Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

France HICP Final MoM (Nov)

France HICP Final MoM (Nov)A:--

F: --

P: --

China, Mainland Outstanding Loans Growth YoY (Nov)

China, Mainland Outstanding Loans Growth YoY (Nov)A:--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)A:--

F: --

P: --

India CPI YoY (Nov)

India CPI YoY (Nov)A:--

F: --

P: --

India Deposit Gowth YoYA:--

F: --

P: --

Brazil Services Growth YoY (Oct)

Brazil Services Growth YoY (Oct)A:--

F: --

P: --

Mexico Industrial Output YoY (Oct)

Mexico Industrial Output YoY (Oct)A:--

F: --

P: --

Russia Trade Balance (Oct)

Russia Trade Balance (Oct)A:--

F: --

P: --

Philadelphia Fed President Henry Paulson delivers a speech

Philadelphia Fed President Henry Paulson delivers a speech Canada Building Permits MoM (SA) (Oct)

Canada Building Permits MoM (SA) (Oct)A:--

F: --

P: --

Canada Wholesale Sales YoY (Oct)A:--

F: --

P: --

Canada Wholesale Inventory MoM (Oct)A:--

F: --

P: --

Canada Wholesale Inventory YoY (Oct)A:--

F: --

P: --

Canada Wholesale Sales MoM (SA) (Oct)A:--

F: --

P: --

Germany Current Account (Not SA) (Oct)

Germany Current Account (Not SA) (Oct)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

Japan Tankan Small Manufacturing Outlook Index (Q4)

Japan Tankan Small Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)A:--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)

U.K. Rightmove House Price Index YoY (Dec)A:--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)A:--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)A:--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)--

F: --

P: --

Canada Existing Home Sales MoM (Nov)--

F: --

P: --

Euro Zone Total Reserve Assets (Nov)--

F: --

P: --

U.K. Inflation Rate Expectations--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

Canada New Housing Starts (Nov)--

F: --

P: --

U.S. NY Fed Manufacturing Employment Index (Dec)--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)--

F: --

P: --

Canada Core CPI YoY (Nov)--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)--

F: --

P: --

U.S. NY Fed Manufacturing Prices Received Index (Dec)--

F: --

P: --

U.S. NY Fed Manufacturing New Orders Index (Dec)--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)--

F: --

P: --

Canada Core CPI MoM (Nov)--

F: --

P: --

Canada Trimmed CPI YoY (SA) (Nov)--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)--

F: --

P: --

Canada CPI YoY (Nov)--

F: --

P: --

Canada CPI MoM (Nov)--

F: --

P: --

Canada CPI YoY (SA) (Nov)--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)--

F: --

P: --

Canada CPI MoM (SA) (Nov)--

F: --

P: --

Federal Reserve Board Governor Milan delivered a speech U.S. NAHB Housing Market Index (Dec)--

F: --

P: --

Australia Composite PMI Prelim (Dec)

Australia Composite PMI Prelim (Dec)--

F: --

P: --

Australia Services PMI Prelim (Dec)--

F: --

P: --

Australia Manufacturing PMI Prelim (Dec)--

F: --

P: --

Japan Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. Unemployment Claimant Count (Nov)--

F: --

P: --

U.K. Unemployment Rate (Nov)--

F: --

P: --

U.K. 3-Month ILO Unemployment Rate (Oct)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Switzerland has had productive talks with the US on the central bank’s currency interventions, Swiss National Bank President Mar...

Switzerland has had productive talks with the US on the central bank’s currency interventions, Swiss National Bank President Martin Schlegel said, rejecting the suggestion that the country manipulates the franc’s exchange rate.

“We are no currency manipulator,” he said in Lucerne on Friday, adding that “we had a constructive conversation with the US authorities” on the topic.

Schlegel declined to further elaborate on the format or content of those talks, though a spokesperson later said that the SNB has an ongoing exchange with US authorities, especially with the Department of the Treasury.

The central bank chief pointed out that historically, the SNB has only ever intervened on the franc to meets its price stability directive.

“We have never influenced the exchange rate to get us an advantage,” he said. “We only acted to ensure we fulfill our mandate under the given global economic conditions.”

The franc is typically seen as a haven currency in times of market stress, with the recent market uncertainty triggered by US President Donald Trump’s tariff policy pushing it to a decade high against the dollar last month and near such a high against the euro.

The SNB’s past interventions earned Switzerland a currency manipulator tag during Trump’s first term, though that label was subsequently removed. Schlegel has repeatedly said that the threat of that classification won’t stop the institution from steering the currency if required.

By selling some of its own reserves in foreign denominations, the SNB can strengthen the exchange rate. In 2022 and 2023, it boosted the franc in this way to dampen domestic inflation by making imported goods cheaper.

For several years before that, it had used the mechanism in the opposite direction to keep a lid on the currency. This has seen the SNB’s balance sheet grow to a size some observers deem dangerous as it can yield large profits — as last year — but also large losses.

The latest data show that the Swiss central bank hardly stepped into currency markets in 2024. First-quarter numbers will be available at the end of June.

The SNB is just a month away from its next monetary policy decision, with markets and economists expecting a 25 basis-point reduction to zero at that meeting. Asked if officials may have to embrace negative rates, Schlegel said that “if the economic situation dictates that the interest rate needs to be at that level, then we will go there.”

Nvidia (NVDA.O), opens new tab is seeking a site in Shanghai for a research and development centre, three sources close to the matter said, reflecting the strategic significance of the Chinese market where U.S. curbs on advanced chip exports have hit sales.

The U.S. chipmaker began the search in early 2025 and is primarily evaluating locations in Shanghai's Minhang and Xuhui districts, one of the sources said.

The project gained momentum after a surprise visit to China by Nvidia CEO Jensen Huang last month, said two of the sources.

Huang, who has consistently said China is critical to Nvidia's growth, made his visit immediately after the U.S. placed new restrictions on China-bound shipments of its H20 chips, the only AI chip the company can sell legally in China.

Huang met senior Chinese officials, including Vice Premier He Lifeng and Shanghai's mayor Gong Zheng.

Reuters reported earlier this month that Nvidia plans to release a downgraded version of the H20 chip for China in the next two months, as it seeks to prop up sales in the country, where it has been lost market share to domestic rivals such as Huawei.

China generated $17 billion in revenue for Nvidia in the fiscal year ending January 26, accounting for 13% of the company's total sales.

The local government of Shanghai, which hosts China's largest foreign business community, including firms such as Tesla (TSLA.O), opens new tab, has expressed willingness to offer incentives for the Nvidia project, including tax reductions, said two of the sources.

The local authorities are also considering offering a substantial amount of land to Nvidia for its China R&D centre, one source added.

Nvidia declined to comment, while the Shanghai city government did not immediately respond to a request for comment. The sources declined to be named, as the plan is not public.

Following his visit to China, Huang told CNBC that the country's AI market could reach approximately $50 billion within the next two-to-three years.

He said that being excluded from this rapidly expanding sector would represent a "tremendous loss" for Nvidia, especially as competition with Huawei intensifies.

During an earnings call in February, before H20 chip sales to China were restricted, Nvidia executives said the company's sales to China were about half the level before U.S. export controls.

Since 2022, the U.S. government has imposed restrictions on the export of Nvidia's most advanced chips to China, citing concerns over potential military applications.

The Financial Times first reported on Friday about Nvidia's plan to build a R&D centre in China.

Israeli strikes on Gaza have killed more than 250 people since Thursday morning, local health authorities said on Friday, one of the deadliest phases of bombardment since a truce collapsed in March and with a new ground offensive expected soon.

The air and artillery strikes were focused on the northern section of the tiny, crowded enclave, where dozens of people including women and children were killed overnight, said Gaza Health Ministry spokesman Khalil al-Deqran.

Israel has intensified its bombardment and built-up armour along the border despite growing international pressure for it to resume ceasefire talks and end its blockade of Gaza, where an international hunger monitor has warned of famine.

U.S. President Donald Trump on Friday backed aid for the Palestinians, saying people in Gaza are starving and adding that he expected "a lot of good things" in the next month.

Asked whether he supported Israeli plans to expand the war in Gaza, Trump told reporters: "I think a lot of good things are going to happen over the next month, and we're going to see. We have to help also out the Palestinians. You know, a lot of people are starving on Gaza, so we have to look at both sides."

Prime Minister Benjamin Netanyahu said on May 5 that Israel was planning an expanded and intensive offensive against Hamas as his security cabinet approved plans that could involve seizing the entire Gaza Strip and controlling aid.

An Israeli defence official said at the time that the operation would not be launched before Trump concluded his visit to the Middle East, which is expected to end on Friday.

Israel's declared goal in Gaza is the elimination of Hamas, which attacked Israeli communities on October 7, 2023, killing around 1,200 people and seizing about 250 hostages.

Its military campaign has devastated the enclave, pushing nearly all inhabitants from their homes and killing more than 53,000 people according to Gaza health authorities, while aid agencies say its blockade has caused a humanitarian crisis.

Heavy strikes on Friday were reported in the northern town of Beit Lahiya and in the Jabalia refugee camp, where Palestinian emergency services said many bodies were still buried in the rubble.

Israel's military said its air force had struck more than 150 targets across Gaza, saying these included anti-tank missile posts, terrorist cells, military structures and operational centres.

In Jabalia camp in the northern Gaza Strip, men picked through a sea of rubble following the night's strikes, pulling out sheets of metal as small children clambered through the debris.

Around 10 bodies draped in white sheets were lined up on the ground before being taken to hospital. Women sat crying nearby and one lifted a corner of a sheet to gaze at the dead person's face.

Ismail, a man from Gaza City who gave only his first name, described a night of horror. "The non-stop explosions resulting from the airstrikes and tank shelling reminded us of the early days of the war. The ground didn't stop shaking underneath our feet," Ismail told Reuters via a chat app.

"We thought Trump arrived to save us, but it seems Netanyahu doesn't care, neither does Trump," he added.

Israel has faced increasing international isolation over its campaign in Gaza, with even the United States, its staunchest ally, expressing unease over the scale of the destruction and the dire situation caused by its blockade on the delivery of food and other vital aid.

On Thursday, U.S. Secretary of State Marco Rubio said Washington was "troubled" by the humanitarian situation in the enclave.

Netanyahu has dispatched a team to Doha to take part in ceasefire talks with Qatari mediators but he has ruled out concessions, saying Israel remains committed to defeating Hamas.

The Hostages and Missing Families Forum, which represents some of the families and supporters of the 58 hostages still held in Gaza, said that Israel risked missing a "historic opportunity" to bring them home as Trump wound up his visit to the Middle East.

"We are in dramatic hours that will determine the future of our loved ones, the future of Israeli society, and the future of the Middle East," the group said in a statement.

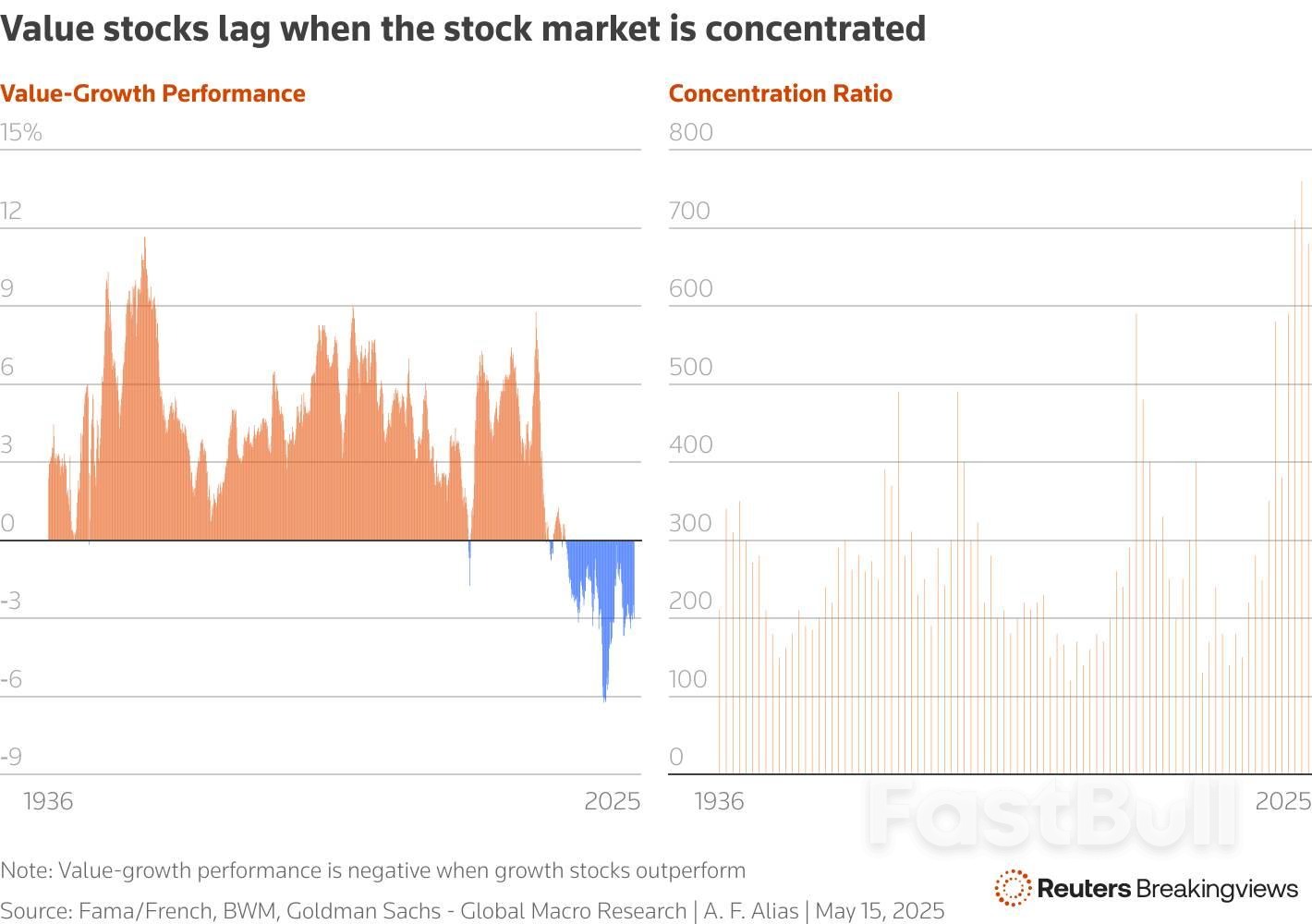

Warren Buffett, the greatest investor of all time, has announced his retirement. Fellow value investors are in a state of shock. Unfortunately, they have more serious problems to consider. For years, their favoured investment style has been out of fashion. Clients have lost patience. In a world in which the U.S. stock market index has delivered consistently outsized returns, low-cost funds that passively track an index seem a no-brainer. Yet the prospects for value investors have always been always brightest when the rest of the world loses faith.

Over the very long run, buying equities at relatively cheap valuations has worked out well. Economists Eugene Fama and Ken French define value as a low ratio of share price to book value. Using this measure, U.S. value stocks have beaten growth stocks, which have high price-to-book ratios, by 2.5% a year since 1926. Value has also outperformed in most other overseas markets, according to the UBS Global Investment Returns Yearbook compiled by Elroy Dimson, Paul Marsh and Mike Staunton. Its luck ran out, however, on the eve of the global financial crisis. Between 2007 and 2020, growth beat value. The latter recovered some ground in 2020 but fell back again after the “Magnificent Seven” big technology stocks took off in late 2022.

It is important to note that price to book is not the metric contemporary value investors rely upon. Warren Buffett’s partner, the late Charlie Munger, taught him to consider a firm’s competitive position – what the Oracle of Omaha called the “moat.” If a business consistently earns above average returns on capital, investors can safely buy its shares at a premium multiple to the rest of the market. Furthermore, the balance sheet value of a company’s assets is not a reliable measure of value, since it excludes many intangible assets such as research and development. Share buybacks and acquisitions further distort accounting book value.

Still, there are other investment oddities to consider. Small-cap stocks, which historically have beaten larger rivals and provide a favourite hunting ground for value investors, have also had a dismal run. Global stock markets, both the developed and emerging variety, have been trounced by the extraordinary performance of U.S. stocks. Between 2010 and the start of this year, American equities had delivered annualised returns of 10% after inflation, according to UBS. Over the same period, the other stock markets have collectively returned 2.6% a year after inflation. Emerging markets returned just half that figure. Howard Marks, the veteran value investor and co-chairman of Oaktree Capital Management, laments that “all norms have been overturned.”

The hard times for value investing can be explained by various factors. First, ultra-low interest rates after the global financial crisis increased the appeal of growth stocks whose profits lie in the distant future. Higher-yielding value stocks were relatively disadvantaged.

Second, value investors have suffered from the rapid expansion of index investing. Nearly 60% of the U.S. stock market is currently held by funds that passively track a benchmark. Goldman Sachs forecasts that between 2014 and 2026 the cumulative outflows from U.S. actively managed equity mutual funds into passive vehicles will reach around $3 trillion. As indexation advances, investors dump the value and small-cap stocks owned by traditional fund managers in favour of the S&P 500 Index (.SPX), opens new tab, which is heavily weighted towards larger and more expensive stocks.

The United States is home to the largest and most profitable companies the world has ever seen. The outsized returns of the Magnificent Seven over the last decade have depressed the relative returns of both value stocks and small caps. By the end of last year, the U.S. stock market had become more concentrated than at any time since the 1930s. Georg von Wyss, a portfolio manager at Zurich-based firm BWM, observes that in the past periods of extreme market concentration have been accompanied by the underperformance of value stocks. This was the case during the “Nifty Fifty” boom of the early 1970s and again in the technology bubble of the late 1990s.

Towards the end of that craze, value stocks were exceedingly cheap relative to the overall market. Clients closed their accounts with underperforming investment firms. Several well-known value managers were either fired or took early retirement. Warren Buffett, who didn’t partake in the market frenzy, was deemed to have lost the plot. But when the boom turned to bust and market concentration declined, as it did in 1975 and 2000, value stocks outperformed for years. Could value investors be on the verge of yet another winning streak?

The turmoil of the early months of Donald Trump’s second term may signal such a shift. At the London Value Investor Conference on Wednesday Richard Oldfield of Oldfield Partners said that the new U.S. administration, with its on-off threat of tariffs and hostile rhetoric to erstwhile allies, poses a risk to trend of “American exceptionalism”. Sensing the loss of U.S. support, Germany is borrowing to invest in defence and infrastructure. If capital flows to the United States start to reverse, developed and emerging stock markets stand to benefit. Value rallies have repeatedly petered out in recent years but, says Oldfield, “this time is different.”

Other headwinds that have buffeted value investors over the past decade may also be about to disperse. Over the past three years, interest rates have returned to more normal levels. The Magnificent Seven are currently locked in an arms race to invest in artificial intelligence. Time will tell whether their vast capital spending delivers an adequate return. These megacap growth stocks have underperformed in the year to date. Meanwhile, value and small-cap stocks in the United States and elsewhere offer exceptional opportunities.

Last year, David Einhorn of Greenlight Capital pronounced that value was “dead, opens new tab”. Another speaker at the London conference, Alissa Corcoran of Kopernik Global Investors refutes this claim. Value investing is immortal, she says. As index funds absorb a greater share of the world’s stock market, fundamental investors are still needed to perform the vital role of price discovery. Ideally, such investors would exhibit a patient, long-term approach and not be swayed by the herd. They should be careful stewards of their clients’ capital, and, above all, be endowed with common sense. Warren Buffett displayed these virtues to an uncommon degree. He will be missed. But there are legions of value investors ready to fill the void.

In a recent column, I argued that US managers have much to learn from emerging markets. Today, I want to add that managers everywhere have much to learn from the interwar years.

The interwar period — marked by the turmoil of the 1920s and the depression of the 1930s — was the last great period of deglobalization. The century between the defeat of Napoleon in 1815 and the outbreak of the First World War in 1914 was an era of pell-mell globalization. International trade grew by 3.5% a year. The gaps in commodity prices between continents declined by four-fifths. Sixty million Europeans migrated to the US. In 1913, foreign direct investment was 9% of world output, a proportion that wasn’t equaled until the 1990s.

The interwar years replaced seemingly unstoppable globalization with seemingly unstoppable deglobalization. The US had never shared Britain’s cast-iron commitment to free trade — in 1870 America, tariffs of 50% were common — but between the wars, protectionism became rampant. Governments not only increased and extended tariffs but also put a near halt to immigration. The annual migration rate to the US fell from 11.6 immigrants per thousand in the first decade of the 20th century to 0.4 per thousand in the 1940s.

European countries responded with tariffs of their own. Governments abandoned gold and imposed currency controls. The Mexican government nationalized foreign oil companies. By the late 1930s, half the world’s trade was restricted by tariffs, and the world was divided into currency blocs. Deglobalization gathered momentum despite the emergence of new technologies such as airplanes, automobiles, telephones, and ocean liners that were relentlessly killing distance.

Multinationals adopted three main strategies to cope with this world of deglobalization and political instability.

The first was to jump over tariff barriers and currency restrictions by establishing powerful foreign subsidiaries. American companies led the way partly because they were so well managed and partly because the US government made life so difficult for foreign companies, particularly banks.

This produced paradoxical results. The number of multinationals increased even as the world fragmented. But successful multinationals put down deep global roots. “The national autonomy of subsidiaries grew as they were closer to the local market and local politicians,” says Geoffrey Jones, a professor at Harvard Business School and author of Multinationals and Global Capitalism. “They unwound global supply chains and produced more stuff locally.” General Motors purchased Opel, one of Germany’s 10 largest industrial companies, and Vauxhall, a smaller British company, and employed local managers to run them. American Home Products, a giant US pharmaceuticals company, rolled up several smaller British firms. Coca-Cola sponsored the 1936 Olympic Games in Berlin.

The second was to use institutional innovation to compensate for political turbulence. Many companies coped with the most obvious downsides of fragmentation, falling demand and unpredictable supply, by either consolidation or coordination. Giant new companies such as Germany’s IG Farben and the UK’s Imperial Chemical Industries in chemicals, Unilever (a merger of Dutch margarine producer Unie with the British soap maker Lever Brothers) in consumer goods and Shell in petrol formed from the merger of smaller companies. Cartels appeared in a wide range of markets (tea, tin, coffee, gold and diamonds, electric lights and matches) either to control prices or divvy up the world into separate spheres. Cartelization produced some of the world’s most powerful companies, such as the Anglo-American Corporation and De Beers in South Africa, and some of its most enduring price-fixing arrangements, such as the Tin Producers Association, which was started in 1929 and only wound up in 1985. The Swiss-registered Electric Light Consortium controlled three-quarters of the global supply of electric lights and was itself controlled from behind the scenes by America’s General Electric, which wasn’t even a member.

Others adopted a new institutional form: the multidivisional firm or “M form” for short. General Motors pioneered the M form under Alfred Sloan’s leadership as a way of coping with the fragmentation of the consumer market: Powerful product managers were given control of producing different models for different consumer markets (Cadillac for the rich and so on down the income pyramid). But that approach turned out to be equally appropriate for a fragmenting geographical market. Both US and German behemoths began devolving enormous operational power to regional managers and restricting the headquarters to producing broad strategic plans.

The third was to treat regional fragmentation as a business opportunity rather than as a barrier to global ambitions. British companies such as Cadbury’s in chocolate and Dunlop in rubber focused on securing supplies and markets across the British Empire and the wider Commonwealth. Barclays purchased banks across Africa. Ford purchased a rubber plantation in Brazil and the United Fruit Company tightened its grip on South American bananas. State-allied oil companies such as Britain’s Anglo-Persian and America’s Standard Oil battled for control of supplies in the disputed Middle East, with plenty of help from the secret services.

Harvard’s Jones is struck by the similarity between today and the 1930s, with technologies working to bring the world together and policy makers and parts of the electorate pushing in the opposite direction. “The first lesson of history,” he says, “is that politics always matters more than technology in the direction of travel.” This means, in my view, that companies would be wise to abandon their “one world” strategies from the heady years of globalization and instead reorganize themselves into federations of national firms that can respond to local circumstances and, if necessary, pretend to be local companies. They also need to embrace anything from mergers to alliances that will give them the bulk to deal with collapses in demand or interruptions in supply: The more unpredictable markets become, the more companies need to do things internally.

But these years contain some powerful moral as well as practical lessons. CEOs can’t be expected to sacrifice their businesses to defend social or political causes of the day far outside their realm of operations. But there are limits to what they ought to tolerate. Some of America’s most successful companies placed no limits on how far they would go to get German business in the 1930s. General Motors’ Opel produced trucks for the Nazi war machine; IBM worked so closely with the Nazi regime that its boss, Thomas J. Watson Sr., was awarded the Order of the German Eagle in 1937. CEOs will be judged by their investors on how well they adapt to a rapidly deglobalizing world, but they will also be judged by history if they lose their moral compass in order to bow to the will of autocrats and scoundrels.

Ether's ETH$2,616.44 rally, though impressive, leaves much to be desired. That's because the unwinding of shorts is said to be fueling the rally, not fresh longs or bullish leveraged bets on the Chicago Mercantile Exchange (CME).

"The rally is primarily the result of short covering – traders unwinding bearish positions – rather than a surge of bullish conviction," Sui Chung, CEO of crypto index provider CF Benchmarks, told CoinDesk. CME's derivatives, preferred by institutions, track the CF Benchmarks' Bitcoin Reference Rate – New York (BRRNY) variant.

When bears cover their shorts, it means they are buying back futures contracts initially sold. This action of short covering temporarily boosts demand in the market, putting upward pressure on prices.

Chung pointed to the still-low CME futures premium (basis) as evidence that the rally is led by short covering.

While ether's spot price has surged nearly 90% to above $2,600 since the early April sell-off, the annualized one-month basis in the CME's ether has held flat between 6% and 10%, according to data source Velo.

"In more conventional setups, we would expect rising basis levels if traders were initiating fresh longs with leverage," Chung noted. "It's a reminder that not all rallies are fueled by new demand; sometimes, they reflect repositioning and risk reduction."

One might argue that the basis has held steady due to sophisticated trades "arbing" away the price difference between the CME ETH futures and the spot index price by shorting futures and buying ETH spot ETFs.

That argument looks weak when considering the U.S.-listed spot ETFs have seen net positive inflows on just ten trading days in the past four weeks. Besides, net inflows tallied over $100 million just once, according to the data source SoSoValue.

"The lack of inflows into ETH ETFs and the muted basis paints a different picture, this latest move higher doesn't appear to be driven by new leveraged longs," Chung said.

Key points in this update:

Global financial markets responded very enthusiastically this past week to news that the US and China had agreed to a 90-day pause in their escalating trade war, for now reducing punitive tariffs that were beginning to hurt both economies, threatening a recession in the US and a slowdown in China’s export-driven economy. This de-escalation provided what may still turn out to be temporary relief to markets, with global equity markets and pro-cyclical commodities staging a comeback while haven demand for gold faded.

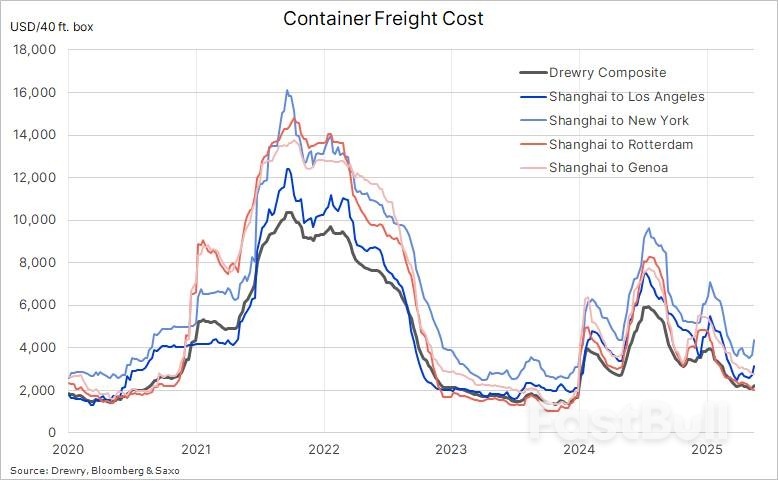

The announcement of a 90-day truce in trade tensions prompted a swift and strong reaction from the global shipping industry. The Drewry Global Container Index—a key benchmark that tracks weekly freight rates for container shipping across major international routes showed a jump in the Shanghai–Los Angeles and Shanghai–New York lanes by 15.6% and 19.3%, respectively. The notable rebound on these routes reflects a renewed wave of frontloading activity, as exporters and importers in both China and the United States rush to ship goods ahead of any potential re-escalation of tariffs once the truce expires. Yet, the overall index remains down around 40% this year amid rising container capacity and tariff threats to global trade.

Drewry Global Container Freight Indices

Drewry Global Container Freight IndicesThe risk-on rally saw the tech-heavy Nasdaq reach February levels, reversing most of its tariff-related weakness, while USD bears were challenged and US Treasury yields, especially at the long end, rose to levels that raised a few eyebrows, not least considering an urgent need to bring down funding costs to service a growing fiscal deficit. Economic data in the US showed the first albeit small signs of what may come in the coming months as tariffs start to impact consumers. While prices paid to US producers unexpectedly declined by the most in five years, suggesting companies, for now, are absorbing some of the hit from higher tariffs. Separate data for April showed growth in retail sales decelerated while factory production declined for the first time in six months, and confidence fell for a third month.

All signs indicate that the near-term economic outlook, not only in the US but also abroad—note Japan’s economy shrank for the first time in a year—remains challenged and vulnerable even before sustaining the full impact of Trump’s tariff measures. With this in mind, the prospect for additional dollar gains remains limited while the next rate cut from the US Federal Reserve is not a question of if but when they will cut next time; note the market is currently pricing in fully two 25-basis point cuts this year, followed by another two next year.

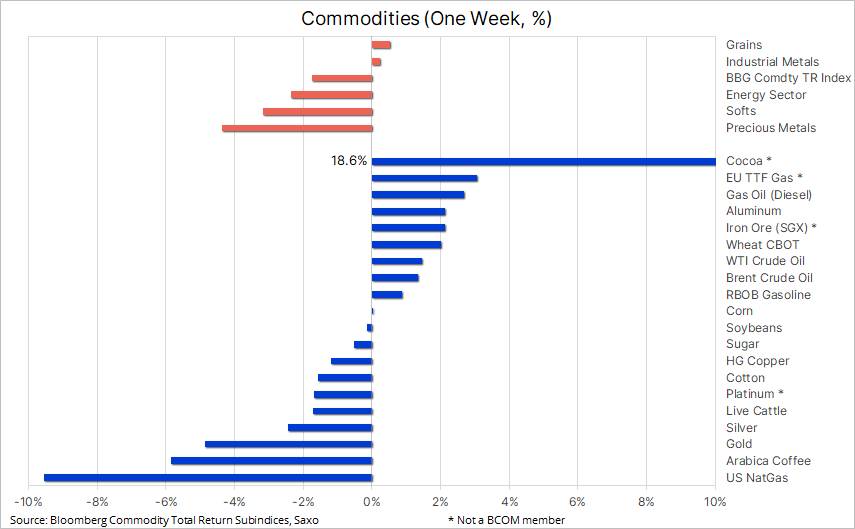

Overall, the trade truce initially gave pro-cyclical commodities, such as energy and industrial metals a boost, before fading amid economic data weakness, leading the Bloomberg Commodity Index towards a weekly loss around 1.8%, lowering the year-to-date gain to 3.8%. Weighing on the index which tracks a basket of 24 major commodities futures spread almost evenly between energy, metals and agricultural, were a steep 9.6% loss in natural gas, and 5% drop in gold, two commodities that together with Arabica coffee (-6%) accounts for around 25% of the index. At the other end of the spectre, cocoa – a non-BCOM member - surged higher almost 19% and back above USD 11,000 tons amid renewed concerns about the quality and size of the current crop being harvested in West Africa.

Key commodities: one week performances

Key commodities: one week performancesGold has experienced its sharpest correction—both in absolute and percentage terms—since 2023, breaking through multiple technical support levels. The initial trigger was a fading of safe-haven demand following the US-China 90-day trade truce. However, prices have since found renewed support amid a weakening dollar and falling bond yields, driven by a batch of softer-than-expected U.S. economic data.

Having already hit our 2025 price target of USD 3,500, we are currently adopting a wait-and-see approach. The market remains caught between profit-taking from those selling into strength and renewed interest from dip buyers. Despite the recent pullback, several key structural drivers—including central bank buying, geopolitical risks, fiscal debt concerns, and inflation hedging—remain intact. These are likely to underpin prices over the longer term, though a period of consolidation may be required before the next significant upside catalyst emerges.

Investor flows will be critical to watch going forward, particularly in China, where demand from retail investors through yuan-denominated ETFs has been a key source of support before recently fading. In contrast, Western-based ETF holdings have seen net outflows since late April, contributing to the softer price environment. Meanwhile, speculative positioning in COMEX futures has turned increasingly bearish, with managed money and other reportables reducing their net long exposure by 42% over the past seven weeks. This highlights the need for a fresh technical breakout or macro catalyst to entice these key participants back to the buy side.

While gold fell sharply, silver and platinum also declined but were partially shielded by their industrial use cases. Optimism around U.S.-China trade relations has lent support to growth-sensitive commodities, tempering the downside in these two metals. The gold-silver ratio has since pulled back below 100, after spiking above 105 in early April.

Platinum has underperformed both on a relative and absolute basis over the past decade. Once at parity with gold, it now trades at a ratio of 3.2:1, while its average price of USD 955 per oz over the past 17 years is just below current levels. This underperformance comes despite three consecutive years of structural deficits. According to Johnson Matthey, primary supply is expected to fall by 3% in 2025 to 5.54 million troy ounces, while demand is seen slipping 2.6% to 7.66 million ounces. Yet investment flows remain weak amid macroeconomic uncertainty, trade risks, and a softening outlook for the automotive sector, platinum’s largest demand driver.

Platinum remains trapped in a narrowing technical range. A breakout could provide the spark for renewed speculative interest. Until then, COMEX-managed money accounts remain largely neutral. We are closely watching USD 1,010 as near-term resistance and USD 1,025 as the more significant downtrend level stemming from the 2008 highs.

Spot Platinum (XPTUSD) - Source: SaxoTraderGO

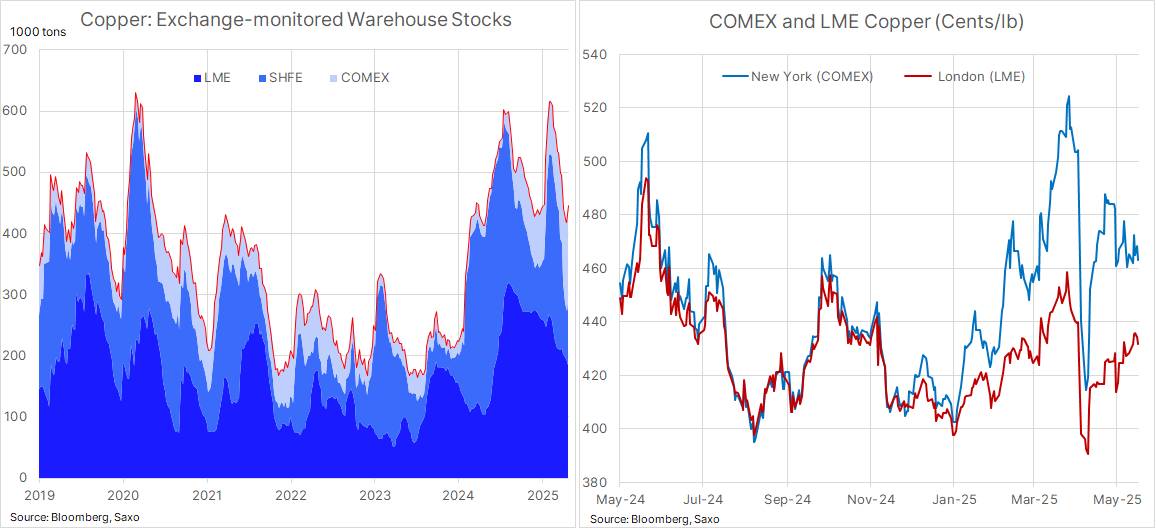

Spot Platinum (XPTUSD) - Source: SaxoTraderGOBenchmark copper prices in London were heading for a small weekly gain, extending a rebound from a 13-month low hit in April, as investors weigh tightening supply against a clouded economic outlook. The tightness has primarily been driven by a major transfer of copper to the US ahead of an expected tariff announcement, leaving the rest of the world, which accounts for more than 90% of global demand, with lower supplies.

Since the US opened a probe into the copper market back in February, potentially leading to an implementation of tariffs on imports similar to the 25% tariff on all steel and aluminium imports that came into force this month, the spread between the High Grade contract on COMEX in New York and the global LME benchmark in London has seen a great deal of volatility, culminating at the end of March when the premium reached 16%.

A level that helped trigger a massive, and ongoing surge in shipments of copper to the US, leading to a surge in copper stocks in COMEX-monitored warehouses to the highest since 2018, well above what is needed. As a result, and despite the risk of a 25% tariff being introduced, the premium over London has come down to around 7% on a combination of softer COMEX and firmer LME prices. Ample supply within the US has now created a glut that would delay the price impact of an eventual tariff introduction.

Exchange monitored copper stocks and COMEX and LME prices

Exchange monitored copper stocks and COMEX and LME pricesFollowing the early April price collapse, both WTI and Brent—widely regarded as the two global benchmarks for crude oil—have settled into broad, yet volatile, $10-per-barrel trading ranges. WTI has fluctuated between $55 and $65, while Brent has moved between $58.5 and $68.5. Market sentiment continues to alternate between concerns over rising global supply and the potential economic fallout from ongoing global trade tensions.

Over the past week, a fresh attempt to push prices higher—driven by renewed hopes from U.S.-China trade negotiations—was only partially successful. Gains were quickly reversed amid bearish supply-side developments. U.S. crude inventories posted another increase, and the Energy Information Administration (EIA) reported a 10% decline in the four-week average of U.S. crude oil exports. This drop brought export levels well below seasonal averages from the past two years and may indicate weakening demand among key buyers in Europe and Asia.

Meanwhile, the International Energy Agency (IEA) has warned of a global oil glut both this year and next, citing a combination of robust supply growth and slower-than-expected demand expansion. The potential revival of the Iran nuclear deal could further aggravate this imbalance by bringing additional barrels to market. This would add to the already announced output increases from eight OPEC+ members, spearheaded by Saudi Arabia.

In the short term, we expect oil prices to continue oscillating within their current ranges. Market participants remain focused on four key uncertainties: developments in global trade negotiations, lower prices’ potential negative impact on supply from high-cost producers, the extent of future production increases from OPEC+ members, and whether the group can rein in persistent quota violations. Recent compliance data suggests cumulative overproduction peaked at around 800,000 barrels per day, with Iraq, Kazakhstan, and the UAE identified as the primary offenders.

Brent Crude Oil, first month future - Source: SaxoTraderGO

Brent Crude Oil, first month future - Source: SaxoTraderGO728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up