- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Japan's top banks eye record profits, driven by domestic interest rate hikes and robust corporate lending.

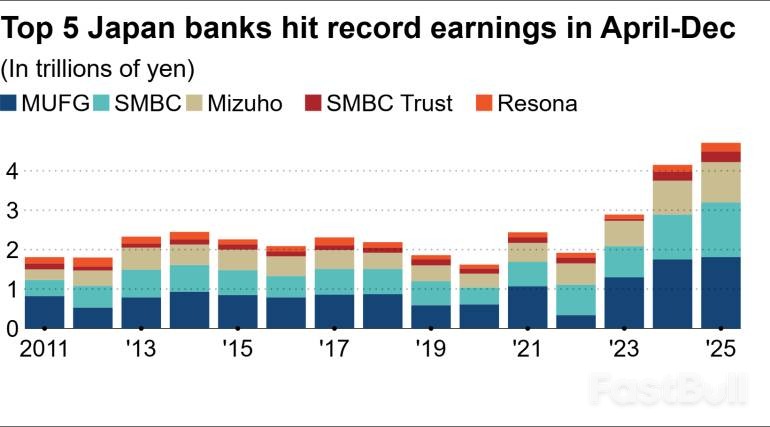

Japan’s three largest commercial banks are on track for a third consecutive year of record-breaking full-year profits, driven by a surge in lending income from higher domestic interest rates.

Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Financial Group (SMFG), and Mizuho Financial Group collectively generated a record 4.22 trillion yen ($26.9 billion) in net profit for the April-December 2025 period, a 13% increase from the previous year. All three have maintained their earnings forecasts for the full fiscal year.

The banking giants are projected to achieve a total net profit of 4.73 trillion yen for the year ending in March. This would represent 9% of the total net profit from all companies listed on the Tokyo Stock Exchange's Prime market, an increase of 1.6 percentage points from the prior year.

MUFG reported a 4% year-on-year rise in its consolidated net profit to 1.81 trillion yen for the nine-month period, marking its third straight record for that timeframe. The bank cited higher interest rates boosting deposit and loan revenue, growing fee income, and strong performance from its U.S. partner Morgan Stanley.

SMFG and Mizuho also delivered record profits. When including Sumitomo Mitsui Trust Group and Resona Holdings, Japan's five largest banks saw their combined net profits climb 14% to 4.71 trillion yen, setting a new high for the third year in a row.

The primary catalyst for this performance has been the Bank of Japan's interest rate hikes. The BOJ's most recent move in December 2025 raised the policy rate by 25 basis points to 0.75%. This series of rate increases, which began with the end of the negative interest rate policy in March 2024, is expected to boost the megabanks' combined net interest income by an estimated 700 billion yen for the full year ending March 2026.

Higher market rates have successfully widened the banks' interest spreads—the difference between what they charge for loans and what they pay on deposits. For the April-December 2025 period, the average interest spread at the megabanks reached 1.04 percentage points, the highest level in 11 years. As a result, their combined net interest income from lending and other sources grew 17% to a new high of 3.81 trillion yen.

Robust demand for capital from the corporate sector provided another significant tailwind. As of the end of December 2025, the total loan balance across the three megabanks had increased by 3% from the previous year. This growth was driven by strong demand for financing related to mergers and acquisitions as well as real estate projects.

This activity also translated into higher fee income. Combined profits from fees and commissions, including loan origination and M&A advisory services, rose 9% year-on-year to a record 1.6 trillion yen.

While rising interest rates are beneficial for lending profits, they create headwinds for bond portfolios by decreasing their market value. By the end of December, the megabanks held a combined 748.6 billion yen in unrealized losses on their domestic bond holdings, a 33% increase over just three months.

However, the impact on earnings is expected to be limited. The banks proactively managed this risk by shortening the maturities of their securities. Furthermore, their unrealized gains on stock holdings provided a substantial cushion, rising 11% in three months to approximately 8 trillion yen. Overall, their combined securities portfolios held unrealized gains of around 8.5 trillion yen.

Looking ahead, the banks face several challenges. Although the non-performing loan ratio remains low across all three institutions, a key focus will be the impact of a higher interest burden on borrowers.

Attracting enough deposits to fund lending growth is another critical task. The combined domestic deposit balance for the three banks grew by only 0.6% year-on-year as of December 2025. Corporate clients are increasingly moving funds into financial products with higher yields. In response, banks are expected to enhance their efforts to attract both retail and corporate deposits by improving digital services and raising interest rates on fixed-term accounts.

Despite these potential hurdles, all three megabanks have maintained their full-year earnings forecasts for the year ending March 2026. Having already achieved roughly 90% of their profit targets by December, they appear confident but have factored in allowances for potential market uncertainty and geopolitical risks.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up