- USDJPY

- XAUUSD

- XAGUSD

- WTI

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Thailand's cheap assets are overlooked as global investors doubt its election will reform a struggling economy.

Thailand's sluggish economy has pushed its stocks and bonds into a precarious position: cheap, overlooked, and increasingly off the radar for global capital. With a general election this weekend, major money managers are signaling caution, viewing the vote as more likely to worsen existing challenges than to solve them.

Persistent issues like high household debt and weak growth have already taken their toll. In the past year, Thai stocks were among the world's worst performers, while its bonds lagged most emerging market peers in 2026. Investors see little reason to believe the country's fourth leader in three years can deliver the reforms needed to fix poor governance and policy drift.

The market consensus points to a steeper yield curve, driven by potential interest rate cuts and government spending, while equities remain depressed as capital seeks opportunities elsewhere.

"Thailand does look cheap in terms of valuations," said Christopher Leow, chief investment officer at Principal Asset Management in Singapore. "But looking cheap is probably not enough."

The sentiment is clear among institutional investors, who are limiting their exposure ahead of the election.

• T Rowe Price Group Inc. has reduced its bond holdings and remains cautious on local currency debt, waiting for clear policy direction before committing more capital.

• Allianz Global Investors holds a broadly underweight allocation but is considering a shift into longer-duration bonds.

• Aberdeen is favoring defensive stocks and exporters to minimize exposure to the domestic Thai economy, warning that a fragile coalition government could lead to uneven policy execution.

"For lasting investor confidence, the election is only the starting point," said Nattanont Arunyakananda, an investment manager at Aberdeen in Bangkok. He stressed that the outlook depends on credible reforms and sustained fiscal and monetary support. "Without reforms that lift productivity and improve the investment climate, any post-election bounce is likely to remain tactical rather than structural."

Historically, Thai markets have seen a brief lift after elections. Over the past three votes, the benchmark Stock Exchange of Thailand (SET) Index gained an average of 3.3% in the month following the polls. However, these rallies often fade as political realities set in.

The ongoing worries are forcing a rethink of Thai assets in international portfolios. Once valued for their exposure to global growth, they have lost appeal due to a stagnant economy, weak tourism, and recurring political instability.

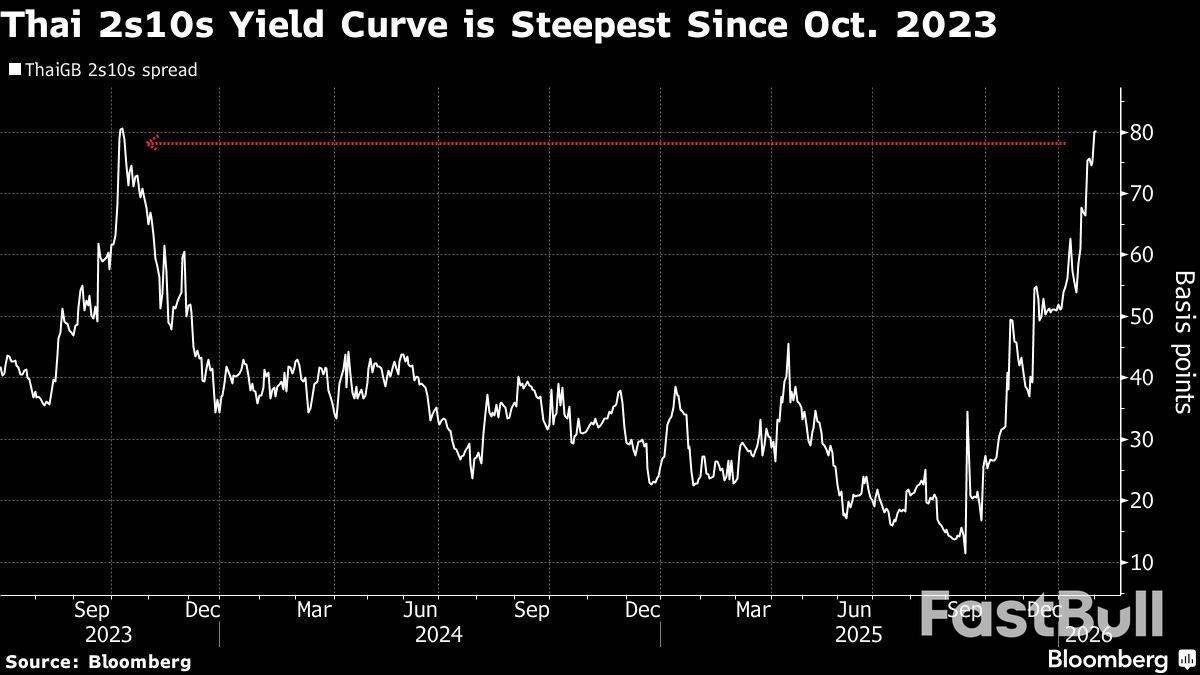

A key concern is the expected rise in debt issuance needed to fund campaign promises from leading political parties. With the central bank forecasting economic growth of just 2.2% in 2025—trailing regional peers—the government has already approved a US$1.4 billion food and services subsidy program.

These additional spending pledges have helped push the spread between Thailand's two- and 10-year bond yields to its widest point since October 2023.

"We'll be looking for them to invest into unleashing the potential of the economy," said Leonard Kwan, a portfolio manager at T Rowe Price in Hong Kong. While Thailand has some fiscal capacity, he added, "the key question is effectiveness in how they utilize it."

Despite the bearish outlook, some signs of value are emerging. Thai stocks are trading at around 14 times forward earnings, which is below both their five-year average and a gauge of regional peers. The steepening yield curve, with expectations of higher fiscal spending already priced in, may also present opportunities at the long end.

BlackRock Inc., while holding less exposure than a year ago, has recently begun buying more bonds with longer maturities, according to Navin Saigal, its Asia Pacific head of fundamental fixed income in Singapore.

Ultimately, investors are watching to see if the election will be followed by meaningful reforms or if policy will be watered down by the compromises needed to form a government. The frequent turnover in political leadership is also dimming hopes for lasting change.

"With no clear majority for any single party in sight, it's hard to envisage a sharp turn in investor confidence," said Wai Kiat Soh, a portfolio manager at Ninety One in Singapore. "The 'muddle-through' scenario will likely play out once again."

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up