for Takaichi could also empower her reflationist advisers, who favor keeping rates low to support the fragile economy. This creates a complex political backdrop for the central bank.

"So far, the BOJ has maintained a negative stance toward consecutive rate hikes," noted Ayako Fujita, Japan chief economist at JPMorgan Securities, citing concerns over the financial system and pressure from Takaichi's administration. "Whether the recent yen depreciation will prompt a change in this stance is a key point to watch."

Japan’s financial markets are already feeling the strain. Concerns over the nation's finances have pushed the 10-year Japanese government bond yield to a 27-year high of 2.30% this week.

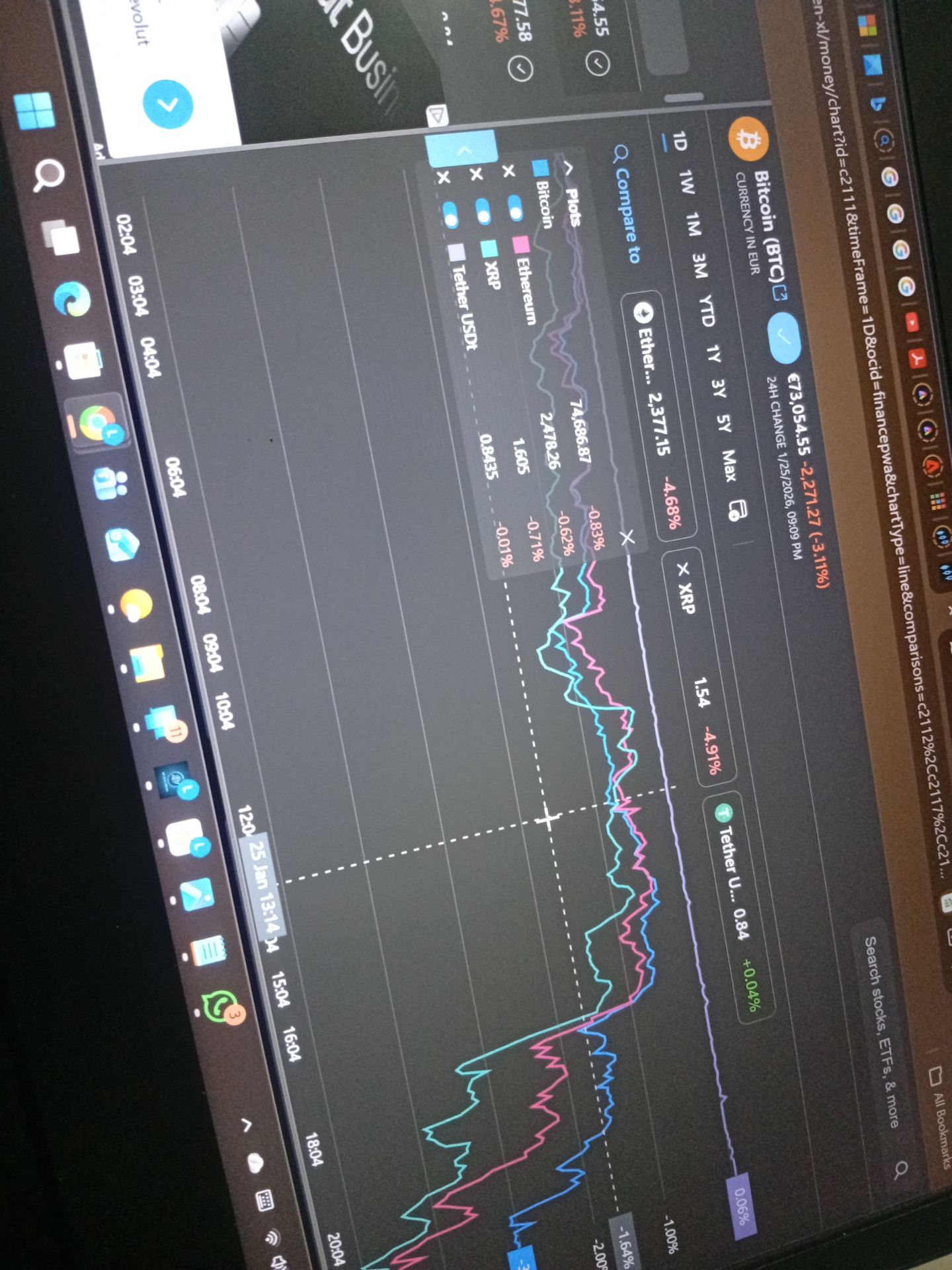

Meanwhile, the yen has weakened considerably since Takaichi became prime minister in October, falling about 8% against the dollar. It briefly hit an 18-month low of 159.45 last week, its weakest point since Japan’s last currency intervention in July 2024. Although it has since recovered slightly to around 158.18, the downward trend is raising import costs and contributing to broader consumer price increases. This has led markets to speculate that the BOJ may need to speed up its rate hike cycle to prevent inflation from overheating.

Internal discussions at the BOJ may be shifting. Sources have indicated that some policymakers see a case for raising rates sooner than markets anticipate, with April emerging as a distinct possibility. The primary driver for this view is the risk that a sliding yen will add to already broadening inflationary pressures.

This contrasts with the broader market consensus. A Reuters poll shows most analysts expect the BOJ to wait until July before hiking rates again, with over 75% forecasting the policy rate to reach 1% or higher by September. The central bank has moved methodically since ending its massive stimulus program in 2024, most recently lifting its short-term rate to 0.75% from 0.5% last month.

The BOJ's quarterly outlook report, due on Friday, is expected to reinforce the bank's growing conviction that conditions are aligning for further rate increases. Key updates are likely to include:

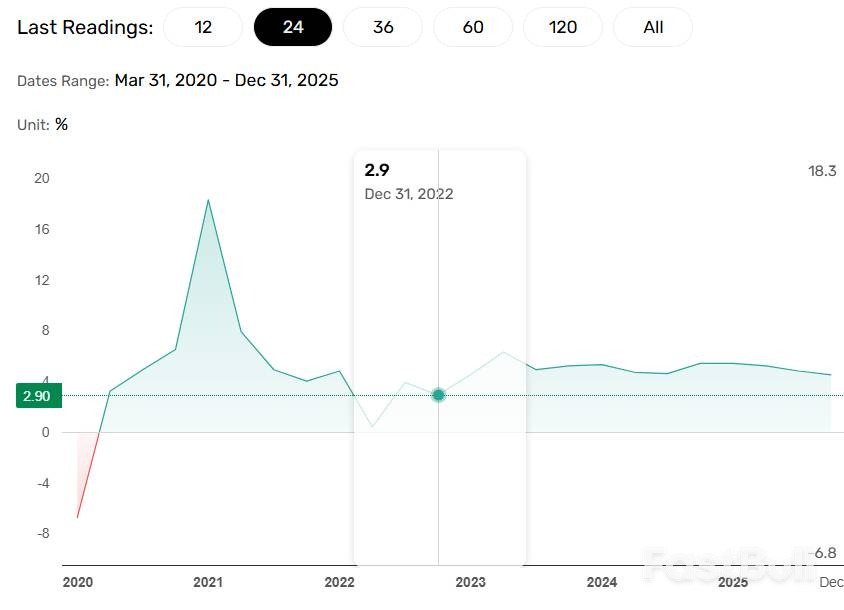

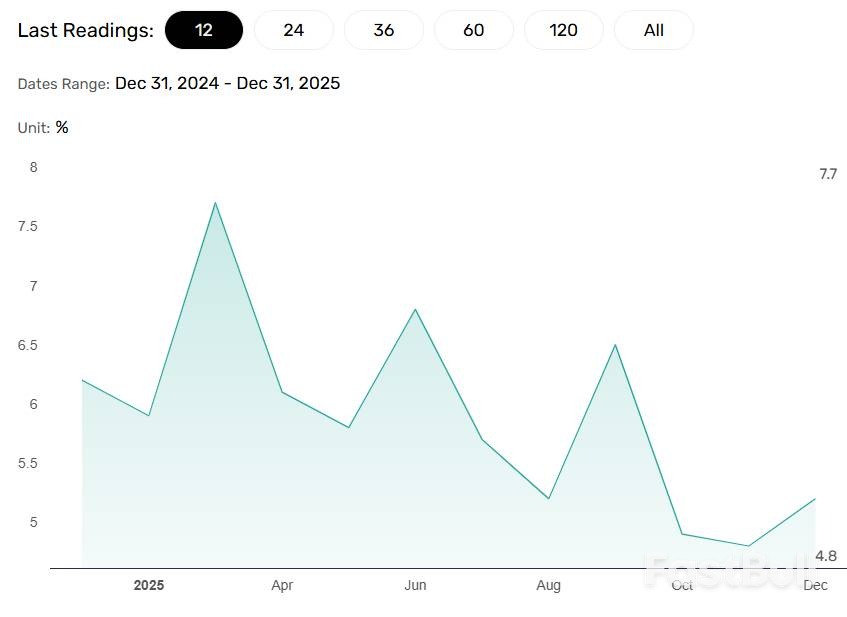

• Economic Growth: The forecast for fiscal 2026 is expected to be revised upward from the 0.7% growth projected three months ago. This reflects a boost from government stimulus and the fading impact of U.S. tariffs.

• Inflation: The core consumer inflation forecast for fiscal 2026 may be revised slightly higher from the 1.8% projected previously, as rising goods prices and steady wage gains offset government efforts to curb utility bills.

• 2% Target: The central bank is expected to maintain its projection that inflation will durably reach its 2% target around October, or in the latter half of the fiscal year beginning in April.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up

Price Forecast: Breakout Signals Strong Upside Continuation_1")

Price Forecast: Breakout Signals Strong Upside Continuation_2")