Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Donald Trump threatens to sue JPMorgan Chase for "debanking" him post-January 6, denying a Fed chief offer to CEO Jamie Dimon.

Donald Trump has threatened to sue JPMorgan Chase & Co., accusing the banking giant and its CEO Jamie Dimon of "debanking" him following the Capitol riot on January 6, 2021.

The former president’s statement, made in a social media post on Saturday, was a direct response to a Wall Street Journal story. The report claimed Trump had offered Dimon the position of Federal Reserve chief several months ago, an offer Dimon reportedly interpreted as a joke.

"There was never such an offer," Trump wrote. "In fact, I'll be suing JPMorgan Chase over the next two weeks for incorrectly and inappropriately DEBANKING me after the January 6th Protest."

Trump did not provide further details on the planned lawsuit. JPMorgan did not immediately issue a comment on the matter.

This isn't the first time Trump has leveled these accusations against the bank. In August, he claimed JPMorgan "discriminated against me very badly," alleging the firm asked him to close accounts he had maintained for decades. Trump asserted that this action was linked to his supporters storming the Capitol to prevent the certification of Joe Biden’s 2021 election victory.

JPMorgan has previously acknowledged it is facing reviews, investigations, and legal proceedings connected to the broader political fight over "debanking."

In the past, Dimon has directly pushed back against claims that the bank's decisions are politically biased. "We do not debank people's religious or political affiliations," he told Fox Business in December.

Jamie Dimon has made his own position on a potential government role clear. When asked about leading the central bank at a U.S. Chamber of Commerce event on Thursday, Dimon was unequivocal.

"Chairman of the Fed, I'd put in the absolutely, positively no chance, no way, no how, for any reason," he stated.

However, he expressed openness to a different cabinet position, noting that if offered the job of running the Treasury, "I would take the call."

The public exchange highlights ongoing friction over the Federal Reserve's independence. Dimon recently criticized attacks on the institution, warning that "chipping away at Fed independence is not a great idea" and could ultimately result in higher inflation and interest rates. His comments followed actions by the Justice Department, including criminal subpoenas related to the renovation of the Fed's headquarters.

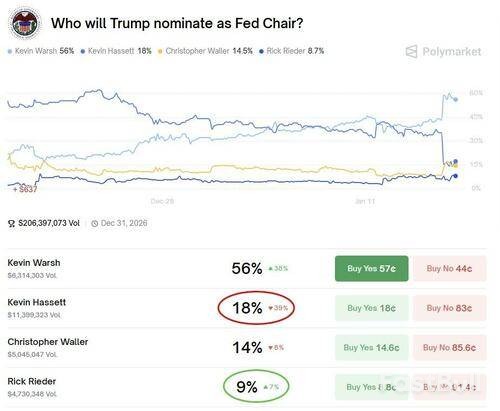

Meanwhile, the question of who would lead the central bank under a new Trump administration remains open. Fed Chair Jerome Powell's term ends in May. On Friday, Trump confirmed he has a successor in mind but declined to name the individual.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up