Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Global financial markets responded very enthusiastically this past week to news that the US and China had agreed to a 90-day pause in their escalating trade war.

Key points in this update:

Global financial markets responded very enthusiastically this past week to news that the US and China had agreed to a 90-day pause in their escalating trade war, for now reducing punitive tariffs that were beginning to hurt both economies, threatening a recession in the US and a slowdown in China’s export-driven economy. This de-escalation provided what may still turn out to be temporary relief to markets, with global equity markets and pro-cyclical commodities staging a comeback while haven demand for gold faded.

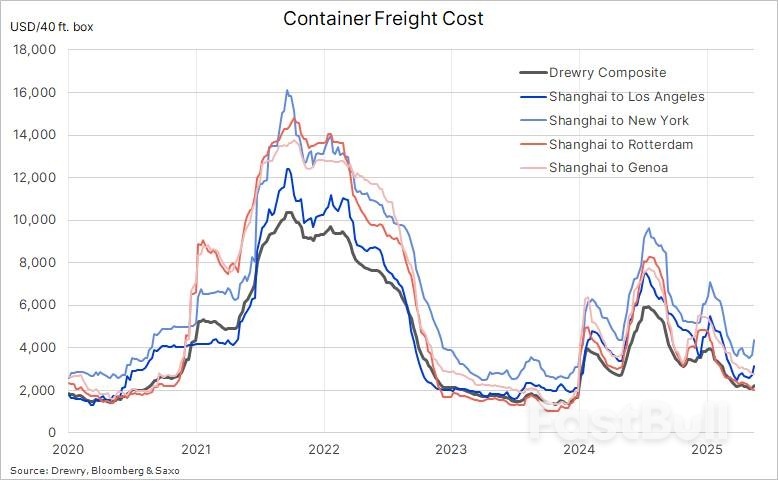

The announcement of a 90-day truce in trade tensions prompted a swift and strong reaction from the global shipping industry. The Drewry Global Container Index—a key benchmark that tracks weekly freight rates for container shipping across major international routes showed a jump in the Shanghai–Los Angeles and Shanghai–New York lanes by 15.6% and 19.3%, respectively. The notable rebound on these routes reflects a renewed wave of frontloading activity, as exporters and importers in both China and the United States rush to ship goods ahead of any potential re-escalation of tariffs once the truce expires. Yet, the overall index remains down around 40% this year amid rising container capacity and tariff threats to global trade.

Drewry Global Container Freight Indices

Drewry Global Container Freight IndicesThe risk-on rally saw the tech-heavy Nasdaq reach February levels, reversing most of its tariff-related weakness, while USD bears were challenged and US Treasury yields, especially at the long end, rose to levels that raised a few eyebrows, not least considering an urgent need to bring down funding costs to service a growing fiscal deficit. Economic data in the US showed the first albeit small signs of what may come in the coming months as tariffs start to impact consumers. While prices paid to US producers unexpectedly declined by the most in five years, suggesting companies, for now, are absorbing some of the hit from higher tariffs. Separate data for April showed growth in retail sales decelerated while factory production declined for the first time in six months, and confidence fell for a third month.

All signs indicate that the near-term economic outlook, not only in the US but also abroad—note Japan’s economy shrank for the first time in a year—remains challenged and vulnerable even before sustaining the full impact of Trump’s tariff measures. With this in mind, the prospect for additional dollar gains remains limited while the next rate cut from the US Federal Reserve is not a question of if but when they will cut next time; note the market is currently pricing in fully two 25-basis point cuts this year, followed by another two next year.

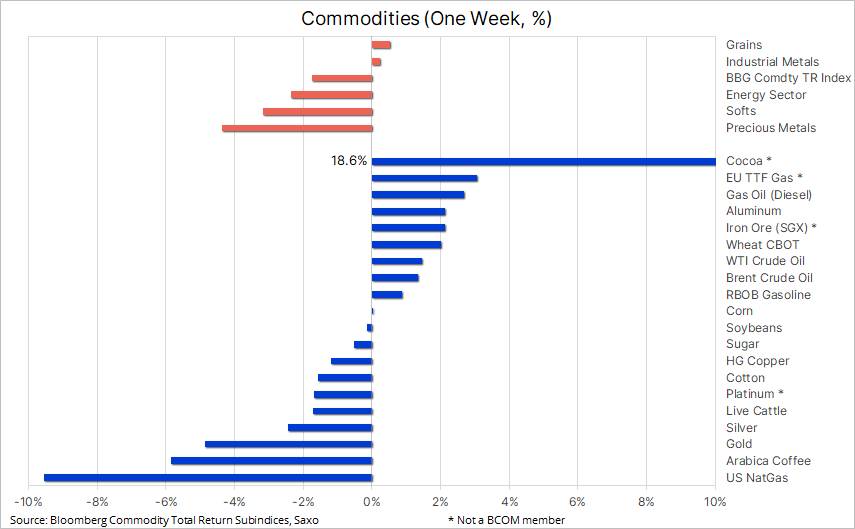

Overall, the trade truce initially gave pro-cyclical commodities, such as energy and industrial metals a boost, before fading amid economic data weakness, leading the Bloomberg Commodity Index towards a weekly loss around 1.8%, lowering the year-to-date gain to 3.8%. Weighing on the index which tracks a basket of 24 major commodities futures spread almost evenly between energy, metals and agricultural, were a steep 9.6% loss in natural gas, and 5% drop in gold, two commodities that together with Arabica coffee (-6%) accounts for around 25% of the index. At the other end of the spectre, cocoa – a non-BCOM member - surged higher almost 19% and back above USD 11,000 tons amid renewed concerns about the quality and size of the current crop being harvested in West Africa.

Key commodities: one week performances

Key commodities: one week performancesGold has experienced its sharpest correction—both in absolute and percentage terms—since 2023, breaking through multiple technical support levels. The initial trigger was a fading of safe-haven demand following the US-China 90-day trade truce. However, prices have since found renewed support amid a weakening dollar and falling bond yields, driven by a batch of softer-than-expected U.S. economic data.

Having already hit our 2025 price target of USD 3,500, we are currently adopting a wait-and-see approach. The market remains caught between profit-taking from those selling into strength and renewed interest from dip buyers. Despite the recent pullback, several key structural drivers—including central bank buying, geopolitical risks, fiscal debt concerns, and inflation hedging—remain intact. These are likely to underpin prices over the longer term, though a period of consolidation may be required before the next significant upside catalyst emerges.

Investor flows will be critical to watch going forward, particularly in China, where demand from retail investors through yuan-denominated ETFs has been a key source of support before recently fading. In contrast, Western-based ETF holdings have seen net outflows since late April, contributing to the softer price environment. Meanwhile, speculative positioning in COMEX futures has turned increasingly bearish, with managed money and other reportables reducing their net long exposure by 42% over the past seven weeks. This highlights the need for a fresh technical breakout or macro catalyst to entice these key participants back to the buy side.

While gold fell sharply, silver and platinum also declined but were partially shielded by their industrial use cases. Optimism around U.S.-China trade relations has lent support to growth-sensitive commodities, tempering the downside in these two metals. The gold-silver ratio has since pulled back below 100, after spiking above 105 in early April.

Platinum has underperformed both on a relative and absolute basis over the past decade. Once at parity with gold, it now trades at a ratio of 3.2:1, while its average price of USD 955 per oz over the past 17 years is just below current levels. This underperformance comes despite three consecutive years of structural deficits. According to Johnson Matthey, primary supply is expected to fall by 3% in 2025 to 5.54 million troy ounces, while demand is seen slipping 2.6% to 7.66 million ounces. Yet investment flows remain weak amid macroeconomic uncertainty, trade risks, and a softening outlook for the automotive sector, platinum’s largest demand driver.

Platinum remains trapped in a narrowing technical range. A breakout could provide the spark for renewed speculative interest. Until then, COMEX-managed money accounts remain largely neutral. We are closely watching USD 1,010 as near-term resistance and USD 1,025 as the more significant downtrend level stemming from the 2008 highs.

Spot Platinum (XPTUSD) - Source: SaxoTraderGO

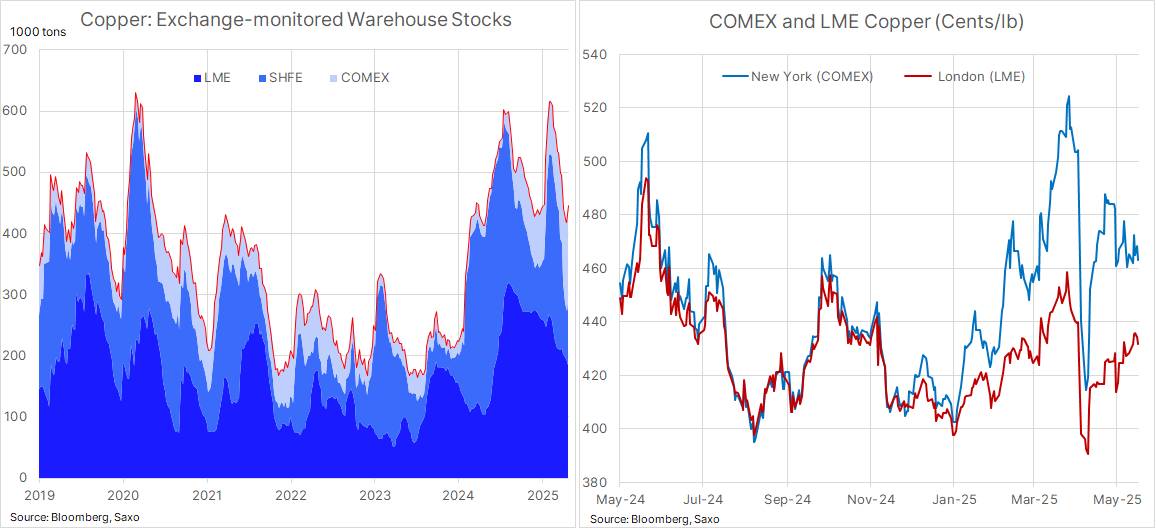

Spot Platinum (XPTUSD) - Source: SaxoTraderGOBenchmark copper prices in London were heading for a small weekly gain, extending a rebound from a 13-month low hit in April, as investors weigh tightening supply against a clouded economic outlook. The tightness has primarily been driven by a major transfer of copper to the US ahead of an expected tariff announcement, leaving the rest of the world, which accounts for more than 90% of global demand, with lower supplies.

Since the US opened a probe into the copper market back in February, potentially leading to an implementation of tariffs on imports similar to the 25% tariff on all steel and aluminium imports that came into force this month, the spread between the High Grade contract on COMEX in New York and the global LME benchmark in London has seen a great deal of volatility, culminating at the end of March when the premium reached 16%.

A level that helped trigger a massive, and ongoing surge in shipments of copper to the US, leading to a surge in copper stocks in COMEX-monitored warehouses to the highest since 2018, well above what is needed. As a result, and despite the risk of a 25% tariff being introduced, the premium over London has come down to around 7% on a combination of softer COMEX and firmer LME prices. Ample supply within the US has now created a glut that would delay the price impact of an eventual tariff introduction.

Exchange monitored copper stocks and COMEX and LME prices

Exchange monitored copper stocks and COMEX and LME pricesFollowing the early April price collapse, both WTI and Brent—widely regarded as the two global benchmarks for crude oil—have settled into broad, yet volatile, $10-per-barrel trading ranges. WTI has fluctuated between $55 and $65, while Brent has moved between $58.5 and $68.5. Market sentiment continues to alternate between concerns over rising global supply and the potential economic fallout from ongoing global trade tensions.

Over the past week, a fresh attempt to push prices higher—driven by renewed hopes from U.S.-China trade negotiations—was only partially successful. Gains were quickly reversed amid bearish supply-side developments. U.S. crude inventories posted another increase, and the Energy Information Administration (EIA) reported a 10% decline in the four-week average of U.S. crude oil exports. This drop brought export levels well below seasonal averages from the past two years and may indicate weakening demand among key buyers in Europe and Asia.

Meanwhile, the International Energy Agency (IEA) has warned of a global oil glut both this year and next, citing a combination of robust supply growth and slower-than-expected demand expansion. The potential revival of the Iran nuclear deal could further aggravate this imbalance by bringing additional barrels to market. This would add to the already announced output increases from eight OPEC+ members, spearheaded by Saudi Arabia.

In the short term, we expect oil prices to continue oscillating within their current ranges. Market participants remain focused on four key uncertainties: developments in global trade negotiations, lower prices’ potential negative impact on supply from high-cost producers, the extent of future production increases from OPEC+ members, and whether the group can rein in persistent quota violations. Recent compliance data suggests cumulative overproduction peaked at around 800,000 barrels per day, with Iraq, Kazakhstan, and the UAE identified as the primary offenders.

Brent Crude Oil, first month future - Source: SaxoTraderGO

Brent Crude Oil, first month future - Source: SaxoTraderGO728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

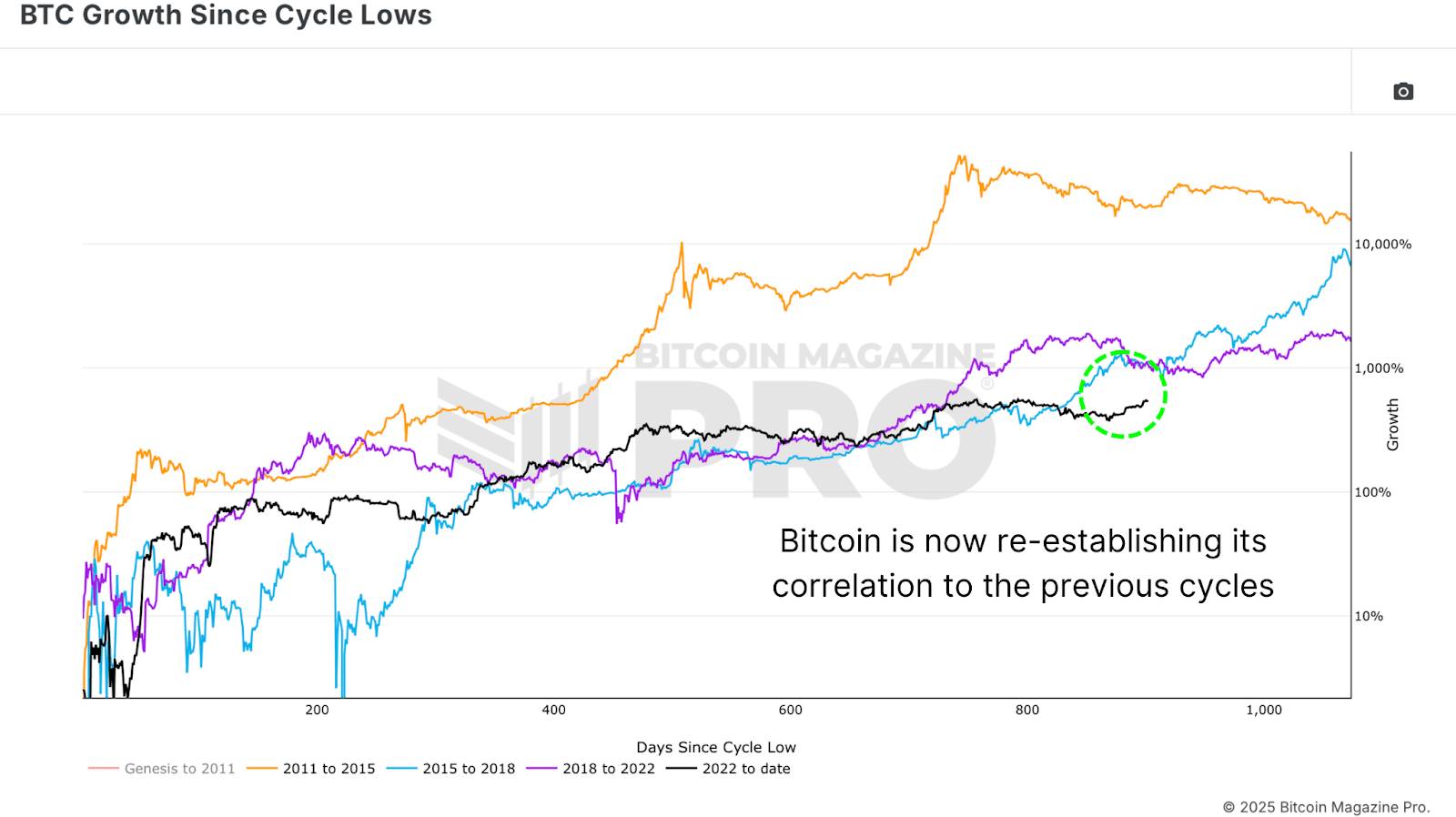

Figure 1: Bitcoin’s 2025 bullish price action mirrors previous cycles.

Figure 1: Bitcoin’s 2025 bullish price action mirrors previous cycles. Figure 2: MVRV-Z Score shows behavioral similarities to the 2017 Bitcoin bull run.

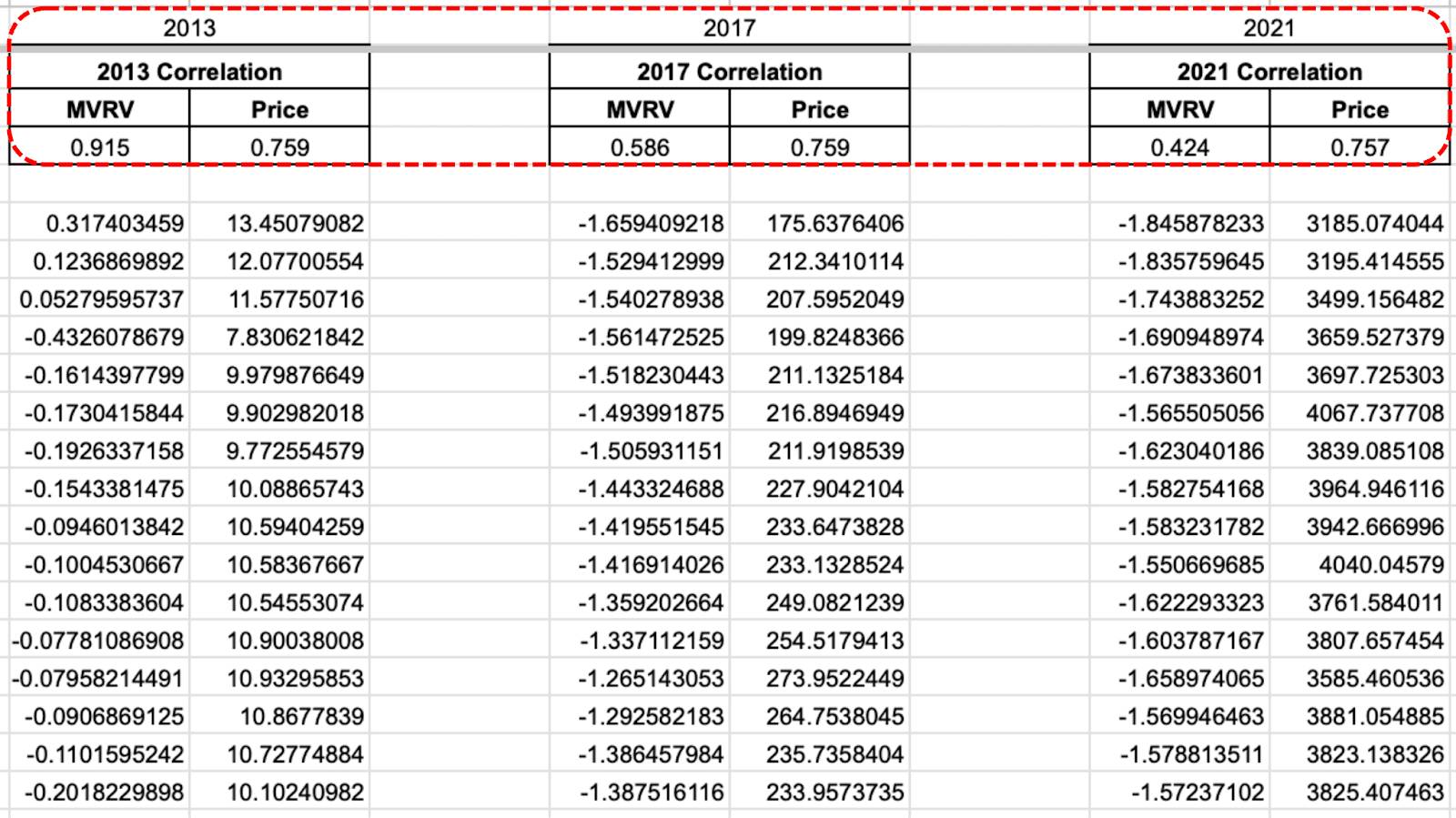

Figure 2: MVRV-Z Score shows behavioral similarities to the 2017 Bitcoin bull run.  Figure 3: Cross-cycle behavioral correlations using rolling MVRV-Z scores and price action.

Figure 3: Cross-cycle behavioral correlations using rolling MVRV-Z scores and price action. Figure 4: The rate of change in the 1+ Year HODL Wave suggests confidence in future Bitcoin prices.

Figure 4: The rate of change in the 1+ Year HODL Wave suggests confidence in future Bitcoin prices.  Figure 5: A repeat of 2017’s exponential Bitcoin price growth may be ambitious.

Figure 5: A repeat of 2017’s exponential Bitcoin price growth may be ambitious.