Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

U.S. Initial Jobless Claims 4-Week Avg. (SA)

U.S. Initial Jobless Claims 4-Week Avg. (SA)A:--

F: --

U.S. EIA Weekly Natural Gas StocksA:--

F: --

P: --

U.S. Kansas Fed Manufacturing Production Index (Jul)A:--

F: --

P: --

U.S. Kansas Fed Manufacturing Composite Index (Jul)A:--

F: --

P: --

ECB President Lagarde Speaks Treasury Sec Yellen Speaks U.S. Weekly Treasuries Held by Foreign Central Banks

ECB President Lagarde Speaks Treasury Sec Yellen Speaks U.S. Weekly Treasuries Held by Foreign Central BanksA:--

F: --

P: --

Japan Tokyo CPI MoM (Excl. Food & Energy) (Jul)

Japan Tokyo CPI MoM (Excl. Food & Energy) (Jul)A:--

F: --

P: --

Japan Tokyo CPI YoY (Excl. Food & Energy) (Jul)A:--

F: --

P: --

Japan Tokyo Core CPI YoY (Jul)A:--

F: --

P: --

Japan Tokyo CPI YoY (Jul)A:--

F: --

P: --

Japan Tokyo CPI MoM (Jul)A:--

F: --

P: --

Italy Average Hourly Wage MoM (Jun)

Italy Average Hourly Wage MoM (Jun)A:--

F: --

P: --

Russia Key Rate

Russia Key RateA:--

F: --

P: --

India Deposit Gowth YoY

India Deposit Gowth YoYA:--

F: --

P: --

Mexico Trade Balance (Jun)

Mexico Trade Balance (Jun)A:--

F: --

P: --

U.S. Core PCE Price Index YoY (Jun)A:--

F: --

P: --

U.S. Core PCE Price Index MoM (Jun)A:--

F: --

P: --

U.S. Personal Outlays MoM (SA) (Jun)A:--

F: --

U.S. PCE Price Index MoM (Jun)A:--

F: --

P: --

U.S. PCE Price Index YoY (SA) (Jun)A:--

F: --

P: --

U.S. Real Personal Consumption Expenditures MoM (Jun)A:--

F: --

U.S. Personal Income MoM (Jun)A:--

F: --

U.S. UMich Consumer Expectation Index Final (Jul)A:--

F: --

P: --

U.S. UMich 1-Year Inflation Expectations Final (Jul)A:--

F: --

P: --

U.S. UMich Consumer Confidence Index Final (Jul)A:--

F: --

P: --

U.S. UMich Current Status Index Final (Jul)A:--

F: --

P: --

Canada Federal Government Budget Balance (May)

Canada Federal Government Budget Balance (May)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

China, Mainland Industrial Profit YoY (YTD) (Jun)

China, Mainland Industrial Profit YoY (YTD) (Jun)A:--

F: --

P: --

Germany Actual Retail Sales MoM (May)

Germany Actual Retail Sales MoM (May)--

F: --

U.K. BOE Mortgage Lending (Jun)

U.K. BOE Mortgage Lending (Jun)--

F: --

P: --

U.K. M4 Money Supply YoY (Jun)--

F: --

P: --

U.K. BOE Mortgage Approvals (Jun)--

F: --

P: --

U.K. M4 Money Supply MoM (Jun)--

F: --

P: --

U.K. M4 Money Supply (SA) (Jun)--

F: --

P: --

U.K. CBI Distributive Trades (Jul)--

F: --

P: --

U.K. CBI Retail Sales Expectations Index (Jul)--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

U.S. Dallas Fed PCE Price Index YoY (Jun)--

F: --

P: --

U.S. Dallas Fed New Orders Index (Jul)--

F: --

P: --

U.S. Dallas Fed General Business Activity Index (Jul)--

F: --

P: --

U.K. BRC Shop Price Index YoY (Jul)--

F: --

P: --

Japan Unemployment Rate (Jun)--

F: --

P: --

Japan Job Seeker Ratio (Jun)--

F: --

P: --

Australia Building Approval Total YoY (Jun)

Australia Building Approval Total YoY (Jun)--

F: --

P: --

Australia Building Permits MoM (SA) (Jun)--

F: --

P: --

Australia Private Construction Permits MoM (SA) (Jun)--

F: --

P: --

Australia Building Permits YoY (SA) (Jun)--

F: --

P: --

France GDP Prelim YoY (SA) (Q2)

France GDP Prelim YoY (SA) (Q2)--

F: --

P: --

Turkey Economic Confidence Index (Jul)

Turkey Economic Confidence Index (Jul)--

F: --

P: --

Germany GDP Prelim YoY (Not SA) (Q2)--

F: --

P: --

Germany GDP Prelim YoY (SA) (Q2)--

F: --

P: --

Germany GDP Prelim QoQ (SA) (Q2)--

F: --

P: --

Italy GDP Prelim YoY (SA) (Q2)--

F: --

P: --

Euro Zone GDP Prelim YoY (SA) (Q2)--

F: --

P: --

Euro Zone GDP Prelim QoQ (SA) (Q2)--

F: --

P: --

Euro Zone Services Sentiment Index (Jul)--

F: --

P: --

Euro Zone Industrial Climate Index (Jul)--

F: --

P: --

Euro Zone Economic Confidence Index (Jul)--

F: --

P: --

No matching data

US

US VN US VN

VN US VNLatest Views

Latest Views

Trending Topics

To quickly learn market dynamics and follow market focuses in 15 min.

In the world of mankind, there will not be a statement without any position, nor a remark without any purpose.

Inflation, exchange rates, and the economy shape the policy decisions of central banks; the attitudes and words of central bank officials also influence the actions of market traders.

Money makes the world go round and currency is a permanent commodity. The forex market is full of surprises and expectations.

Top Columnists

Enjoy exciting activities, right here at FastBull.

The latest breaking news and the global financial events.

I have 5 years of experience in financial analysis, especially in aspects of macro developments and medium and long-term trend judgment. My focus is maily on the developments of the Middle East, emerging markets, coal, wheat and other agricultural products.

BeingTrader chief Trading Coach & Speaker, 8+ years of experience in the forex market trading mainly XAUUSD, EUR/USD, GBP/USD, USD/JPY, and Crude Oil. A confident trader and analyst who aims to explore various opportunities and guide investors in the market. As an analyst I am looking to enhance the trader’s experience by supporting them with sufficient data and signals.

Latest Update

Risk Warning on Trading HK Stocks

Despite Hong Kong's robust legal and regulatory framework, its stock market still faces unique risks and challenges, such as currency fluctuations due to the Hong Kong dollar's peg to the US dollar and the impact of mainland China's policy changes and economic conditions on Hong Kong stocks.

HK Stock Trading Fees and Taxation

Trading costs in the Hong Kong stock market include transaction fees, stamp duty, settlement charges, and currency conversion fees for foreign investors. Additionally, taxes may apply based on local regulations.

HK Non-Essential Consumer Goods Industry

The Hong Kong stock market encompasses non-essential consumption sectors like automotive, education, tourism, catering, and apparel. Of the 643 listed companies, 35% are mainland Chinese, making up 65% of the total market capitalization. Thus, it's heavily influenced by the Chinese economy.

HK Real Estate Industry

In recent years, the real estate and construction sector's share in the Hong Kong stock index has notably decreased. Nevertheless, as of 2022, it retains around 10% market share, covering real estate development, construction engineering, investment, and property management.

Hongkong, China

Ho Chi Minh, Vietnam

Dubai, UAE

Lagos, Nigeria

Cairo, Egypt

View All

No data

English

English Español

Español العربية

العربية Bahasa Indonesia

Bahasa Indonesia Bahasa Melayu

Bahasa Melayu Tiếng Việt

Tiếng Việt ภาษาไทย

ภาษาไทย Русский язык

Русский язык 简中

简中 繁中

繁中Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Hongkong, China

Ho Chi Minh, Vietnam

Dubai, UAE

Lagos, Nigeria

Cairo, Egypt

India is expected to be the largest driver of global oil demand growth between 2023 and 2030, narrowly taking the lead from top importer China, the International Energy Agency (IEA) said on Wednesday.

India is expected to be the largest driver of global oil demand growth between 2023 and 2030, narrowly taking the lead from top importer China, the International Energy Agency (IEA) said on Wednesday.

The world's third-largest oil importer and consumer is on track to post an oil demand increase of almost 1.2 million barrels per day (bpd) between 2023 and 2030, accounting for more than one-third of the projected 3.2 million bpd of global increases in the period, the IEA said in a report released at the India Energy Week in Goa.

The agency forecast India's demand would reach 6.6 million bpd in 2030, up from 5.5 million bpd in 2023.

"India will become the largest source of global oil demand growth between now and 2030, while growth in developed economies and China initially slows and then subsequently goes into reverse in our outlook," it added.

The single largest basis of India's oil consumption will be diesel fuel, accounting for almost half of the rise in the nation's demand and more than one-sixth of total global oil demand growth through to 2030, the IEA said.

Jet fuel is poised to grow 5.9% annually on average but this will be from a low base compared with other countries, it added.

"In the case of India, compared with China or other parts of the world, the Indian economy still continues to need more transport fuels so we expect India will continue to grow in transportation fuels. So that's something different from countries like China," Keisuke Sadamori, the IEA's director of energy markets and security, said on the sidelines of the conference.

Still, the electrification of India's vehicle fleet will lead to a more muted 0.7% annual growth average through 2030 for gasoline, the IEA said. New electric vehicles and energy efficiency improvements in India will avoid 480,000 bpd of extra oil demand from now to 2030, it added.

To meet this demand, India is expected to add 1 million bpd of new refining capacity over the seven-year period and this will increase its crude imports further to 5.8 million bpd by 2030, the IEA said.

"India is moving to the right path in terms of adding large additional refining capacities," Prasad Panicker, chairman of Indian refiner Nayara Energy said at the conference.

He added that Indian gasoline demand will not peak for "at least the next 20-25 years".

G Krishnakumar, the chairman of state run refiner Bharat Petroleum Corp, said that petrochemical demand for the company will also be a factor in India's oil consumption increase, as demand growth for petrochemicals is "directly proportional to the gross domestic product of the country."

An executive from India's top refiner Indian Oil Corp said on Tuesday at the conference that growth in all oil product sales are expected to rise in the fiscal year to March 2025.

The IEA report estimated India's oil inventories were at 243 million barrels, with 26 million barrels held at strategic petroleum reserves sites while the rest are industry stocks.

"This equates to 66 days of net imports, based on IEA methodology. Indian oil import requirements will rise rapidly toward 2030 and beyond," the IEA said in the report.

Pakistan is counting votes in a general election marred by violence by armed groups and a suspension of mobile phone services. More than 128 million people were registered to elect representatives of the National Assembly and the nation’s four provincial legislatures.

The results will appear below as soon as they are available.

Keep reading

list of 4 items

list 1 of 4

Pakistan election 2024: By the numbers

list 2 of 4

Pakistan election 2024: How the voting works

list 3 of 4

‘Guerilla campaign’: How Imran Khan is fighting Pakistan election from jail

list 4 of 4

Pakistan’s election: Can the next government bring economic stability?

end of list

Each voter can cast two votes — one for the National Assembly and the other for the provincial assembly.

The National Assembly comprises 336 seats – 266 to be decided through direct voting, while 60 seats are reserved for women and 10 for minorities which are allotted on the basis of 5 percent proportional representation in the federal parliament.

A party or a coalition will need 134 seats to form the government.

Based on the results of the national census conducted in 2023, the constituencies went through a delimitation process. The boundaries of many constituencies were altered and the number of seats was reduced from 272 to 266.

A crackdown on the biggest opposition party, Pakistan Tehreek-e-Insaf (PTI), and its leader, former Prime Minister Imran Khan, fuelled concerns that the polls would not be free and fair. Here are the country’s major parties:

Pakistan Muslim League-Nawaz (PMLN)

Nawaz Sharif, a three-time prime minister, returned to Pakistan after four years – in late 2023 – to assume the role of the head of the party. Several corruption cases that had led to his dismissal as prime minister in 2017 have since been dropped. Shehbaz Sharif, his younger brother, has also briefly been prime minister in an alliance with key opposition parties to remove Khan as prime minister in April 2022. If the PMLN forms a government, it is unclear which brother might become PM, but Nawaz will likely hold the strings either way.

Pakistan Peoples Party (PPP)

Bilawal Bhutto Zardari is the scion of the Bhutto dynasty. He will be leading his party after having served as foreign minister for a short period after Khan’s removal as PM in 2022. One of the youngest mainstream politicians, his campaign pays attention to climate change, gender equity in the economy, and striving for civility among parties. His grandfather Zulfikar Ali Bhutto and mother Benazir Bhutto ruled the country as prime ministers, and his father Asif Ali Zardari was Pakistan’s president from 2008 to 2013.

Pakistan Tehreek-e-Insaf (PTI)

Cricketer-turned-politician Imran Khan is the leader of the opposition PTI party. He is currently in jail in cases related to corruption and leaking state secrets. He led protests against the country’s powerful military after his removal from office in 2022. His conviction in a corruption case resulted in him being disqualified as a candidate. His party has ruled Khyber Pakhtunkhwa for the past decade, and the country’s most influential province, Punjab, for most of the past five years.

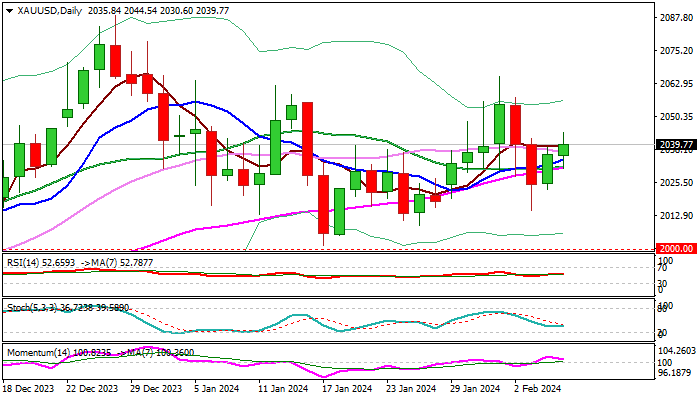

Short-term action remains in a sideways mode after the metal’s price spiked to new record high ($2141) in early December, holding within $1973/$2088 range, but mainly above psychological $2000 level, which adds to positive bias.

Gold is consolidating after Oct-Dec 2023 18% advance, a part of larger uptrend from $1616 (Nov 2022 higher low) with strong prospects for further gains, as growing global geopolitical tensions, economic uncertainty and signals that the Fed considers interest rates cuts later this year, continue to keep demand for safe-haven bullion steady.

The price is likely to continue to fluctuate within current range, awaiting fresh signals from fundamental side as technical studies on all larger timeframes remain bullishly aligned and contribute to positive outlook.

Gold can rise towards Fibonacci projections at $2206/26, on firm break of $2141 peak, with extension towards $2300 zone expected on stronger acceleration.

Res: 2056; 2065; 2088; 2100

Sup: 2014; 2009; 2000; 1985

WASHINGTON – The US Department of Justice’s decision on Feb 8 not to file criminal charges against US President Joe Biden for mishandling classified documents should have been an unequivocal legal exoneration.

Instead, it was a political nightmare.

The investigation into Mr Biden’s handling of the documents after being vice-president called him a “well-meaning, elderly man with a poor memory” and described interviews in which he could not recall when he served as vice-president, what year his son Beau died or whom he agreed with during policy debates.

The memory of the then-80-year-old president was so hazy during five hours of interviews with FBI investigators over two days, according to the report by Robert Hur, the special counsel, that it would be difficult to convince jurors that Mr Biden knew his handling of the documents was wrong. Mr Hur predicted in the report that if the president were charged, his lawyers “would emphasise these limitations in his recall”.

In part because of Mr Biden’s memory, Mr Hur declined to recommend charging the president for what the report described as willful retention of national security secrets, including some documents shared by the president that implicated “sensitive intelligence sources and methods”.

“It would be difficult to convince a jury that they should convict him – by then a former president well into his 80s – of a serious felony that requires a mental state of willfulness,” Mr Hur wrote.

In his own statement, Mr Biden appeared to suggest a reason for why he was distracted.

“I was so determined to give the special counsel what they needed that I went forward with five hours of in-person interviews over two days on Oct 8 and 9 of last year, even though Israel had just been attacked on Oct 7 and I was in the middle of handling an international crisis,” he wrote. “I just believed that’s what I owed the American people.”

The president’s lawyers, Mr Bob Bauer and Mr Richard Sauber, took exception in a Feb 5 letter with Mr Hur’s description of the president’s memory.

“It is hardly fair to concede that the president would be asked about events years in the past, press him to give his ‘best’ recollections and then fault him for his limited memory,” the lawyers wrote. “The president’s inability to recall dates or details of events that happened years ago is neither surprising nor unusual.”

Concerns about Mr Biden’s age have been a recurring theme of his presidency over the past three years. Fuelled in part by video of the president appearing weak or stumbling in public, many voters have expressed concern about his mental and physical fitness as he seeks to remain in the White House until he is 86 years old.

During fundraisers on Feb 7, he twice recalled a 2021 conversation with Helmut Kohl, the one-time German chancellor, who died in 2017. His spokeswoman later said he mis-spoke, as many public officials do.

Mr Biden has tried to laugh off the issue, insisting that with age comes wisdom. And his aides have repeatedly insisted that despite how the president sometimes comes across in public, he remains sharp and tireless when he is in private, in discussions with aides or in meetings with foreign leaders.

In the report by Special Counsel Robert Hur, a damaged box where classified documents were found in President Joe Biden’s garage in Wilmington, Delaware, during a search by the FBI, on Dec 21, 2022, is shown. PHOTO: NYTIMES

But the report released on Feb 7 challenges those descriptions, not by relying on short snippets of Mr Biden posted to social media but rather on hours-long interactions with the president in controlled settings. And the descriptions of his memory were more vivid than what is normally found in legal documents like the one released on Feb 8.

Mr Biden’s political rivals, including former President Donald Trump, who has had his own string of unforced gaffes, are certain to seize on the detailed conclusions in the report as evidence that he is too frail to lead the country for another term.

In the report, Mr Hur wrote that in a 2017 recorded conversation between Mr Biden and the ghostwriter for his book, Mr Biden struggled to “remember events” and was “straining at times to read and relay his own notebook entries”. Mr Hur said that the interviews in 2023 with investigators were even worse.

“He did not remember when he was vice-president, forgetting on the first day of the interview when his term ended (‘if it was 2013 – when did I stop being vice president?’), and forgetting on the second day of the interview when his term began (‘in 2009, am I still vice-president?’),” the report said. “He did not remember, even within several years, when his son Beau died.”

Mr Hur was nominated by Trump to be the US attorney in Maryland, but was later chosen by Attorney General Merrick Garland to lead the investigation into Mr Biden’s handling of classified documents.

Mr Biden’s lawyers have been arguing for more than a year that the discovery of classified documents at his offices and Delaware home was no more than accidental oversight, and certainly not criminal behaviour like the 37 felony charges brought against Trump for his handling of classified material after leaving office.

On Feb 8, the special counsel came to the same conclusion after reviewing a total of seven million documents – a fact celebrated inside the White House and at the president’s re-election campaign headquarters, where aides are preparing to wage a fierce battle to prevent Trump’s return to the White House.

But the report refuted the longstanding argument by the president’s lawyers that Mr Biden never put the nation’s national security at risk. Investigators found documents at Mr Biden’s home in a “box in the garage, near a collapsed dog crate, a dog bed, a Zappos box, an empty bucket, a broken lamp wrapped with duct tape, potting soil, and synthetic firewood”.

While concluding that “the evidence does not establish Mr Biden’s guilt beyond a reasonable doubt,” Mr Hur nonetheless wrote that Mr Biden took classified documents and notebooks about Afghanistan with him in 2017 after leaving the vice-presidency, and shared some of those documents with his ghostwriter.

The tough language by Mr Hur could set the stage for Trump and his allies to launch a fresh round of political attacks on Mr Biden for doing the very same kinds of things Trump is accused of doing. And it will probably complicate the months-long effort by Mr Biden and his advisers to draw sharp distinctions between the actions of the two presidents.

But the most searing political damage is likely to be about Mr Biden’s age, which many veteran Democrats already believe is the president’s biggest weakness. Some have privately said they worried that something would come along to remind voters about the age issue, including the possibility of a fall or a mental stumble.

Republicans began using the report to attack Mr Biden almost immediately, sometimes going much further than the prosecutor’s actual conclusions.

In some ways, the Feb 8 report was the worst of all worlds: an official description of Biden behind the scenes, suggesting that with age come stumbles. NYTIMES

Summary

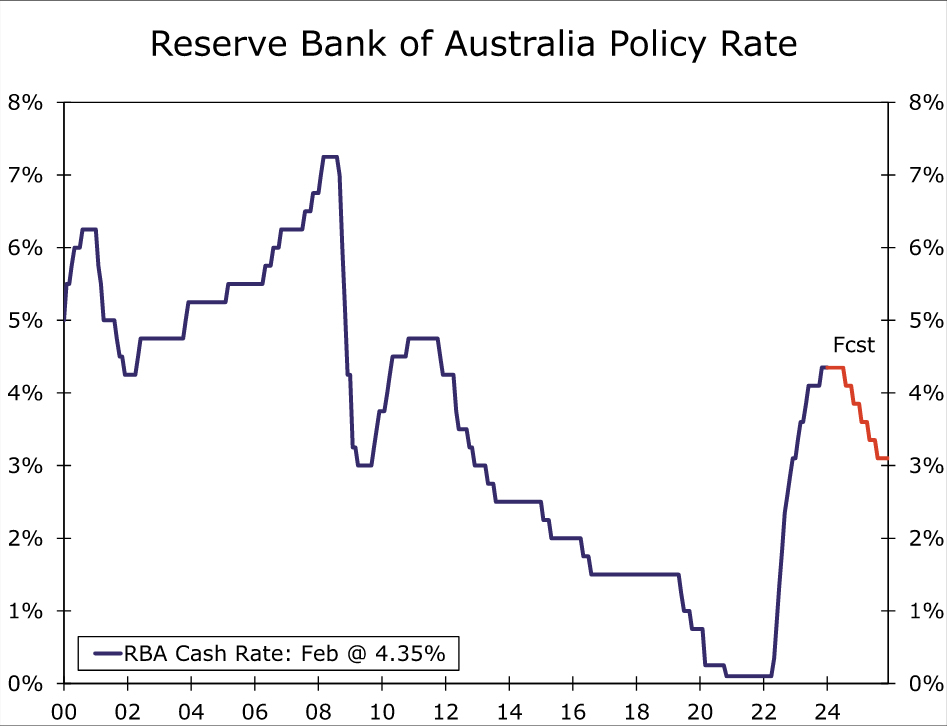

The Reserve Bank of Australia (RBA) held its policy interest rate at 4.35% at this week’s meeting, as widely expected. While acknowledging slower growth and improving inflation trends, the RBA is nonetheless clearly wary of reducing interest rates prematurely. This is reflected in several elements of its announcement:

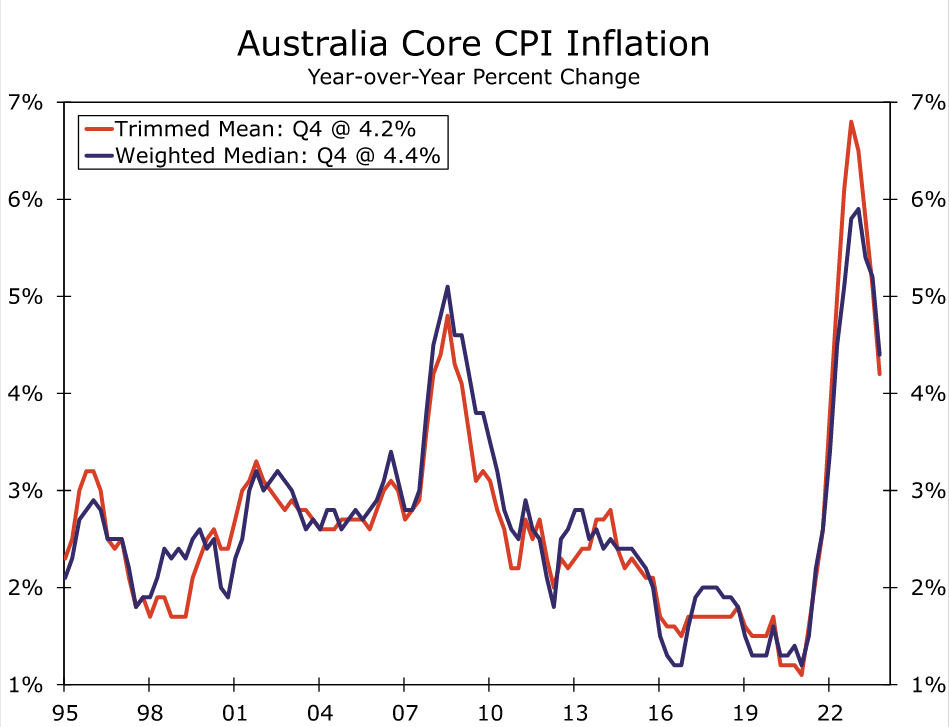

Importantly, therefore, the RBA kept the possibility of a rate increase on the table, even as it lowered both its GDP growth and CPI inflation forecasts. With respect to economic activity, the RBA now forecasts annual average GDP growth of 1.5% for 2024, down from the 1.8% it forecast in November. It also projects a slightly faster rise in the unemployment rate to 4.3% by the end of this year, compared to 4.2% previously. Meanwhile, despite a downside surprise for Australia’s CPI in Q4-2023, inflation is expected to remain above the 2%-3% inflation target range for an extended period. Both headline inflation and trimmed mean inflation are not forecast to return to that target range until the end of 2025, and are not forecast to be at the midpoint of that range until mid-2026.

Keep in mind these forecasts are all predicated on the technical assumption of a policy rate path that is broadly consistent with market implied pricing, which sees the policy rate at 4.3% in mid-2024 and 3.9% by end-2024. Even with that technical assumption, however, the RBA projects inflation remaining above the target range for an extended period. In our view, given that RBA continues to highlight that “returning inflation to target within a reasonable timeframe remains the Board’s highest priority”, at the very least that suggests rate cuts are unlikely to come before the second half of this year. That is, we view the RBA’s announcement and forecasts as consistent with interest rate cuts starting in the second half of this year or later.

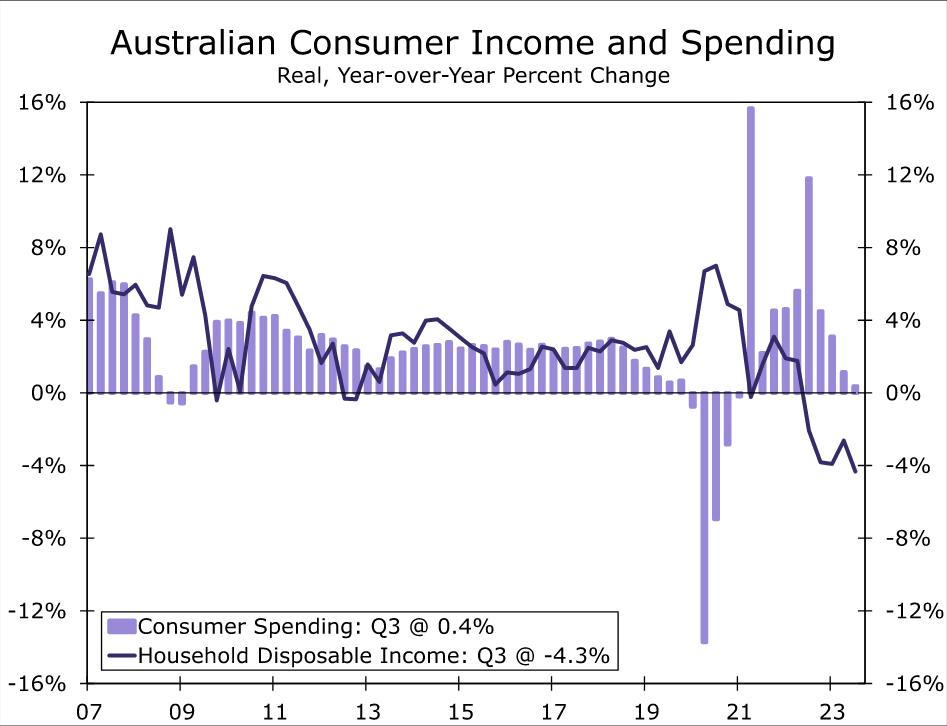

Against this backdrop, we doubt that sluggish economic growth will elicit early easing from Australia’s central bank. The RBA has repeatedly highlighted an uncertain outlook for the consumer, uncertainty that is reflected in recent data. Q4 real retail sales rose a modest 0.3% quarter-over-quarter and, while that was better than expected, it was offset by a downward revision to Q3 sales. In fact, the increase in quarterly sales was the first since Q3-2022, and thus, in our view, represents more stabilization than strength in retail activity. In terms of consumer fundamentals, real household disposable incomes fell 4.3% year-over-year in Q3-2023 and the household saving rate dropped to just 1.1% of disposable income, arguing against a quick rebound in consumer spending. Perhaps on a more encouraging note however, tax cuts scheduled for 1 July have been adjusted to provide greater support to lower income earners, which should at least offer some support for consumer spending, and help to limit the extent of any slowdown in the overall economy.

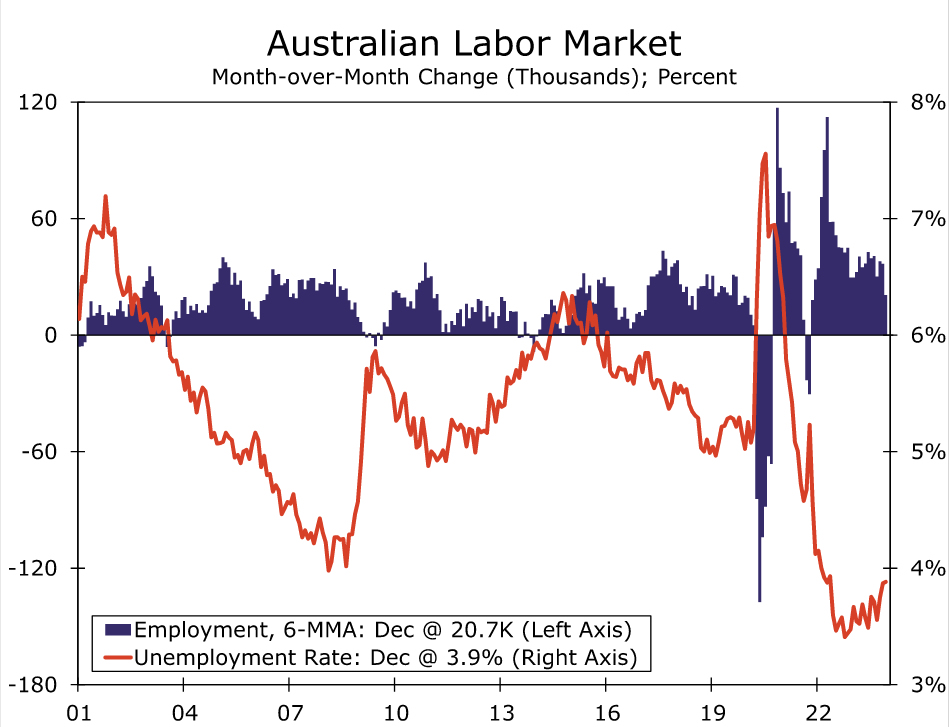

Even amid slow growth, the labor market has remained reasonably resilient so far. Employment has been particularly volatile in recent months, with a large December decline in jobs broadly offsetting a big November increase. Looking through that volatility, the average monthly employment increase slowed during the second half of last year to a still-respectable 20,700 per month. The unemployment rate has also increased to 3.9%, from as low as 3.4% in late 2022. While the labor market has loosened to some extent, we note that a further moderate increase in unemployment and slowing in wage growth (from the current 4.1% year-over-year for the Wage Price Index) would be in line with the RBA’s forecast, and could make the central bank more comfortable that inflation is returning sustainably to the target range.

Accordingly, we think an initial RBA rate cut remains some way off. At this time, we remain comfortable with our outlook for an initial 25 bps rate reduction to 4.10% at the August monetary policy announcement, by which time the labor market will likely have softened further, and wage and price pressures will likely have moderated somewhat. We also expect the pace of rate cuts to be quite gradual even after that initial easing, at just 25 bps per quarter, which means the RBA’s policy rate would not reach a low of 3.10% until the second half of 2025. While we see risks around this policy rate outlook in both directions, those risks are perhaps tilted toward a later rate cut than an earlier rate cut. Persistence in services or wage inflation could easily see an initial rate cut pushed back to Q4 of this year while, although it is not our base case, an especially sharp slowdown in consumer spending or inflation pressures could still prompt the RBA to move earlier than August.

The pace of monetary easing we forecast for the RBA, at least through the end of 2024, is broadly in line with that implied by market pricing. As mentioned, however, the risks are more heavily tilted toward a later move. Moreover, even our base case for an initial RBA rate cut in August sees Australia’s central bank moving noticeably later than the Federal Reserve, where we expect an initial rate cut to occur in May. Overall, a gradual moderation of Australian economic growth and inflation that leads to only a gradual pace of monetary easing from the Reserve Bank of Australia should be supportive of the Australian dollar versus the greenback over time.

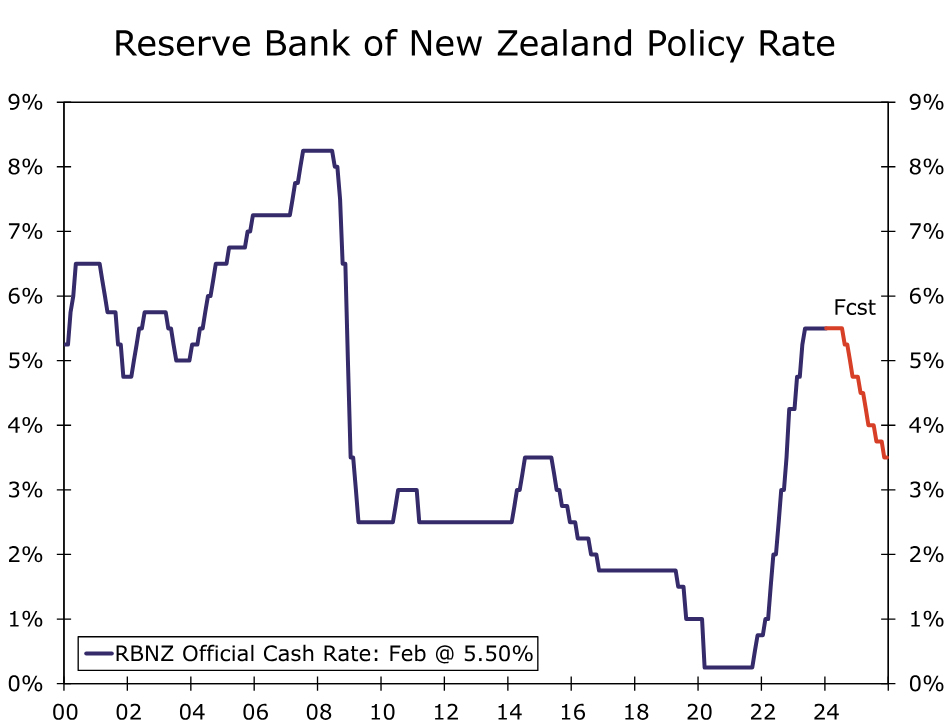

High Inflation and Recovering Economy Keeping New Zealand Central Bank Hawkish

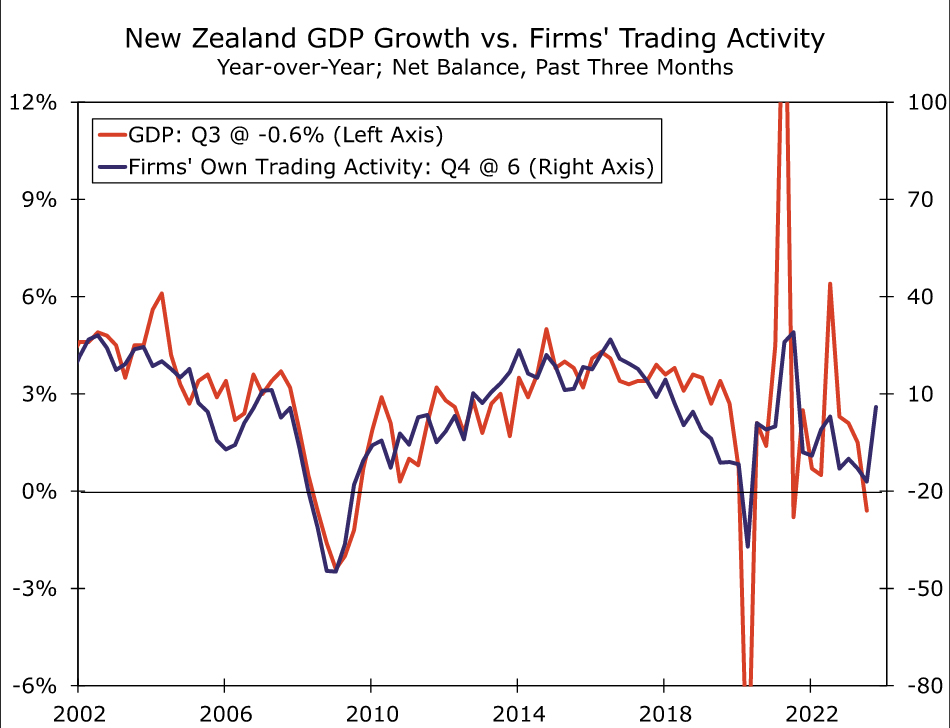

In New Zealand, the economy appears to be moving toward recovery after what was a challenging year through much of 2023. The impact of elevated inflation and the Reserve Bank of New Zealand’s (RBNZ) aggressive monetary tightening contributed to GDP reporting sequential declines in three out of four quarters through Q3-2023, according to the latest available figures. Election-related uncertainty may have also provided a temporary restraint to growth late last year. Q3-2023 saw New Zealand’s GDP fall 0.3% quarter-over-quarter and 0.6% year-over-year: economic underperformance that occurred even as immigration, and population growth, surged.

Some key economic headwinds facing New Zealand are now starting to abate; inflation has peaked, and we also believe the RBNZ has come to the end of its rate hike cycle. We think that should gradually allow for the economy to transition to a recovery phase, even if these key fundamentals have not turned to significant tailwinds just yet. That appears to be reflected in some available economic indicators for Q4 of last year. Most importantly, the Quarterly Survey of Business Opinion saw businesses become much less downbeat, as just a net 2% of businesses were pessimistic in Q4, compared to the net 52% of businesses who were pessimistic in Q3. Moreover, a net 6% of respondents reported an increase in their own trading activity in Q4, compared to net 17% who reported a decrease in Q3. This latter point is significant as, historically, it is firms’ assessment of their own trading activity that has tended to be more closely correlated with overall GDP growth.

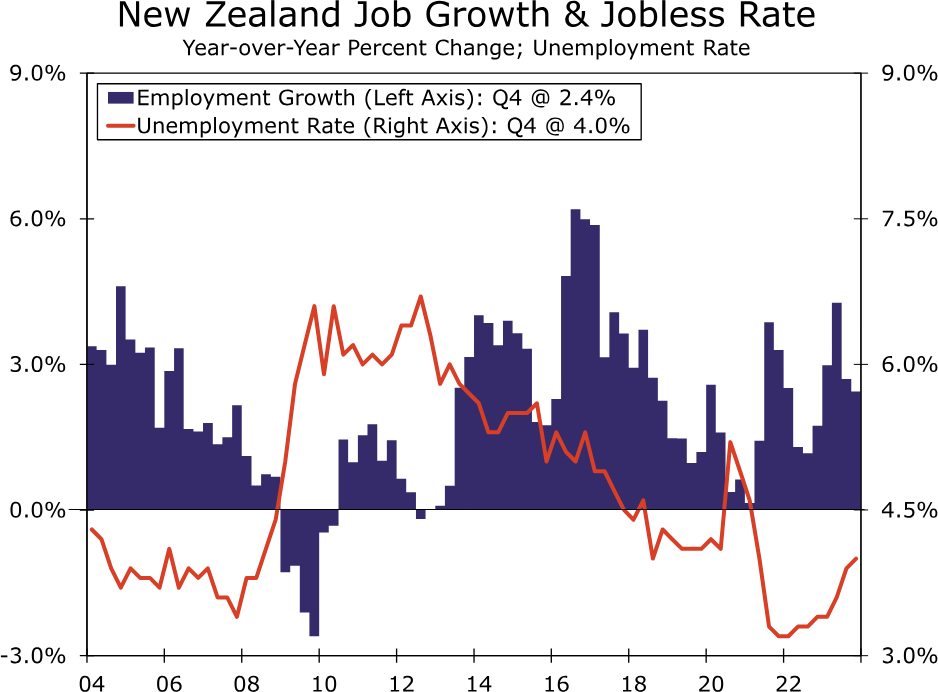

The improvement in sentiment in Q4 suggests that a gradual economic recovery may be upon us, a message that is also reflected in labor market data for the fourth quarter. Q4 employment rose 0.4% quarter-over-quarter, rebounding following a small decline in Q3, while employment was also up 2.4% year-over-year. The unemployment rate did edge higher to 4.0%, though in part, that stems from surging population growth. In fact, if anything, rising unemployment may help to place some restraint on wage pressures. The fourth quarter also saw the Labor Cost Index for the private sector rise to 1.0% quarter-over-quarter and ease to 3.9% year-over-year. Overall, we believe the New Zealand economy can enjoy a moderate recovery this year. We forecast GDP growth of 1.2% for 2024, which would be up from an estimated 0.8% growth in 2023.

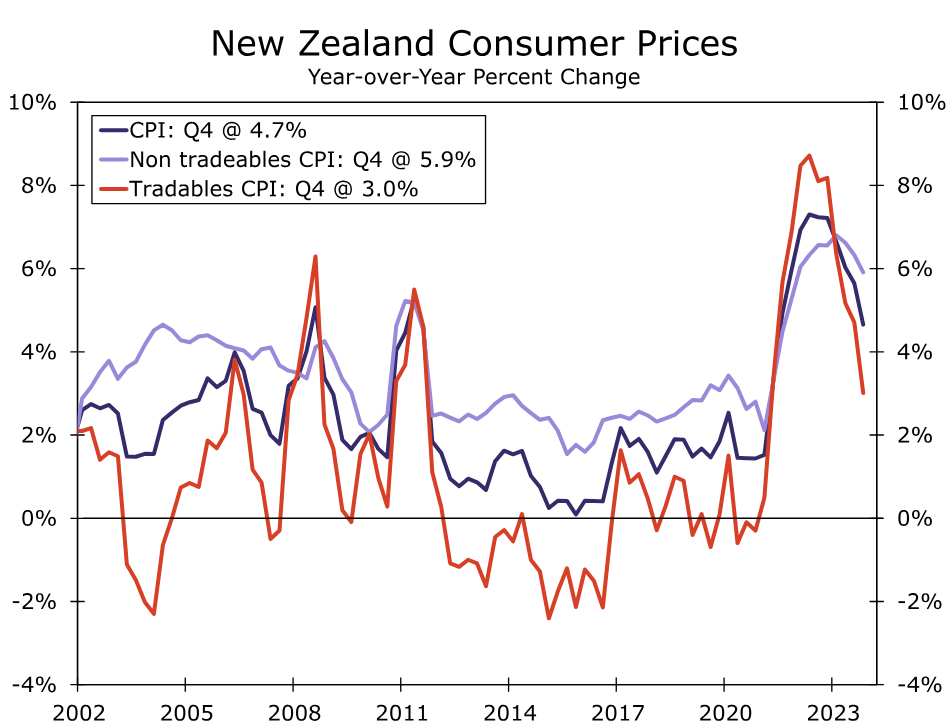

On the inflation front, consumer prices have started to recede, although domestically oriented inflation pressures remain persistent. Q4 CPI inflation slowed to 4.7% year-over-year, matching the consensus forecast. However, although tradeables inflation surprised to the downside and slowed to 3.0%, non-tradeables inflation surprised to the upside, with only a moderate slowing to 5.9%. Both headline inflation and, more particularly, domestically-oriented inflation, remain well above the central bank’s 2% inflation target. As a result, the RBNZ has maintained a relatively hawkish monetary policy stance. At its most recent announcement in November, the RBNZ said that despite some decline, inflation remains too high, and policymakers maintain a wariness of inflationary pressures. In fact, the central bank said if inflationary pressures were stronger than expected, the policy rate would likely need to increase further. In more recent comments, RBNZ Chief Economist Conway offered additional hawkish comments. Conway said non-tradeables inflation was higher than expected and a long way from 2%, and that the central bank still has a way to go to get inflation back to target. Given the backdrop of improving sentiment, domestic inflationary pressures and a hawkish central bank, we now see RBNZ policy rate cuts occurring later than previously envisaged. We expect an initial 25 bps rate cut to 5.25% at the August announcement. Beyond that, we see a relatively steady pace of easing, with our forecast for a cumulative 75 bps of rate cuts in 2024, and a further cumulative 125 bps of rate cuts in 2025, which would see the RBNZ’s policy rate reach 3.50% by the end of next year. Against a backdrop of a U.S economic slowdown and Fed easing, we believe a moderate rebound in NZ economic growth and gradual RBNZ monetary easing should see the New Zealand dollar enjoy moderate gains against the U.S. dollar over time.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.