Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.S. Average Hourly Wage MoM (SA) (Dec)

U.S. Average Hourly Wage MoM (SA) (Dec)A:--

F: --

U.S. Average Weekly Working Hours (SA) (Dec)A:--

F: --

P: --

U.S. New Housing Starts Annualized MoM (SA) (Oct)A:--

F: --

U.S. Total Building Permits (SA) (Oct)A:--

F: --

P: --

U.S. Building Permits MoM (SA) (Oct)A:--

F: --

P: --

U.S. Annual New Housing Starts (SA) (Oct)A:--

F: --

U.S. U6 Unemployment Rate (SA) (Dec)A:--

F: --

P: --

U.S. Manufacturing Employment (SA) (Dec)A:--

F: --

U.S. Labor Force Participation Rate (SA) (Dec)A:--

F: --

P: --

U.S. Private Nonfarm Payrolls (SA) (Dec)A:--

F: --

U.S. Unemployment Rate (SA) (Dec)A:--

F: --

U.S. Nonfarm Payrolls (SA) (Dec)A:--

F: --

U.S. Average Hourly Wage YoY (Dec)A:--

F: --

Canada Full-time Employment (SA) (Dec)

Canada Full-time Employment (SA) (Dec)A:--

F: --

P: --

Canada Part-Time Employment (SA) (Dec)A:--

F: --

P: --

Canada Unemployment Rate (SA) (Dec)A:--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Dec)A:--

F: --

P: --

U.S. Government Employment (Dec)A:--

F: --

P: --

Canada Employment (SA) (Dec)A:--

F: --

P: --

U.S. UMich Consumer Expectations Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich Consumer Sentiment Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich Current Economic Conditions Index Prelim (Jan)A:--

F: --

P: --

U.S. UMich 1-Year-Ahead Inflation Expectations Prelim (Jan)A:--

F: --

P: --

U.S. UMich 5-Year-Ahead Inflation Expectations Prelim YoY (Jan)A:--

F: --

P: --

U.S. 5-10 Year-Ahead Inflation Expectations (Jan)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Dec)

China, Mainland M1 Money Supply YoY (Dec)--

F: --

P: --

China, Mainland M0 Money Supply YoY (Dec)--

F: --

P: --

China, Mainland M2 Money Supply YoY (Dec)--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

Indonesia Retail Sales YoY (Nov)

Indonesia Retail Sales YoY (Nov)--

F: --

P: --

Euro Zone Sentix Investor Confidence Index (Jan)

Euro Zone Sentix Investor Confidence Index (Jan)--

F: --

P: --

India CPI YoY (Dec)

India CPI YoY (Dec)--

F: --

P: --

Germany Current Account (Not SA) (Nov)

Germany Current Account (Not SA) (Nov)--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

FOMC Member Barkin Speaks U.S. 3-Year Note Auction Yield--

F: --

P: --

U.S. 10-Year Note Auction Avg. Yield--

F: --

P: --

Japan Trade Balance (Customs Data) (SA) (Nov)

Japan Trade Balance (Customs Data) (SA) (Nov)--

F: --

P: --

Japan Trade Balance (Nov)--

F: --

P: --

U.K. BRC Overall Retail Sales YoY (Dec)

U.K. BRC Overall Retail Sales YoY (Dec)--

F: --

P: --

U.K. BRC Like-For-Like Retail Sales YoY (Dec)--

F: --

P: --

Turkey Retail Sales YoY (Nov)

Turkey Retail Sales YoY (Nov)--

F: --

P: --

U.S. NFIB Small Business Optimism Index (SA) (Dec)--

F: --

P: --

Brazil Services Growth YoY (Nov)

Brazil Services Growth YoY (Nov)--

F: --

P: --

Canada Building Permits MoM (SA) (Nov)--

F: --

P: --

U.S. CPI MoM (SA) (Dec)--

F: --

P: --

U.S. CPI YoY (Not SA) (Dec)--

F: --

P: --

U.S. Real Income MoM (SA) (Dec)--

F: --

P: --

U.S. CPI MoM (Not SA) (Dec)--

F: --

P: --

U.S. Core CPI (SA) (Dec)--

F: --

P: --

U.S. Core CPI YoY (Not SA) (Dec)--

F: --

P: --

U.S. Core CPI MoM (SA) (Dec)--

F: --

P: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. New Home Sales Annualized MoM (Oct)--

F: --

P: --

U.S. Annual Total New Home Sales (Oct)--

F: --

P: --

U.S. Cleveland Fed CPI MoM (SA) (Dec)--

F: --

P: --

China, Mainland Imports YoY (CNH) (Dec)--

F: --

P: --

China, Mainland Trade Balance (CNH) (Dec)--

F: --

P: --

China, Mainland Imports YoY (USD) (Dec)--

F: --

P: --

China, Mainland Exports YoY (USD) (Dec)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

The US and Venezuela begin surprising diplomatic talks, hinting at a thaw in their long-strained relationship.

The United States and Venezuelan governments confirmed on Friday they are exploring the possibility of restoring diplomatic relations, signaling a potential shift in their historically strained relationship.

This development comes as a surprise, considering the Trump administration had previously stated its intent to influence Venezuela's leadership and control its oil sales following a potential removal of President Nicolas Maduro.

A small delegation of US diplomats and diplomatic security officials from the Trump administration arrived in Venezuela on Friday to begin discussions.

According to a statement from the US State Department, the team's primary objective is to conduct a preliminary assessment regarding the potential reopening of the US Embassy in Caracas.

Venezuela's government officially acknowledged the US delegation's presence and announced its own intention to send a delegation to the United States, though a specific date was not provided.

In a formal statement, the government of Delcy Rodríguez confirmed it "has decided to initiate an exploratory process of a diplomatic nature with the Government of the United States of America." The stated goal of these talks is "the re-establishment of diplomatic missions in both countries."

Just a week after President Donald Trump spoke of U.S. oil majors "going in and spending billions" to rebuild Venezuela's failing crude industry, his administration is clarifying a crucial detail: who pays. Washington is now signaling that American taxpayers will not directly fund the massive undertaking, even as top energy executives gather at the White House.

The President's initial comments fueled speculation that Washington might offer hefty financial guarantees or underwrite the risks for firms like Chevron, ExxonMobil, and ConocoPhillips to re-enter the politically volatile nation.

However, the administration has since shifted its emphasis, managing expectations about the level of direct government financial involvement.

On Friday, Interior Secretary Doug Burgum, who also heads the White House's National Energy Dominance Council, stated that the administration does not plan to use taxpayer money to underwrite the rebuilding of Venezuela's oil sector. He clarified that the necessary capital, estimated to be in the tens of billions over the next decade, must come from the companies themselves and private capital markets. The U.S. role, he suggested, would be to provide security and a stable operating environment, not direct funding.

Energy Secretary Chris Wright reinforced this position, noting that while institutions like the U.S. Export-Import Bank could offer credit support, companies have not yet requested direct government money.

This adjustment clarifies President Trump's earlier remarks, where he implied the government might backstop investments or allow companies to be reimbursed. The message from senior officials is now unambiguous: private capital is expected to carry the financial load.

To discuss this framework, the White House is hosting a high-level meeting with a wide array of global oil industry leaders. The guest list includes major U.S. and international players:

• Chevron

• ExxonMobil

• ConocoPhillips

• Continental Resources

• Halliburton

• HKN Energy

• Valero

• Marathon

• Shell

• Trafigura

• Vitol

• Repsol

• Eni

• Aspect Holdings

• Tallgrass

• Raisa Energy

• Hilcorp

Administration officials participating in the talks include Burgum, Wright, and Secretary of State Marco Rubio.

Any potential investment in Venezuela faces significant hurdles. Chevron is currently the only major U.S. producer with ongoing operations in the country, working under a special license. ExxonMobil and ConocoPhillips both left in the 2000s following the nationalization of their assets.

Industry leaders have been clear that a return would require strong legal, political, and financial guarantees from Washington to mitigate the decades of instability and expropriation risk.

Venezuela sits on one of the world's largest proven oil reserves, and a return to former production levels could reshape global crude markets and lower prices. However, the path forward is difficult. Decades of neglect have left the country's oil infrastructure in a state of disrepair. Compounding these operational challenges are significant political risks and geopolitical tensions, underscored by the U.S. seizing sanctioned tankers and controlling Venezuelan crude sales. Furthermore, current oil prices do not provide a strong incentive for the massive capital outlay required.

Ultimately, a genuine revival of Venezuela's oil sector will depend on private investment, supported by whatever assurances Washington can provide. Today's White House meeting is the first real test of whether that model is enough to convince the industry's key players to write the checks.

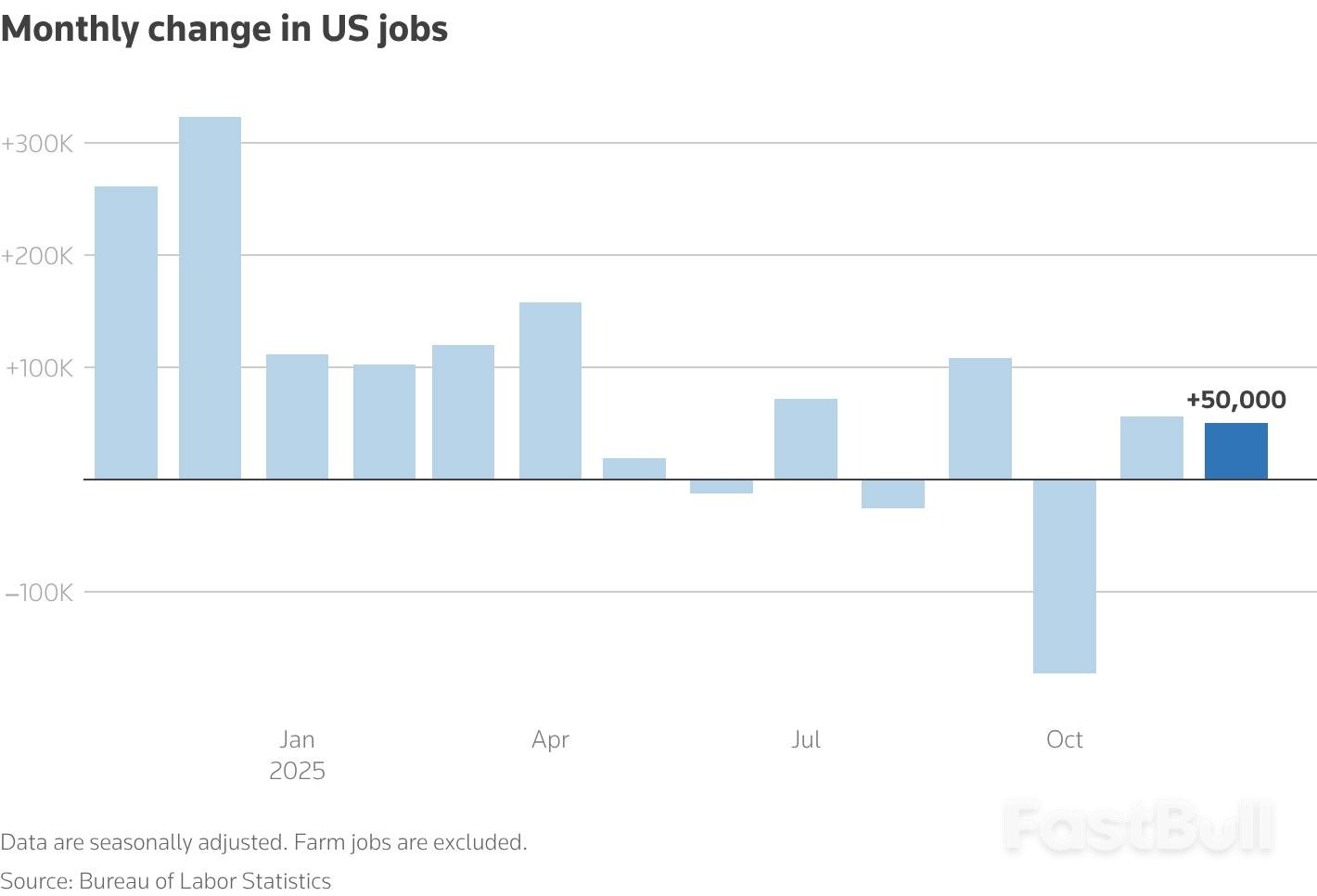

Richmond Fed President Tom Barkin characterized the latest employment data as a continuation of modest jobs growth within a low-hiring environment.

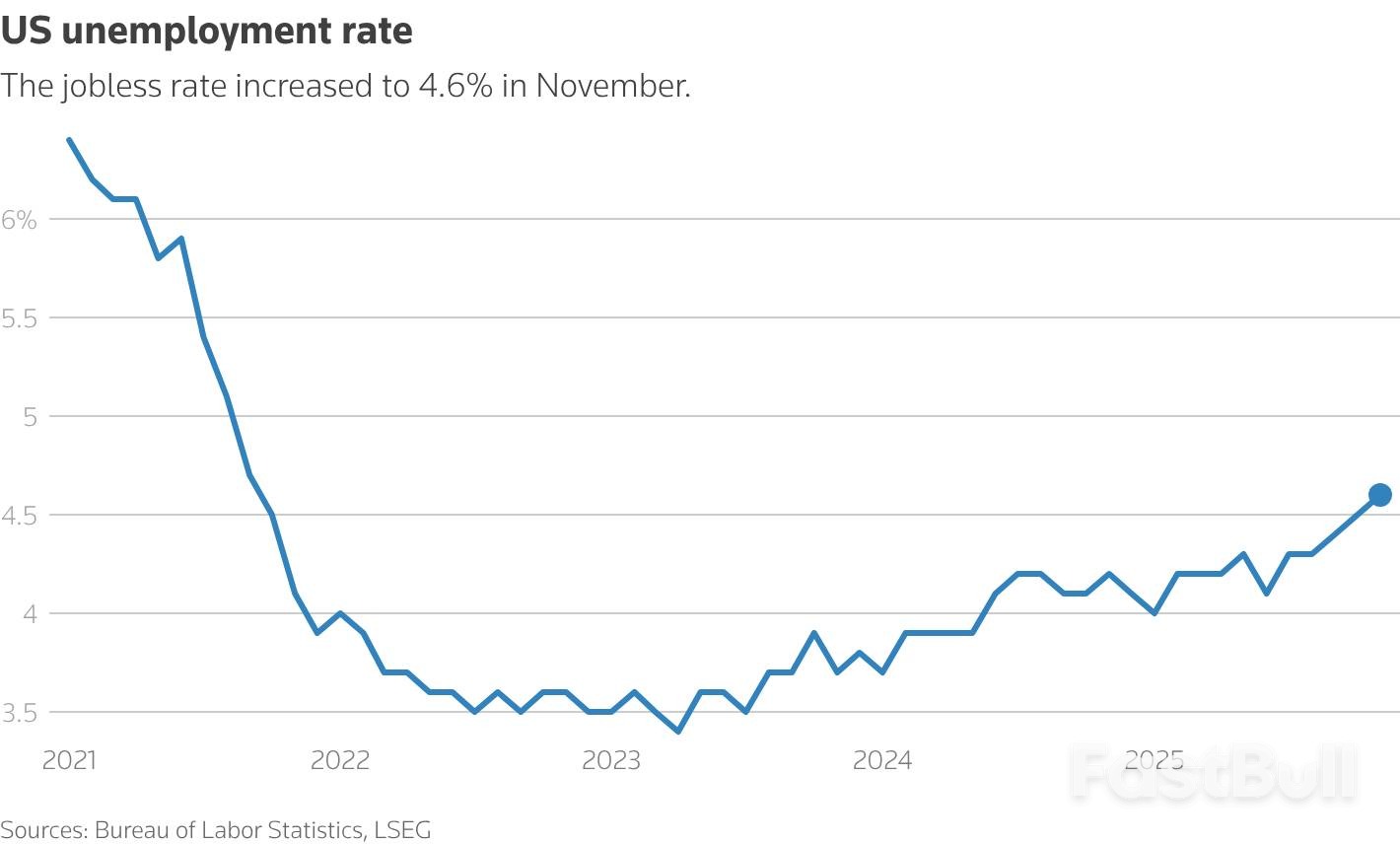

His comments followed a Bureau of Labor Statistics report showing that employers added 50,000 jobs last month, with the unemployment rate edging down to 4.4%.

"This fine balance between a modest job growth environment with a modest labor-supply growth environment seems to be continuing, and that was encouraging," Barkin told reporters on Friday.

According to the Richmond Fed chief, the current state of the jobs market is a reflection of two key factors: prevailing uncertainty among businesses and productivity gains that allow companies to operate with fewer new hires.

This landscape helps explain the restrained pace of hiring despite a relatively low unemployment rate.

Barkin emphasized that Federal Reserve policymakers must remain focused on the twin risks of rising unemployment and persistent inflation. The central bank cut its benchmark interest rate for the third consecutive time last month, but officials have signaled uncertainty about further reductions amid internal divisions over the economic outlook.

The challenge lies in balancing two conflicting trends.

On one hand, inflation remains a key concern. "Inflation has been above our target now for almost five years," Barkin noted. "It's in a lot better shape than it was two or three years ago, but it's certainly not all the way there."

On the other hand, the labor market is showing signs of cooling. "The unemployment rate has ticked up in the last year, and job growth is modest," he said.

This delicate situation requires careful monitoring from the central bank. "So I think you've got to watch both of them," Barkin concluded.

U.S. employment growth slowed more than anticipated in December, with notable job losses in construction, retail, and manufacturing. However, a surprising dip in the unemployment rate to 4.4% suggests the labor market isn't collapsing, creating a mixed picture for the economy.

The latest employment report also revealed solid wage growth, reinforcing expectations that the Federal Reserve will likely hold interest rates steady at its upcoming meeting on January 27-28.

Nonfarm payrolls rose by only 50,000 jobs last month, falling short of the 60,000 gain economists had forecast. This comes after November's figure was revised downward to a 56,000 increase.

The data for previous months shows a weakening trend. Job losses in October were revised to 173,000, the largest drop in nearly five years, primarily due to federal government buyouts. Over the last three months, the economy has lost an average of 22,000 jobs per month, highlighting a significant loss of momentum.

The full-year data paints a stark picture. In 2025, only 584,000 jobs were created, averaging just 49,000 per month. This is less than a third of the 2 million jobs added in 2024, which saw an average monthly gain of 168,000. Economists describe the current environment as a "low-hire, low-fire" labor market.

Job growth in December was concentrated in a few key areas, with the share of industries reporting hiring falling from 55.6% to 50.8%.

Gaining Sectors:

• Restaurants and Bars: +27,000 jobs

• Healthcare: +21,000 jobs

• Social Assistance: +17,000 jobs

• Federal Government: +2,000 jobs

Losing Sectors:

• Retail: -25,000 jobs

• Construction: -11,000 jobs

• Manufacturing: -8,000 jobs

Manufacturing employment fell by 68,000 over the past year, a decline some economists link to the Trump administration's tariffs. The retail sector's losses were driven by weak holiday season hiring. Job losses were also recorded in mining, wholesale, transportation and warehousing, and professional and business services.

Economists point to several factors driving the slowdown. President Donald Trump's trade and immigration policies are seen as reducing both the demand for and supply of workers. At the same time, businesses are investing heavily in artificial intelligence, making them uncertain about future staffing needs and cautious about hiring.

This has led to a "jobless expansion," where economic growth and worker productivity surge—as seen in the third quarter—without a corresponding increase in employment. Lydia Boussour, a senior economist at EY-Parthenon, noted that "persistent policy headwinds weighed on business sentiment and curtailed hiring."

Despite the hiring slowdown, businesses are not cutting pay. Wages increased 3.8% year-over-year in December, up from 3.6% in November. This solid wage growth is seen as a sign of worker shortages in certain industries.

This dynamic makes the Federal Reserve's job more complex. The combination of a low unemployment rate and rising wages gives the central bank little reason to cut its benchmark interest rate, which currently stands at a 3.50%-3.75% range after a quarter-point cut in December. Financial markets now expect the Fed to remain on hold beyond this month's meeting, as rate cuts may be less effective at stimulating job growth if the underlying issues are structural rather than cyclical.

Following the report, U.S. stocks traded higher, the dollar strengthened, and longer-term Treasury yields fell.

The labor market may be even more fragile than current figures suggest. The Bureau of Labor Statistics (BLS) is set to publish its annual payrolls benchmark revision next month. The agency has already estimated that about 911,000 fewer jobs were created in the 12 months through March 2025 than initially reported.

This overcounting has been blamed on the BLS's "birth-death" model, which estimates job creation from new and closed businesses. The BLS plans to change this model starting in January to incorporate more current data.

Alongside the December report, the BLS published revisions to household survey data, from which the unemployment rate is calculated. November's unemployment rate was revised down to 4.5% from 4.6%. The dip to 4.4% in December was due to a drop in the labor force combined with a rise in household employment.

However, some underlying details show weakness. The number of people experiencing long-term unemployment increased, and the median duration of joblessness jumped to a four-year high of 11.4 weeks. Oscar Munoz, chief U.S. macro strategist at TD Securities, expects these dynamics will "continue to push the unemployment rate higher through the first quarter of 2026."

Economic

Traders' Opinions

Russia-Ukraine Conflict

Daily News

Remarks of Officials

Commodity

Political

Energy

Middle East Situation

Oil prices climbed on Friday, pushing crude benchmarks toward a weekly gain fueled by growing concerns over global supply. Escalating civil unrest in Iran and intensified attacks in the Russia-Ukraine war are putting traders on edge.

By 12:41 p.m. ET, Brent futures were up $1.58, or 2.55%, trading at $63.57 per barrel. U.S. West Texas Intermediate (WTI) crude saw a similar rise of $1.60, or 2.77%, to reach $59.36.

Both benchmarks had already jumped over 3% on Thursday, reversing two consecutive days of losses. For the week, Brent is on pace to gain 4.6%, while WTI is tracking a 3.5% increase.

Two major geopolitical flashpoints are driving fears of potential supply disruptions.

Intensifying Unrest in Iran

The market is closely watching an "uprising in Iran," according to Phil Flynn, a senior analyst with the Price Futures Group. Protests over economic hardship have spread across the country, including in Tehran, Mashhad, and Isfahan.

Ole Hansen, head of commodity analysis at Saxo Bank, noted that the protests "seem to be gathering momentum, leading the market to worry about disruptions." The situation escalated on Thursday when internet monitoring group NetBlocks reported a nationwide internet blackout.

These concerns are backed by data. A recent survey showed that the Organization of the Petroleum Exporting Countries (OPEC) pumped 28.40 million barrels per day (bpd) last month, a decrease of 100,000 bpd from November. Iran and Venezuela posted the largest production declines.

Russia-Ukraine War Escalation

Adding to supply anxiety, Russia’s military announced Friday that it had fired its hypersonic Oreshnik missile at targets in Ukraine. The Russian defense ministry specified that the strikes targeted energy infrastructure that supports Ukraine's military-industrial complex.

In a separate development, the White House is scheduled to meet with oil companies and trading houses Friday afternoon to negotiate Venezuelan export deals. The meeting follows the capture of Venezuelan President Nicolas Maduro on Saturday.

U.S. President Donald Trump has demanded that Washington be given full access to Venezuela's oil sector. U.S. officials have stated their intention to control the country's oil sales and revenue indefinitely.

Oil major Chevron Corp, along with global trading firms Vitol and Trafigura, are among those competing for government deals. The contracts concern the marketing of up to 50 million barrels of oil that state-run company PDVSA accumulated in inventories during a severe embargo.

"The market will focus on the outcome in the coming days for how the Venezuelan oil in storage will be sold and delivered," said Tina Teng, a market strategist at Moomoo ANZ.

Despite the bullish geopolitical news, some analysts urge caution. According to Haitong Futures, global oil inventories are rising, and a potential oversupply could cap further price increases.

The firm suggests that unless the risks surrounding Iran escalate significantly, the current rebound in oil prices is likely to be limited and may struggle to be sustained.

President Trump's meeting with oil executives on Friday is stirring major tensions within the U.S. energy sector. Independent shale drillers are voicing sharp criticism, warning that the administration's push to revive Venezuela's oil industry could devastate American producers by flooding the market and driving down crude prices.

While major oil bosses are meeting with the president, many smaller shale leaders, who were not invited, feel the White House is abandoning domestic energy producers. The sentiment is that a potential influx of Venezuelan crude works directly against their interests.

"We're talking about this administration screwing us over again," one senior executive stated, calling the potential policy "against American producers." Another warned, "If the US government starts providing guarantees to oil companies to produce or grow oil production in Venezuela I'm going to be . . . pissed."

This frustration runs deep in Texas, where many oil executives who had previously backed Trump now describe the strategic shift as a "betrayal."

Kirk Edwards, CEO of Latigo Petroleum, captured the mood succinctly: "To me, the signal from the administration is: we'd rather spend our American money on propping up a Venezuelan oil business than supporting our current independent businesses."

The domestic oil industry is already navigating a difficult economic landscape. The number of active U.S. rigs has dropped to 412, a 15% decrease over the past year. Furthermore, the Energy Information Administration (EIA) projects that U.S. oil output will fall in 2026, marking the first annual decline since the pandemic.

With West Texas Intermediate (WTI) trading below $56 a barrel, many shale producers are struggling, as they often require prices above $60 to break even. This financial strain makes the prospect of new supply from Venezuela particularly alarming.

The administration's calculus appears tied to domestic politics. With the midterm elections approaching, President Trump has made it clear he wants cheaper oil and gasoline for consumers. Adding to supply-side pressures, OPEC producers are also increasing their output.

U.S. Energy Secretary Chris Wright projected that Venezuela's oil production could increase by 50% within a year. "I think you'll see more downward pressure on the price of gasoline," he told Fox News.

However, shale executives are skeptical, suggesting Wright is now "just toeing the party line." The frustration ultimately centers on Trump, with one Midland-based executive noting, "He's definitely not pro oil as far as independent oil companies' survival and vibrancy." He added that the real impact will become clear when "US production [starts] declining."

Financial markets are already reacting to the potential policy shift. This week, shares of prominent energy firms like Diamondback Energy, APA Corp, and Devon Energy fell by as much as 9%.

"Somebody's looking at these stocks today going, why would I own this if in a few years, they're going to be competing against Venezuela for oil, for our refineries in the United States?" Edwards questioned, highlighting rising investor uncertainty.

Outrage grew after President Trump suggested that taxpayer money could be used to reimburse companies investing in Venezuela. "We should not subsidise the big companies in trying to retool Venezuela's infrastructure and develop their reserves for them," said another shale executive. He added that Trump seems content to see independent producers "drill their way into oblivion" and doesn't "give a damn if they went bankrupt."

Analysts note that this environment favors the industry's largest players. "All of this points to the advantage of being larger," said Maynard Holt of Veriten. "Because many of the opportunities that are coming—whether it's Venezuela or Algeria or some other complicated place—you will be able to consider them more seriously the larger you are."

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up