- EURUSD

- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

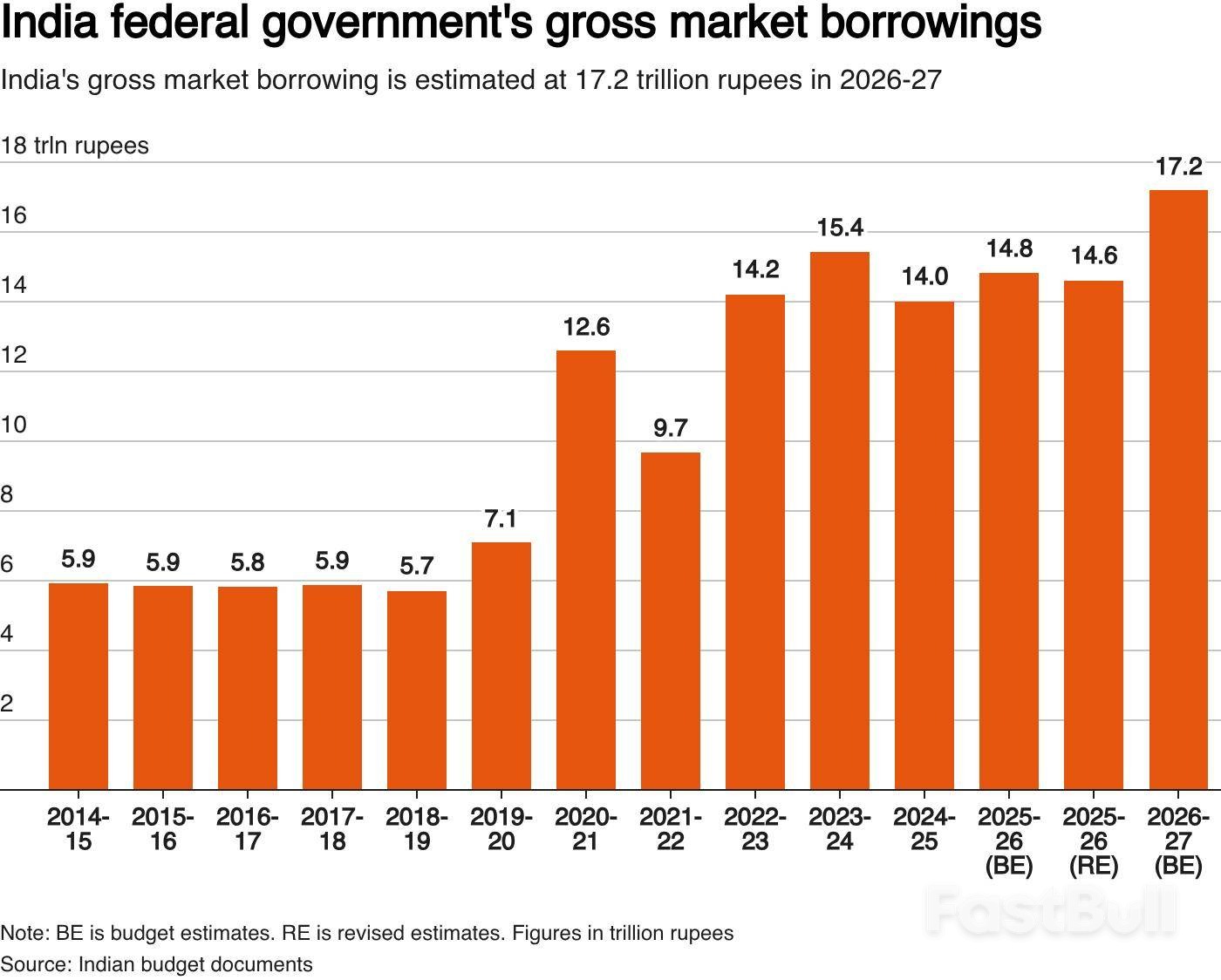

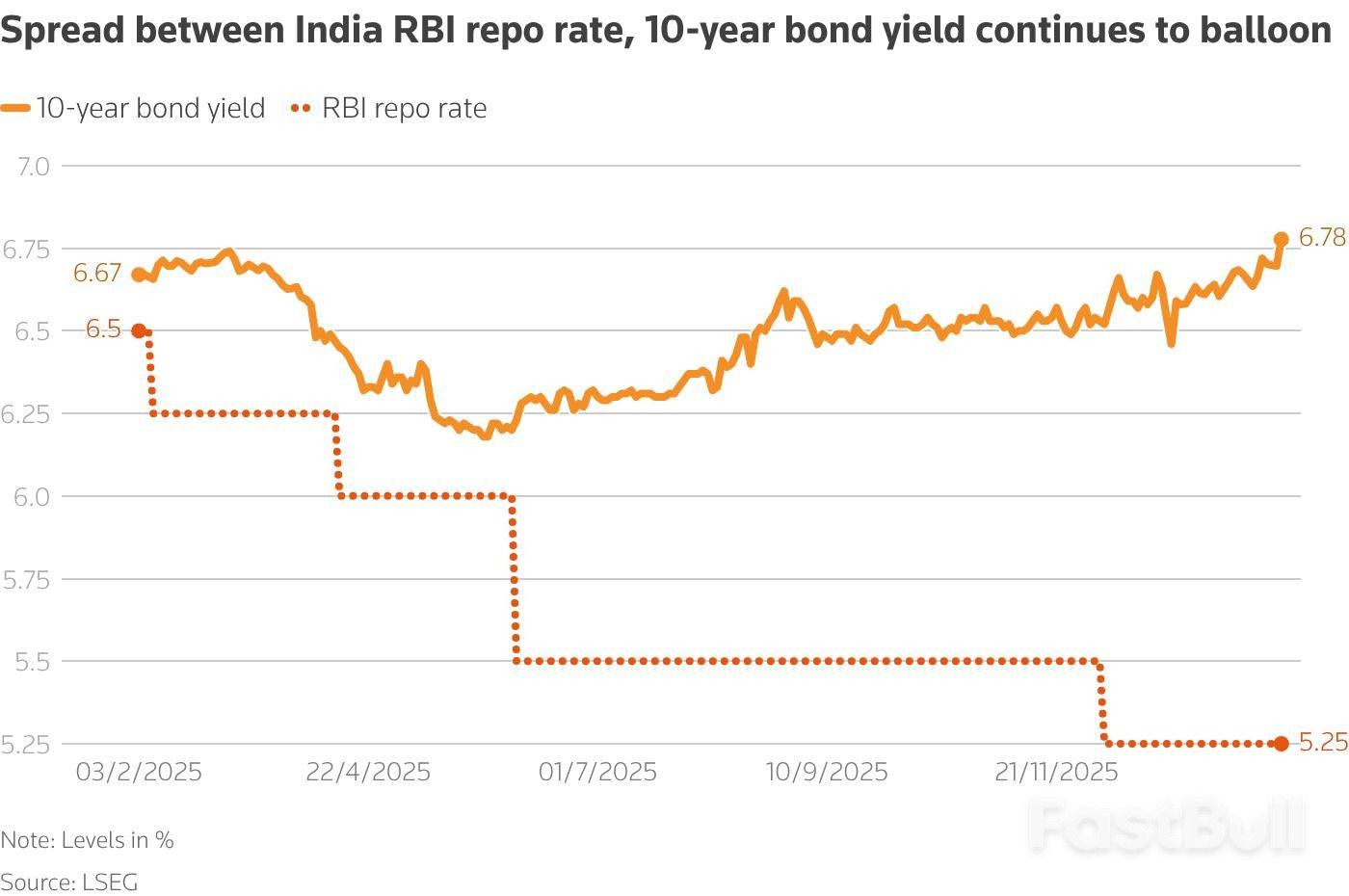

Indian bonds plummeted, with yields soaring to a year-high, amid record government borrowing that challenges central bank policy.

Indian government bonds sold off sharply following the federal budget, with the 10-year benchmark yield hitting its highest level in nearly a year. The market slump was driven by the government's announcement of a record-high borrowing program, which has weakened already fragile investor sentiment.

The government plans to borrow a gross 17.2 trillion rupees ($187.5 billion) in the next fiscal year, which runs from April through March. This news immediately pushed bond prices down and yields up.

The yield on the benchmark 6.48% 2035 bond jumped 8 basis points to 6.78% on Monday, a peak not seen since last March. This move comes as the market grapples with a lack of investor appetite and recent losses on trading portfolios.

Even before the budget announcement, the market showed signs of stress. The 10-year benchmark yield had already risen by around 20 basis points between December and January, despite a 25 basis point policy rate cut and significant debt purchases by the central bank.

The 10-year government bond yield is a crucial economic indicator because it serves as a benchmark for borrowing costs across the country. When this yield rises, it creates several challenges:

• Higher Costs for Companies and States: Both corporate and state-level borrowing becomes more expensive, as their loan rates are priced relative to government bonds.

• Increased Government Debt Burden: The government itself must pay more to finance its operations, straining public finances.

• Complicates Central Bank Policy: The Reserve Bank of India (RBI) has been cutting policy rates to support economic growth. Rising market yields work against these efforts, making monetary policy less effective.

Market analysts are now expressing caution and looking to the central bank for support.

"We remain cautious on bonds, (and) despite the recent cheapening, we do not advocate long positions here and think the 10-year can push closer to 7% near term," said Nathan Sribalasundaram, Asia rates strategist at Nomura. He noted that while the RBI remains the "marginal buyer," the central bank has a low bar for announcing further bond purchases through Open Market Operations (OMOs).

Dhiraj Nim, an economist at ANZ, shared a similar view on the RBI's role. "With macro factors likely to dampen the private sector's bond demand, the RBI is expected to use open market operations to boost liquidity and manage borrowing costs simultaneously," he said.

With the market under pressure, all eyes are on the Reserve Bank of India's monetary policy decision this Friday. While another rate change is not expected, traders and investors are anxiously awaiting any announcements about liquidity injections or new bond-buying programs designed to stabilize the market.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up