Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

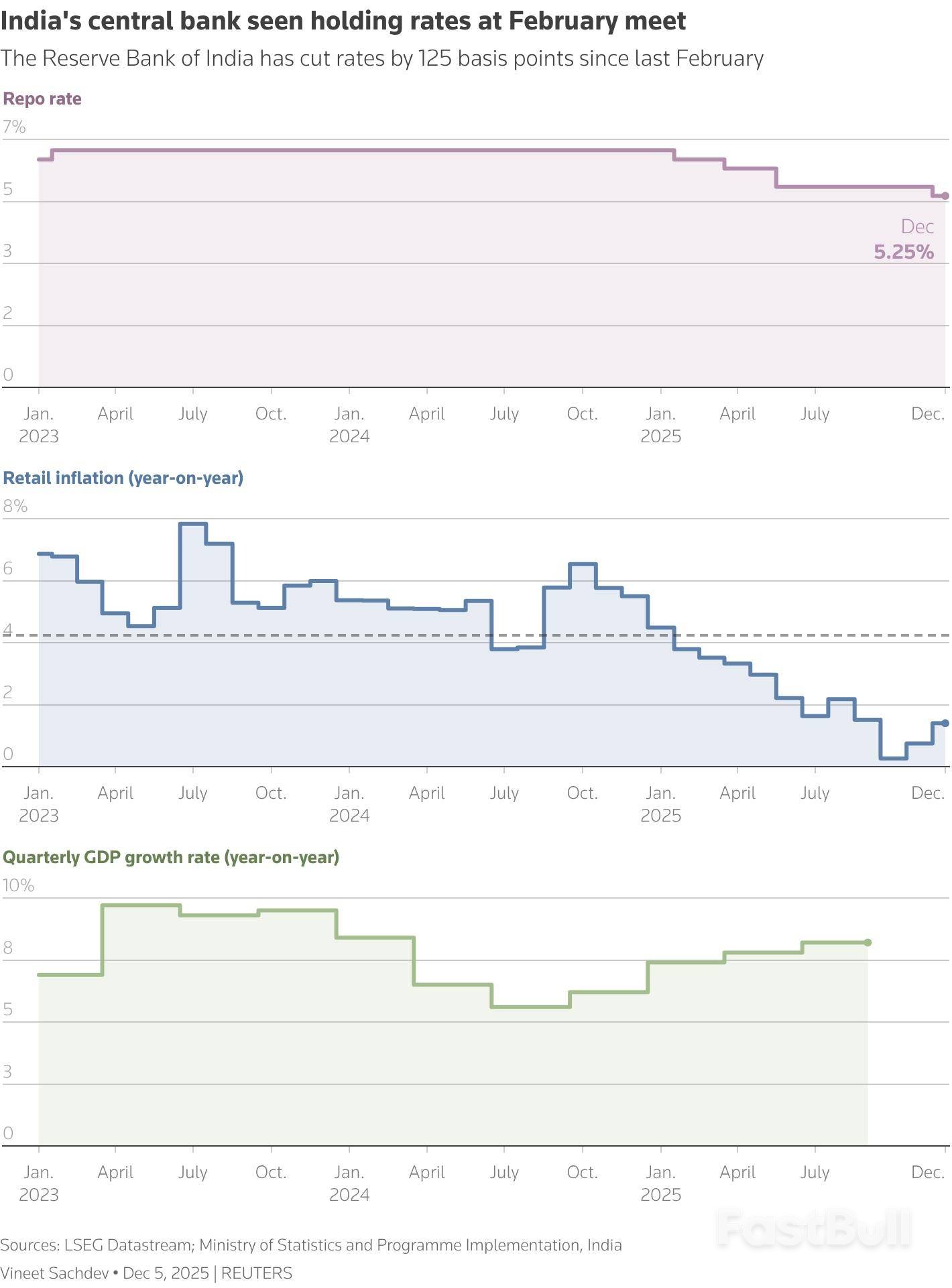

RBI pauses rates, focusing on stalled transmission and market pressures. Bond purchases are anticipated.

The Reserve Bank of India (RBI) is widely expected to hold its key interest rate steady on Friday, shifting its focus from further cuts to ensuring its previous monetary easing effectively filters through the economy. A new U.S.–India trade deal has eased immediate pressure on the central bank to provide more stimulus.

A Reuters poll conducted before the trade deal was announced showed a strong consensus, with 59 of 70 economists anticipating no change in rates. While a minority had called for another cut due to low inflation and U.S. tariff risks, the trade agreement has reinforced the case for a policy pause.

Dhiraj Nim, an economist at ANZ Bank, noted, "The U.S.-India trade deal further bolsters the case for the RBI keeping rates unchanged this week."

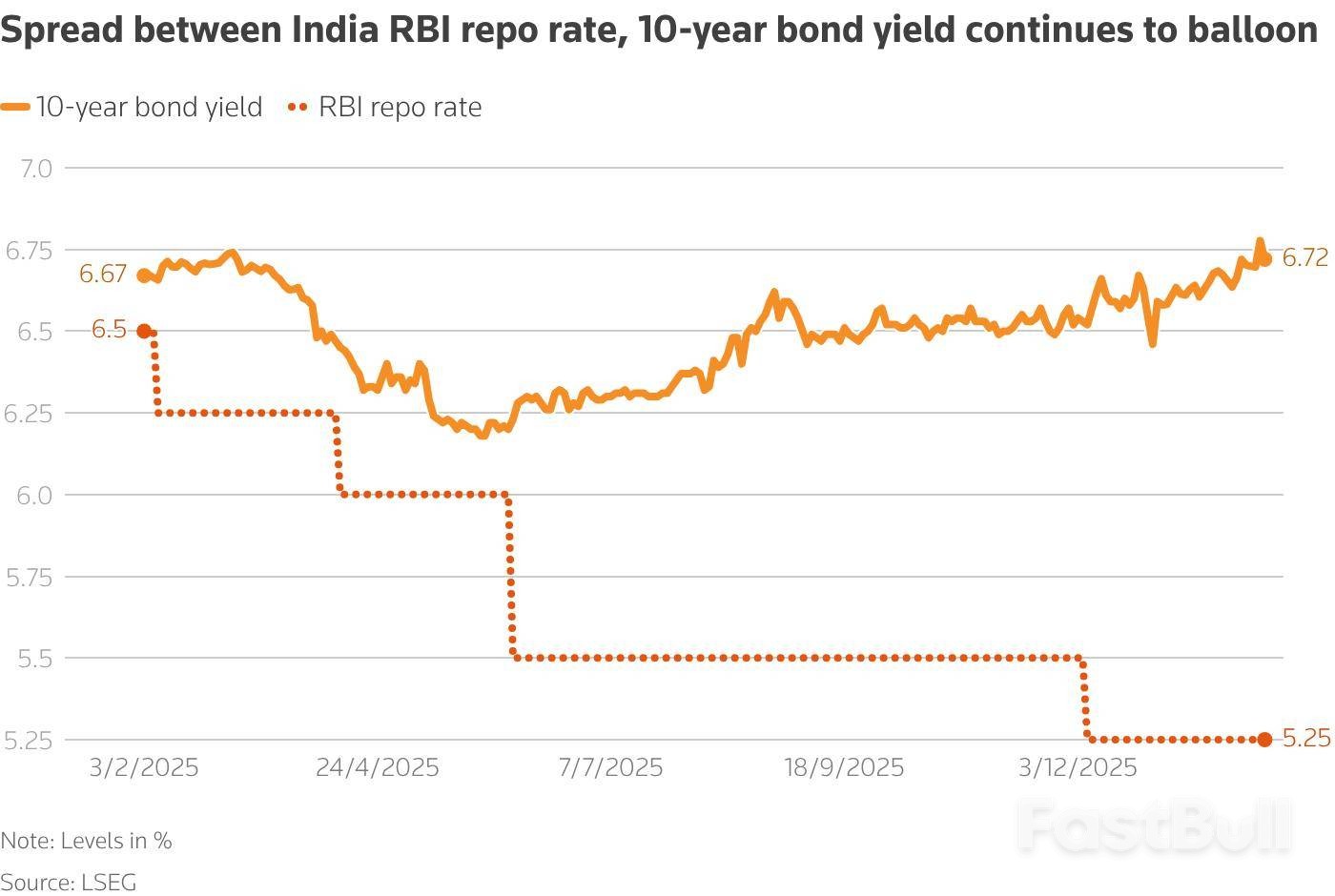

Since last February, the RBI has already cut its policy repo rate by a total of 125 basis points, bringing it down to 5.25%.

The decision to hold rates is supported by India's strong economic performance. RBI Governor Sanjay Malhotra described the economy as being in a "Goldilocks phase" at the last policy meeting in December.

Official forecasts reflect this optimism:

• GDP growth is projected to hit 7.4% in the current financial year.

• The government's economic adviser anticipates growth between 6.8% and 7.2% for the next fiscal year.

• The RBI’s own forecast for the fiscal year ending March 31 was 7.3% growth with CPI inflation at 2%.

This backdrop of steady growth and controlled inflation gives the central bank room to observe the impact of its past actions.

Despite the aggressive rate cuts over the past year, the benefits have not fully reached borrowers. The primary challenge for the RBI is now "policy transmission"—ensuring its lower rates translate into lower funding costs across the financial system.

A key indicator of this disconnect is the benchmark 10-year government bond yield, which has barely fallen. This yield serves as a reference for pricing corporate and bank loans, and its stickiness has kept borrowing costs high, limiting the economic boost from the RBI's easing.

"The challenge now is to ensure that transmission of previous rate cuts is not hampered, while the central bank remains on an extended pause," said Kaushik Das, chief economist for India, Malaysia, and South Asia at Deutsche Bank.

The bond market has been under significant pressure from multiple fronts. To manage foreign capital outflows from equity markets prior to the trade deal, the RBI sold $30 billion from its foreign exchange reserves between September and November. This intervention drained rupee liquidity from the system, adding to the strain on bond markets already grappling with record government borrowings.

To counter these pressures and improve policy transmission, analysts expect the RBI to increase its open market bond purchases by at least 1 trillion rupees ($10.92 billion). This move would inject liquidity into the market, ease the strain, and help bring down yields.

The need for RBI support has grown more urgent following the announcement of a higher-than-expected government borrowing program for the upcoming fiscal year. As economists at Nomura stated, "Higher market borrowing numbers mean concerns around bond supply will remain a challenge for policy transmission."

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up