Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

BitMEX founder Arthur Hayes suggests Fed intervention in Japan's bond crisis with money printing could spark Bitcoin's revival.

BitMEX founder Arthur Hayes has outlined a scenario where the U.S. Federal Reserve could start printing money to support Japan's fragile government bond market, a move he believes could pull Bitcoin out of its current slump.

Hayes argues that for Bitcoin to "exit its sideways funk, it needs a healthy dose of money printing," and a looming crisis in Japan may provide the trigger.

Japan is currently facing a serious economic challenge: its currency, the yen, is weakening while the yields on Japanese government bonds (JGBs) are simultaneously rising. This combination signals a potential loss of confidence in the market.

The problem extends to the United States because Japanese investors, who are major holders of U.S. Treasuries, might be tempted to sell them to purchase higher-yielding JGBs back home.

"Will a meltdown of the yen and JGB markets cause some sort of money printing by the BOJ [Bank of Japan] or the Fed? The answer is yes," said Hayes.

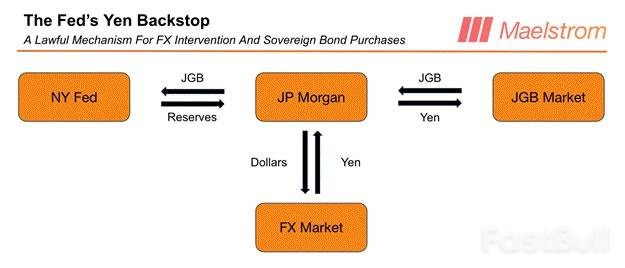

Hayes theorizes that the Fed could intervene through a specific mechanism to strengthen the yen and lower Japanese bond yields. The process would involve:

1. The Fed creating new dollar reserves with commercial banks like JPMorgan.

2. These banks would then sell the dollars to purchase yen on the open market, boosting the yen's value.

3. The acquired yen would then be used to buy JGBs, which would push their yields down.

This operation would effectively expand the Fed's balance sheet, showing up under the "Foreign Currency Denominated Assets" category. "This Fed intervention is just what the filthy fiat system needs to limp along a little longer," Hayes explained.

Despite his theory, Hayes is exercising caution and waiting for concrete evidence of intervention. He is closely monitoring the Fed's weekly H.4.1 report, which details the central bank's balance sheet.

"Bitcoin fell as the yen strengthened against the dollar. I will not increase risk before I confirm the Fed is printing money to intervene in the yen and JGB markets," he stated, indicating he is holding off on major market moves for now.

Meanwhile, the U.S. dollar index (DXY) has been under pressure, falling to 95.6 on Tuesday—its lowest point since January 2022. The dollar has declined 10% over the past year.

Speaking in Iowa on Tuesday, U.S. President Donald Trump maintained that the dollar was "doing great."

"I mean, the value of the dollar, look at the business we're doing. No, the dollar is doing great," he said, according to CNBC. Trump also recalled past tensions over currency valuation, stating, "I used to fight like hell with them because they always wanted to devalue their yen... you know that, the yen and yuan, and they'd always want to devalue it. They devalue, devalue, devalue. And I said, 'not fair.' They devalue, because it's hard to compete when they devalue."

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up