Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

December CPI masks deeper inflation: surging money supply and renewed Fed QE point to persistent price pressures.

The December Consumer Price Index (CPI) report was as complex as analysts predicted, but the real story of inflation isn't in the headline numbers. A closer look at money supply and central bank activity reveals pressures that the official data may be missing.

At first glance, the December inflation data seemed to align with expectations, offering a sliver of optimism for markets hoping for future monetary easing.

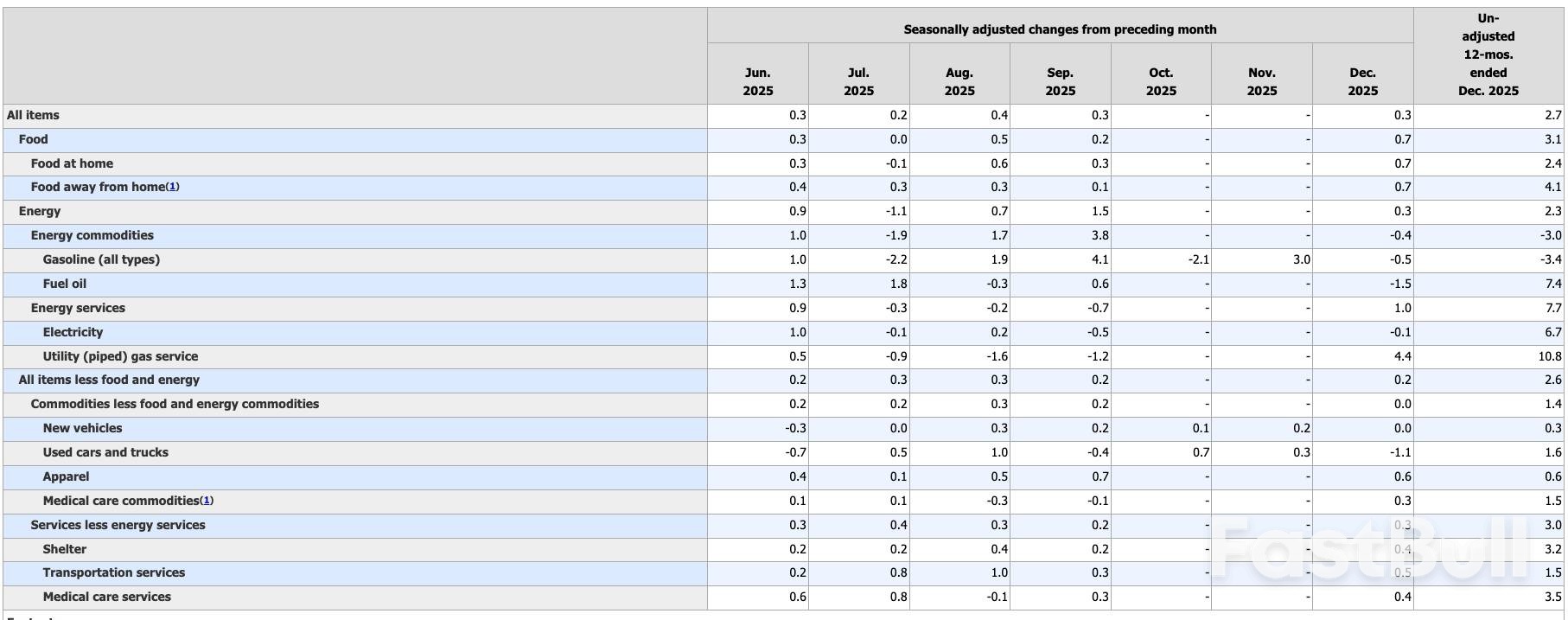

The overall CPI rose 0.3% month-on-month, holding the annual inflation rate steady at 2.7%. When stripping out volatile food and energy costs, the core CPI increased by 0.2% for the month, with the annual rate unchanged at 2.6%. This slightly cooler-than-expected core reading fueled speculation that the Federal Reserve might continue easing monetary policy in 2026.

However, a persistent trend lies beneath the surface. Over the last six available readings, core CPI has posted increases of 0.2%, 0.3%, 0.3%, 0.2%, 0.2%, and 0.2%. This pattern annualizes to a rate of 2.8%, showing that core inflation has been stuck in this range for over a year.

A detailed breakdown of the December report shows specific price pressures:

• Shelter: Increased by 0.4%

• Food: Surged by 0.7%

• Energy: Rose by 0.3%, even as gasoline prices fell 0.4%

• Services: Grew by 0.3%

• Used Cars & Trucks: Posted the largest decline, falling 1.1%

It’s crucial to approach the CPI report with caution. The data's reliability has been questioned, particularly following a November report some critics described as heavily estimated.

Furthermore, the government's methodology for calculating CPI was revised in the 1990s, leading to a formula that many argue systematically understates the true rise in the cost of living. If the formula from the 1970s were still in use, today's official CPI figures would likely be closer to 6%.

Even based on the current official data, inflation remains well above the Federal Reserve's target. As Ellen Zentner, chief economic strategist at Morgan Stanley, noted, the situation feels familiar.

"We've seen this movie before—inflation isn't reheating, but it remains above target," Zentner stated. "Today's inflation report doesn't give the Fed what it needs to cut interest rates later this month."

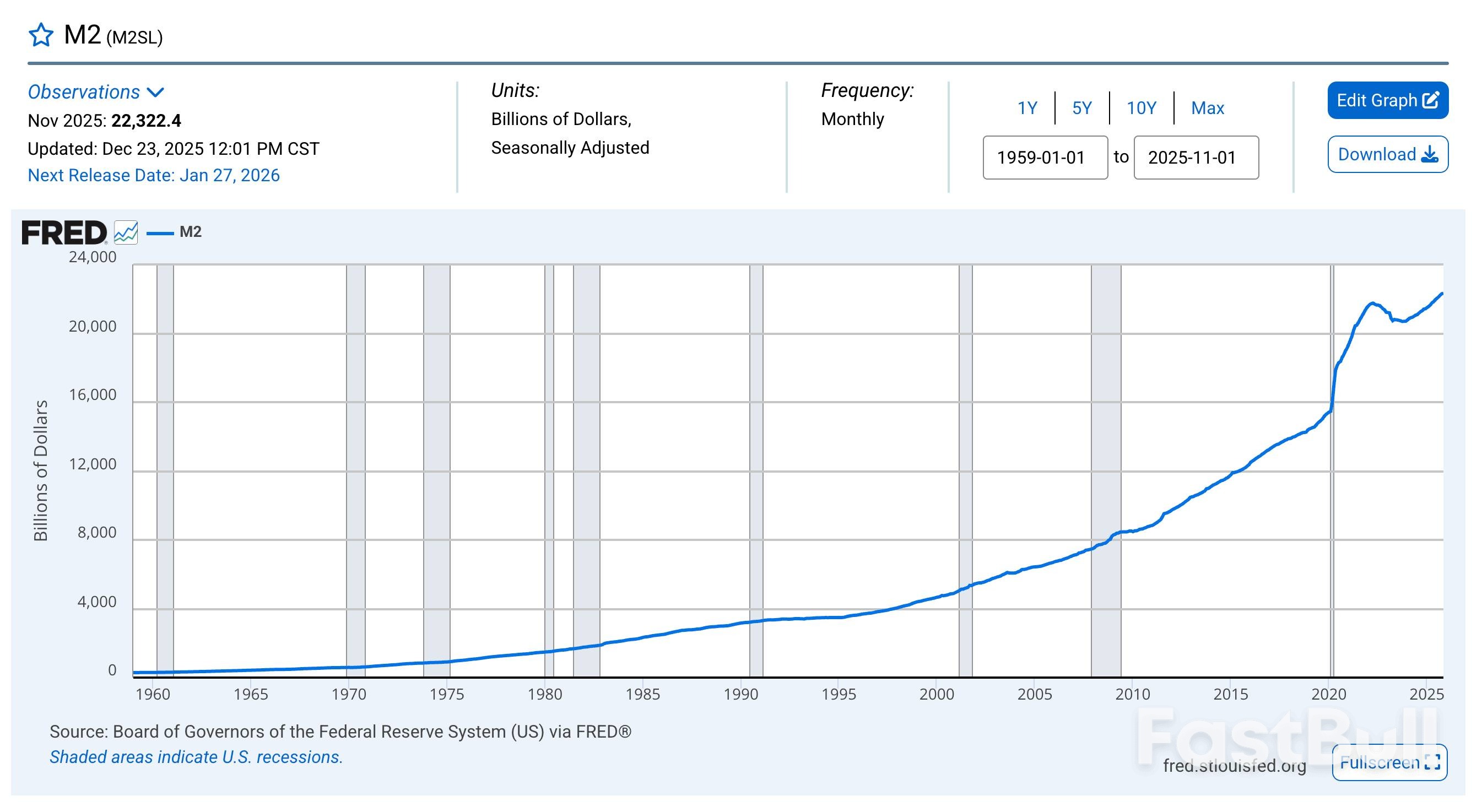

The CPI measures price changes in a specific basket of goods, but it only captures a symptom of inflation. Historically, economists defined inflation as an increase in the supply of money and credit. Rising prices are the consequence of this monetary expansion.

By this fundamental measure, inflation is not only present but accelerating. The M2 money supply is currently growing at its fastest rate since July 2022. After hitting a low in October 2023, the money supply has resumed its upward trajectory, now surpassing its pandemic-era peak as money creation has quickened in recent months.

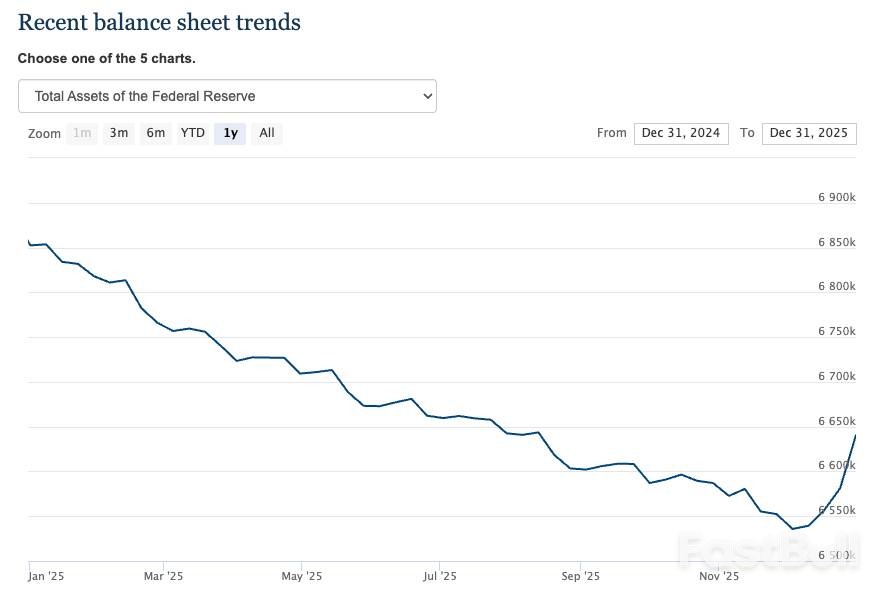

Further evidence of rising inflationary pressure comes from the Federal Reserve's balance sheet, which is once again expanding.

Last month, the central bank resumed purchasing U.S. Treasuries with newly created money, effectively restarting its quantitative easing (QE) program. This direct injection of liquidity into the financial system is, by definition, inflationary.

This leads to a fundamental conflict for the central bank. The Fed is caught in a Catch-22: it needs to loosen monetary policy through rate cuts and QE to support a debt-laden economy, but it also needs higher rates to bring price inflation back under control. It cannot do both at the same time.

Any "cooler than expected" CPI report provides political cover to prioritize easing, despite official rhetoric aimed at managing expectations. This dynamic ensures that even if official price metrics cool temporarily, the underlying inflationary forces are likely to grow stronger.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up