Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Trump's Greenland tariff threat pressures the dollar and raises political risk, reigniting de-dollarization debate.

The U.S. dollar is facing renewed pressure after President Donald Trump suggested imposing tariffs on European nations in connection with his proposal to acquire Greenland, injecting fresh uncertainty into U.S. policy.

The Bloomberg Dollar Spot Index registered a 0.1% decline in Asian trading following Trump's threat of a 10% tariff on European allies that support Denmark's sovereignty over the territory. Meanwhile, Treasury futures saw mixed trading while cash markets were closed for a U.S. holiday.

In response, European currencies gained ground. The Swiss franc outperformed other Group-of-10 currencies as investors sought out haven assets. The euro also climbed, recovering from its lowest point in nearly two months.

Trump’s tariff threats have revitalized the "sell America" trade, as investors begin to price in a higher political risk premium for U.S. assets. This dynamic could encourage foreign investors to scale back their exposure to the United States.

However, some market watchers are looking for a "TACO trade," speculating that Trump might be using the tariff threat as a negotiating tactic. If this proves to be the case, the dollar could find some temporary support.

While the prevailing market belief is that a deal over Greenland will eventually be reached, the involvement of national sovereignty raises concerns that the situation could escalate into a more dangerous conflict.

Analysts predict Europe will be among the biggest losers from rising geopolitical risks under a Trump presidency in 2026. The proposed tariffs could amplify cyclical headwinds for the eurozone economy. Furthermore, such a move could undermine pressure on Russia to conclude its war in Ukraine.

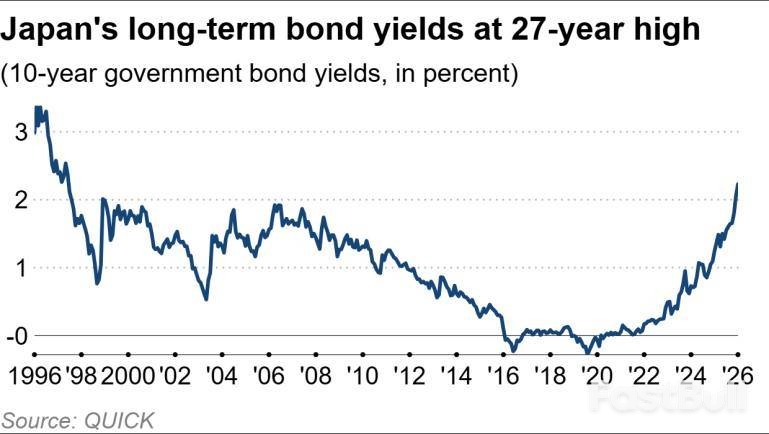

These shifting conditions are making European bonds a more attractive option for some investors, especially as the region's inflation indicators deteriorate amid escalating tensions between Europe and the U.S.

The geopolitical friction over Greenland has reignited the de-dollarization debate, highlighting the United States' large net international liabilities as a key economic vulnerability.

A renewed U.S. isolationist stance is contributing to some dollar weakness. However, analysts note that markets are becoming increasingly numb to tariff announcements, which could lead to more muted reactions in the future.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up