Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Warren Buffett, the greatest investor of all time, has announced his retirement. Fellow...

Warren Buffett, the greatest investor of all time, has announced his retirement. Fellow value investors are in a state of shock. Unfortunately, they have more serious problems to consider. For years, their favoured investment style has been out of fashion. Clients have lost patience. In a world in which the U.S. stock market index has delivered consistently outsized returns, low-cost funds that passively track an index seem a no-brainer. Yet the prospects for value investors have always been always brightest when the rest of the world loses faith.

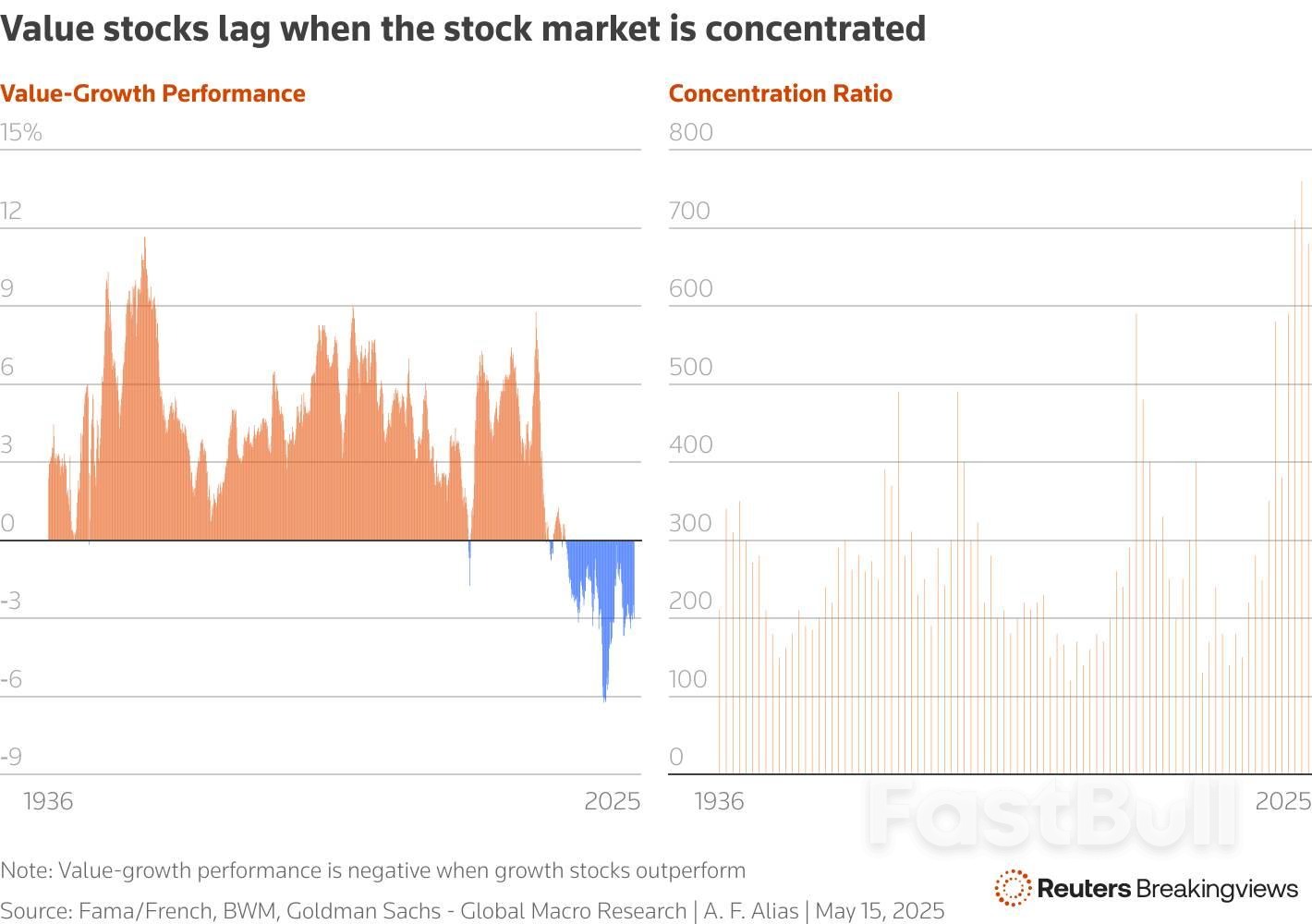

Over the very long run, buying equities at relatively cheap valuations has worked out well. Economists Eugene Fama and Ken French define value as a low ratio of share price to book value. Using this measure, U.S. value stocks have beaten growth stocks, which have high price-to-book ratios, by 2.5% a year since 1926. Value has also outperformed in most other overseas markets, according to the UBS Global Investment Returns Yearbook compiled by Elroy Dimson, Paul Marsh and Mike Staunton. Its luck ran out, however, on the eve of the global financial crisis. Between 2007 and 2020, growth beat value. The latter recovered some ground in 2020 but fell back again after the “Magnificent Seven” big technology stocks took off in late 2022.

It is important to note that price to book is not the metric contemporary value investors rely upon. Warren Buffett’s partner, the late Charlie Munger, taught him to consider a firm’s competitive position – what the Oracle of Omaha called the “moat.” If a business consistently earns above average returns on capital, investors can safely buy its shares at a premium multiple to the rest of the market. Furthermore, the balance sheet value of a company’s assets is not a reliable measure of value, since it excludes many intangible assets such as research and development. Share buybacks and acquisitions further distort accounting book value.

Still, there are other investment oddities to consider. Small-cap stocks, which historically have beaten larger rivals and provide a favourite hunting ground for value investors, have also had a dismal run. Global stock markets, both the developed and emerging variety, have been trounced by the extraordinary performance of U.S. stocks. Between 2010 and the start of this year, American equities had delivered annualised returns of 10% after inflation, according to UBS. Over the same period, the other stock markets have collectively returned 2.6% a year after inflation. Emerging markets returned just half that figure. Howard Marks, the veteran value investor and co-chairman of Oaktree Capital Management, laments that “all norms have been overturned.”

The hard times for value investing can be explained by various factors. First, ultra-low interest rates after the global financial crisis increased the appeal of growth stocks whose profits lie in the distant future. Higher-yielding value stocks were relatively disadvantaged.

Second, value investors have suffered from the rapid expansion of index investing. Nearly 60% of the U.S. stock market is currently held by funds that passively track a benchmark. Goldman Sachs forecasts that between 2014 and 2026 the cumulative outflows from U.S. actively managed equity mutual funds into passive vehicles will reach around $3 trillion. As indexation advances, investors dump the value and small-cap stocks owned by traditional fund managers in favour of the S&P 500 Index (.SPX), opens new tab, which is heavily weighted towards larger and more expensive stocks.

The United States is home to the largest and most profitable companies the world has ever seen. The outsized returns of the Magnificent Seven over the last decade have depressed the relative returns of both value stocks and small caps. By the end of last year, the U.S. stock market had become more concentrated than at any time since the 1930s. Georg von Wyss, a portfolio manager at Zurich-based firm BWM, observes that in the past periods of extreme market concentration have been accompanied by the underperformance of value stocks. This was the case during the “Nifty Fifty” boom of the early 1970s and again in the technology bubble of the late 1990s.

Towards the end of that craze, value stocks were exceedingly cheap relative to the overall market. Clients closed their accounts with underperforming investment firms. Several well-known value managers were either fired or took early retirement. Warren Buffett, who didn’t partake in the market frenzy, was deemed to have lost the plot. But when the boom turned to bust and market concentration declined, as it did in 1975 and 2000, value stocks outperformed for years. Could value investors be on the verge of yet another winning streak?

The turmoil of the early months of Donald Trump’s second term may signal such a shift. At the London Value Investor Conference on Wednesday Richard Oldfield of Oldfield Partners said that the new U.S. administration, with its on-off threat of tariffs and hostile rhetoric to erstwhile allies, poses a risk to trend of “American exceptionalism”. Sensing the loss of U.S. support, Germany is borrowing to invest in defence and infrastructure. If capital flows to the United States start to reverse, developed and emerging stock markets stand to benefit. Value rallies have repeatedly petered out in recent years but, says Oldfield, “this time is different.”

Other headwinds that have buffeted value investors over the past decade may also be about to disperse. Over the past three years, interest rates have returned to more normal levels. The Magnificent Seven are currently locked in an arms race to invest in artificial intelligence. Time will tell whether their vast capital spending delivers an adequate return. These megacap growth stocks have underperformed in the year to date. Meanwhile, value and small-cap stocks in the United States and elsewhere offer exceptional opportunities.

Last year, David Einhorn of Greenlight Capital pronounced that value was “dead, opens new tab”. Another speaker at the London conference, Alissa Corcoran of Kopernik Global Investors refutes this claim. Value investing is immortal, she says. As index funds absorb a greater share of the world’s stock market, fundamental investors are still needed to perform the vital role of price discovery. Ideally, such investors would exhibit a patient, long-term approach and not be swayed by the herd. They should be careful stewards of their clients’ capital, and, above all, be endowed with common sense. Warren Buffett displayed these virtues to an uncommon degree. He will be missed. But there are legions of value investors ready to fill the void.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up