- AUDUSD

- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Central Bank

Bond

Commodity

Remarks of Officials

Political

Technical Analysis

Traders' Opinions

Economic

Daily News

Forex

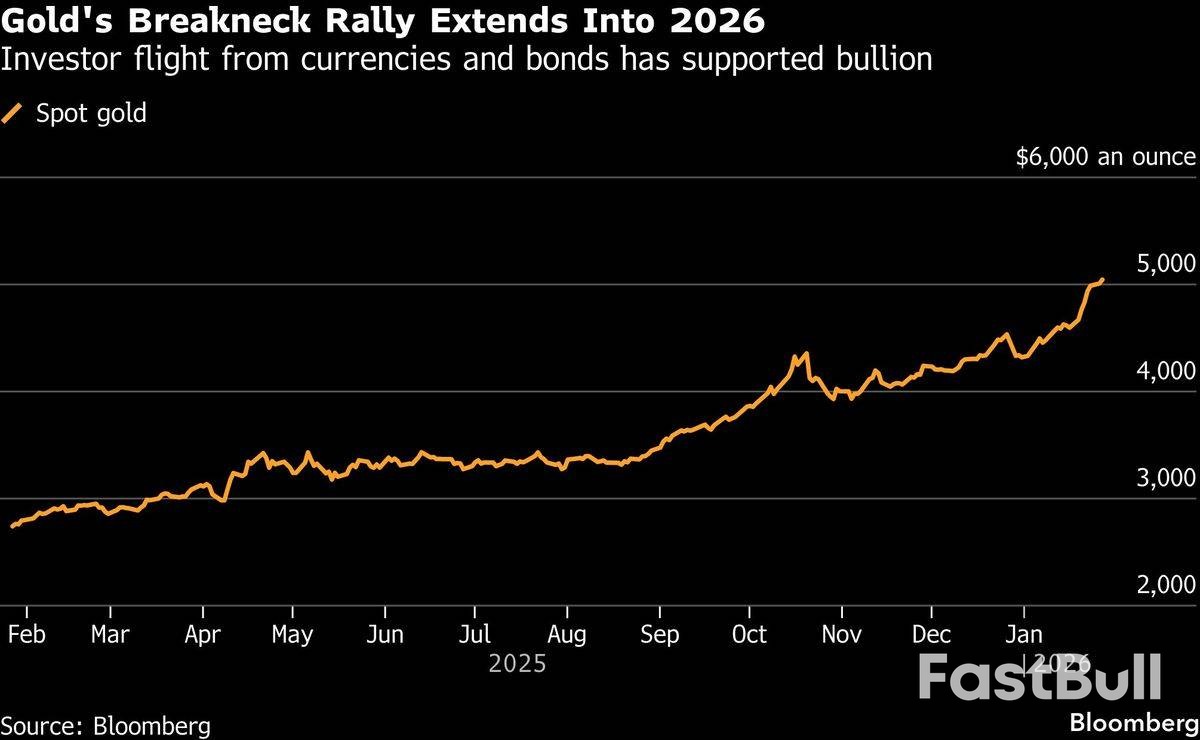

Gold hits record highs, fueled by geopolitical turmoil and currency fears, prompting a flight to safety.

Gold prices pushed above the key US$5,000 per ounce mark for a second consecutive day, extending a powerful rally driven by a weakening U.S. dollar and mounting geopolitical risk. The precious metal is capitalizing on a flight from sovereign bonds and traditional currencies as investors seek safe-haven assets.

On Tuesday, bullion climbed as much as 1.4%, marking its seventh straight day of gains. The rally gained momentum after U.S. President Donald Trump threatened to raise tariffs on South Korean goods. A key dollar index also fell on Monday amid speculation that the U.S. might assist Japan in supporting the yen, a move that makes dollar-priced gold cheaper for international buyers. Silver also saw significant gains, climbing over 7%.

Gold's recent performance underscores its traditional role as a barometer of market fear. The metal, which has more than doubled in value over the last two years, is building on its best annual performance since 1979 with a further 17% gain so far this year.

This surge is largely attributed to the "debasement trade," a strategy where investors move away from government-backed currencies and bonds over concerns about fiscal policy and currency devaluation. A recent large-scale sell-off in the Japanese bond market is a prime example of investors pushing back against heavy government spending.

Recent actions by the Trump administration have further unsettled investors. Market confidence has been shaken by threats of military intervention in Venezuela, proposals to annex Greenland, and renewed attacks on the independence of the U.S. Federal Reserve.

The warning to South Korea came shortly after a weekend threat to impose 100% tariffs on Canada if it finalizes a trade agreement with China. According to Europe's largest money manager, Amundi SA, America's growing isolation is prompting many investors to reduce their holdings of dollar-denominated assets in favor of gold.

"Gold in the long term is a very good protection against debasement and a good way to maintain some purchasing power," said Vincent Mortier, Amundi's chief investment officer, in a Bloomberg Television interview.

The bullish sentiment for gold is reflected across derivatives markets, where traders are positioning for further price increases.

• Implied Volatility: Volatility on Comex gold futures has climbed to its highest level since the peak of the Covid-19 pandemic in March 2020.

• ETF Activity: The world's largest gold-backed exchange-traded fund, State Street's SPDR Gold Shares, has also seen a significant breakout in volatility.

"Traders are buying pullbacks rather than fading rallies," noted Fawad Razaqzada, an analyst at City Index Ltd. "As long as that mindset persists, it is difficult to argue against higher prices in the near term, even if there is a short-term disconnect between fundamentals and reality."

Investors are closely watching for President Trump's nomination for the next Federal Reserve chair. The president has confirmed he has interviewed candidates and has a specific individual in mind. A more dovish appointment could fuel bets on further interest rate cuts this year—a positive catalyst for non-yielding gold—following three consecutive reductions.

In the more immediate term, however, the U.S. central bank is widely expected to pause its rate-cutting cycle on Wednesday. A stabilizing jobs market appears to have restored some consensus among policymakers after months of division.

As of 1 p.m. in Singapore, gold was trading 1.2% higher at US$5,067.84 an ounce. Silver advanced 4.3% to US$108.25 an ounce, after hitting an all-time high above US$117.71 in the previous session. Platinum and palladium also posted gains, while the Bloomberg Dollar Spot Index edged up 0.1% after falling 0.4% in the prior session.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up