Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

The Wall Street Journal Reports That U.S. House Democrats Have Launched An Investigation Into A $500 Million Investment By Members Of The Abu Dhabi Royal Family In World Freedom Finance, A Company Owned By The Trump Family, And Are Urging U.S. Prosecutors To Investigate The Matter Concurrently

Cook: Weak Consumer Sentiment Does Not Reveal A Signal About An Increase In Slack That Can Be Tackled With Fed Policy Rate

Cook: It Is Anticipated That Disinflation Could Resume Once Tariff Effects Recede, But There Is 'Much Uncertainty'

Cook: US Economy Solid, But Some Signs Of Worsening Outlook For Low- And Moderate- Income Households

Cook: Labor Market Has Stabilized And Is Roughly In Balance, But Highly Attentive To Potential For Quick Shift

Cook: My Focus Will Be On Bringing Inflation Down To 2% Until I See Stronger Evidence It Is Moving There

Spot Gold Rebounded Above $5,000 Per Ounce In Early Trading On Thursday, Rising 0.7% On The Day, After A Sharp Pullback In Spot Gold And Silver Overnight

According To Sources Familiar With The Matter, Boeing Will Lay Off 300 Supply Chain Jobs In Its Defense Division. The Company Is Notifying Affected Workers This Week

U.S. House Oversight Committee Chairman Comer Is Considering Subpoenaing Bill Gates In Connection With The Epstein Case

U.K. Composite PMI Final (Jan)

U.K. Composite PMI Final (Jan)A:--

F: --

P: --

U.K. Total Reserve Assets (Jan)A:--

F: --

P: --

U.K. Services PMI Final (Jan)A:--

F: --

P: --

U.K. Official Reserves Changes (Jan)A:--

F: --

P: --

Euro Zone Core CPI Prelim YoY (Jan)

Euro Zone Core CPI Prelim YoY (Jan)A:--

F: --

P: --

Euro Zone Core HICP Prelim YoY (Jan)A:--

F: --

P: --

Euro Zone HICP Prelim YoY (Jan)A:--

F: --

P: --

Euro Zone PPI MoM (Dec)A:--

F: --

Euro Zone Core HICP Prelim MoM (Jan)A:--

F: --

P: --

Italy HICP Prelim YoY (Jan)

Italy HICP Prelim YoY (Jan)A:--

F: --

P: --

Euro Zone Core CPI Prelim MoM (Jan)A:--

F: --

P: --

Euro Zone PPI YoY (Dec)A:--

F: --

U.S. MBA Mortgage Application Activity Index WoW

U.S. MBA Mortgage Application Activity Index WoWA:--

F: --

P: --

Brazil IHS Markit Composite PMI (Jan)

Brazil IHS Markit Composite PMI (Jan)A:--

F: --

P: --

Brazil IHS Markit Services PMI (Jan)A:--

F: --

P: --

U.S. ADP Employment (Jan)A:--

F: --

The U.S. Treasury Department released its quarterly refinancing statement. U.S. IHS Markit Composite PMI Final (Jan)A:--

F: --

P: --

U.S. IHS Markit Services PMI Final (Jan)A:--

F: --

P: --

U.S. ISM Non-Manufacturing Price Index (Jan)A:--

F: --

P: --

U.S. ISM Non-Manufacturing Employment Index (Jan)A:--

F: --

P: --

U.S. ISM Non-Manufacturing New Orders Index (Jan)A:--

F: --

P: --

U.S. ISM Non-Manufacturing Inventories Index (Jan)A:--

F: --

P: --

U.S. ISM Non-Manufacturing PMI (Jan)A:--

F: --

P: --

U.S. EIA Weekly Crude Oil Imports ChangesA:--

F: --

P: --

U.S. EIA Weekly Heating Oil Stock ChangesA:--

F: --

P: --

U.S. EIA Weekly Crude Demand Projected by ProductionA:--

F: --

P: --

U.S. EIA Weekly Gasoline Stocks ChangeA:--

F: --

P: --

U.S. EIA Weekly Crude Stocks ChangeA:--

F: --

P: --

U.S. EIA Weekly Cushing, Oklahoma Crude Oil Stocks ChangeA:--

F: --

P: --

Australia Trade Balance (SA) (Dec)

Australia Trade Balance (SA) (Dec)--

F: --

P: --

Australia Exports MoM (SA) (Dec)--

F: --

P: --

Japan 30-Year JGB Auction Yield

Japan 30-Year JGB Auction Yield--

F: --

P: --

Indonesia Annual GDP Growth

Indonesia Annual GDP Growth--

F: --

P: --

Indonesia GDP YoY (Q4)--

F: --

P: --

France Industrial Output MoM (SA) (Dec)

France Industrial Output MoM (SA) (Dec)--

F: --

P: --

Italy IHS Markit Construction PMI (Jan)--

F: --

P: --

Euro Zone IHS Markit Construction PMI (Jan)--

F: --

P: --

Germany Construction PMI (SA) (Jan)

Germany Construction PMI (SA) (Jan)--

F: --

P: --

Italy Retail Sales MoM (SA) (Dec)--

F: --

P: --

U.K. Markit/CIPS Construction PMI (Jan)--

F: --

P: --

France 10-Year OAT Auction Avg. Yield--

F: --

P: --

Euro Zone Retail Sales YoY (Dec)--

F: --

P: --

Euro Zone Retail Sales MoM (Dec)--

F: --

P: --

U.K. BOE MPC Vote Cut (Feb)--

F: --

P: --

U.K. BOE MPC Vote Hike (Feb)--

F: --

P: --

U.K. BOE MPC Vote Unchanged (Feb)--

F: --

P: --

U.K. Benchmark Interest Rate--

F: --

P: --

MPC Rate Statement U.S. Challenger Job Cuts (Jan)--

F: --

P: --

U.S. Challenger Job Cuts MoM (Jan)--

F: --

P: --

U.S. Challenger Job Cuts YoY (Jan)--

F: --

P: --

Bank of England Governor Bailey held a press conference on monetary policy. Euro Zone ECB Marginal Lending Rate--

F: --

P: --

Euro Zone ECB Deposit Rate--

F: --

P: --

Euro Zone ECB Main Refinancing Rate--

F: --

P: --

ECB Monetary Policy Statement U.S. Weekly Initial Jobless Claims (SA)--

F: --

P: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)--

F: --

P: --

U.S. Weekly Continued Jobless Claims (SA)--

F: --

P: --

ECB Press Conference

No matching data

View All

No data

Europe's major economies launch critical mineral stockpiling to secure vital resources and reduce China dependence.

The European Union's three largest economies—Germany, France, and Italy—are set to lead a major initiative to build strategic stockpiles of critical minerals, a move designed to reduce the bloc's reliance on China for essential raw materials.

According to sources familiar with the strategy, the plan assigns specific responsibilities to each nation to streamline the effort.

Under the new framework, the division of labor is clear:

• Germany will be responsible for overseeing the sourcing of the critical minerals.

• France will manage efforts to secure financing for the EU's purchases.

• Italy will oversee the storage and logistics for the stockpiled metals and minerals.

This coordinated structure was outlined in a December meeting with EU officials. However, details regarding which producers Germany has approached or which banks might be involved in financing the purchases have not yet been made public.

This stockpiling initiative is a core component of the European Commission's wider RESourceEU Action Plan, which was formally adopted in early December. The plan aims to secure the EU’s supply of materials like rare earth elements, cobalt, and lithium.

The Commission stated the initiative provides concrete tools and financing to achieve several key goals:

• Protect European industry from geopolitical tensions and price volatility.

• Promote critical raw material projects both within Europe and abroad.

• Forge partnerships with allied countries to diversify supply chains.

Work on the coordinated EU approach to stockpiling began late last year, with a pilot scheme anticipated to become operational early this year.

To support these efforts, the Commission is establishing a European Critical Raw Materials Centre. This body will act as a "portfolio manager" for the EU, handling joint purchasing and managing the stockpiles to ensure resilient supply chains.

Looking ahead, the EU is also planning to enhance its internal circular economy. By early 2026, the Commission intends to introduce export restrictions on scrap and waste from permanent magnets to strengthen Europe's domestic recycling capacity. Similar measures are being considered for copper scrap if deemed necessary.

Beyond stockpiling and recycling, the EU is exploring direct investment to secure resources at their source. In November, European Commissioner Maros Sefcovic noted that the bloc is considering buying direct stakes in critical minerals projects in Australia as another way to secure long-term supply.

Oil prices surged on Wednesday, driven by two major catalysts: a report that nuclear talks between the United States and Iran have been canceled and industry data revealing a surprisingly large drop in U.S. crude inventories.

By 12:39 ET, Brent oil futures for April delivery had jumped 3.5% to $69.68 a barrel. West Texas Intermediate crude futures matched the gain, rising 3.5% to trade at $64.42 a barrel.

The primary driver for the market rally was news that planned diplomatic talks between Washington and Tehran had collapsed. According to a report from Axios, the meeting scheduled for Friday was called off after the U.S. declined to change the location and format.

Iranian officials had reportedly insisted on narrowing the negotiations to focus solely on nuclear issues in a two-way format, raising doubts about the viability of the dialogue from the start.

This diplomatic breakdown coincides with rising military tensions in the Middle East. Recent incidents include:

• The U.S. military shooting down an Iranian drone that approached an American aircraft carrier in the Arabian Sea.

• A group of Iranian gunboats approaching a U.S.-flagged tanker in the Strait of Hormuz.

The possibility of escalating military action, with U.S. President Donald Trump threatening further measures and Tehran warning of retaliation, introduces significant risk to regional stability. Any conflict could potentially disrupt crucial oil supplies from the Middle East, a fear that has been supporting crude prices in recent sessions.

Adding to the upward pressure on prices, industry data showed an unexpected and substantial decline in U.S. oil stockpiles.

The American Petroleum Institute (API) reported that U.S. inventories shrank by 11.1 million barrels in the week ending January 30. This figure starkly contrasts with analyst expectations for a 0.7 million barrel build, catching the market by surprise.

The outsized inventory draw is largely attributed to extreme cold weather across the country, which has disrupted oil production and interfered with exports from the Gulf Coast.

The API data often signals a similar trend in the official government inventory figures, which are due later in the day. Ongoing disruptions in U.S. supplies have been a key factor helping to boost oil prices in recent weeks.

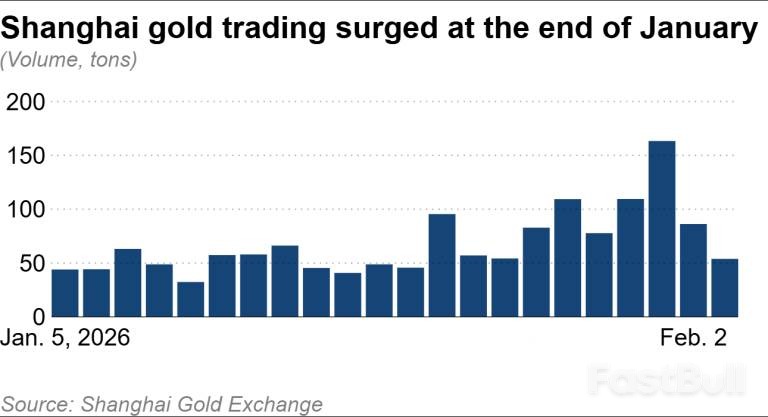

A sharp drop in gold prices, driven by institutional investors, has triggered a buying spree among Chinese retail investors looking to capitalize on the dip. This surge in demand from China is amplifying volatility in the global gold market.

The recent gold slump began after the nomination of Kevin Warsh as the next potential U.S. Federal Reserve chair. Markets reacted to Warsh's reputation as an inflation hawk, speculating he would be less inclined to pursue the deep interest rate cuts favored by U.S. President Donald Trump. This outlook caused the dollar to rebound, putting immediate pressure on gold prices in Asian markets.

Adding to the momentum, commodity trading models at Chinese quantitative hedge funds had reportedly already started reducing their gold positions ahead of the Lunar New Year holiday. The sudden price reversal caught many off guard, leading to significant losses for leveraged investors, from large funds to individual households.

Some analysts had previously warned that the gold market was overheated due to a heavy influx of capital from Chinese retail investors and speculators. As prices fell, these speculative players pulled back, stoking fears of a liquidity crisis in the market.

While institutional players sold, many retail investors in China saw the downturn as a long-awaited buying opportunity. Trading volume on the Shanghai Gold Exchange soared as gold prices fell, driven by a fear of missing out on lower prices.

The enthusiasm was visible on the ground. A sales associate at a Shanghai shopping center noted on Tuesday that the store "suddenly became crowded with customers wanting to buy while prices are still low." With the Lunar New Year approaching, many were also purchasing gold for holiday gifts.

In Wuhan, local media reported that customers in bathrobes lined up with folding chairs, waiting overnight for a gold sale to begin. The frenzy has also boosted related stocks, with Laopu, a high-end gold brand, seeing its share price soar to roughly 20 times its IPO price. "Products from Laopu Gold can be resold for more than the gold itself," a resident of Hubei province commented.

For many Chinese retail investors, gold represents one of the few reliable investment options available. Strict restrictions on converting the yuan into foreign currencies and moving capital overseas limit their ability to diversify and protect their assets. Although the Shanghai Composite Index is trending upward, it remains over 30% below its 2007 peak, leaving a lingering sense of caution around equities.

This sentiment is echoed across social media. A well-known blogger’s post stating, "It's a dip, buy the dip," has been widely shared, with the blogger claiming to have purchased gold 12 times during the current downturn. However, not all opinions are unified; some users have questioned the fundamental valuation of gold.

Official data underscores the trend. According to China's National Bureau of Statistics, retail sales of gold, silver, and jewelry hit a record 373.6 billion yuan ($53.8 billion) in 2025, a 13% increase from the previous year. This brought the cumulative total since 2006 to 4.6 trillion yuan.

The intense retail demand has put Chinese authorities on alert. On Monday, the Postal Savings Bank of China issued a notice urging investors to control their investment amounts and avoid chasing high prices.

Other major banks are following suit. China Construction Bank has raised its minimum purchase amount for gold, while the Industrial and Commercial Bank of China plans to implement limits on holiday trading starting Saturday.

This shift marks a notable change in tone. Previously, when the People's Bank of China resumed building its gold reserves, retail investors interpreted it as an official signal to buy. Now, authorities are actively issuing warnings that could dampen demand from one of the metal's most significant markets.

The UK's dominant services sector cut jobs last month as companies increasingly opted for automation over hiring, a closely watched business survey has revealed. Despite a rebound in business activity, employment numbers fell more sharply in January than in December, extending a downward trend that began in October 2024.

According to the monthly Purchasing Managers' Index (PMI), this marks the "longest period of job shedding" for the services sector in 16 years. Firms are not only cutting jobs but also choosing not to replace staff who leave voluntarily.

The UK's services sector is the largest part of its economy, contributing nearly 80% of the country's output and covering industries from hotels and catering to finance and law.

The survey, compiled by S&P Global, found anecdotal evidence that companies are turning to automation to fill staffing gaps and increase productivity. This trend is amplified by squeezed profit margins and fragile market conditions that are dampening hiring decisions.

Tim Moore, economics indices director at S&P Global Market Intelligence, highlighted the pressure on businesses. "There were again gloomy signals for the UK labour market outlook as staff hiring decreased at a steeper pace in January as firms looked to offset rising payroll costs," he said.

The move toward automation has been particularly evident in specific industries. On Tuesday, Anthropic, the company behind the Claude chatbot, announced its tool could automate legal work. The news triggered a sharp sell-off in the shares of publishing and data companies, which began in London and continued across global markets into Wednesday, even as the FTSE 100 reached a record high.

These cost pressures are compounded by several other factors:

• Rises in the national living wage.

• Increases in employers' national insurance contributions since last April.

• Widespread inflation in energy and food prices.

• A recent shake-up of business rates, which has pushed up bills for some companies and drawn criticism of the government.

In a contrasting trend, overall business activity in the services sector had a strong start to 2026. After a weak final quarter, output rebounded to a five-month high.

The PMI survey's activity index rose to a balance of 54 in January, up from 51.4 in December. This marked the fastest pace of expansion since August, with any reading above 50 indicating growth.

When combined with the manufacturing PMI data for January, the overall reading showed that UK business activity hit a 17-month high.

The survey suggests the improvement was partly driven by a lift in sentiment following the budget in late November, which ended months of speculation about potential tax increases. This clarity allowed delayed projects and investment to move forward.

Expectations for a business upturn were also at their strongest since October 2024. That same month, Chancellor Rachel Reeves had imposed unexpectedly large tax rises on companies in her first budget, despite corporate concerns about geopolitical risks and weak consumer demand.

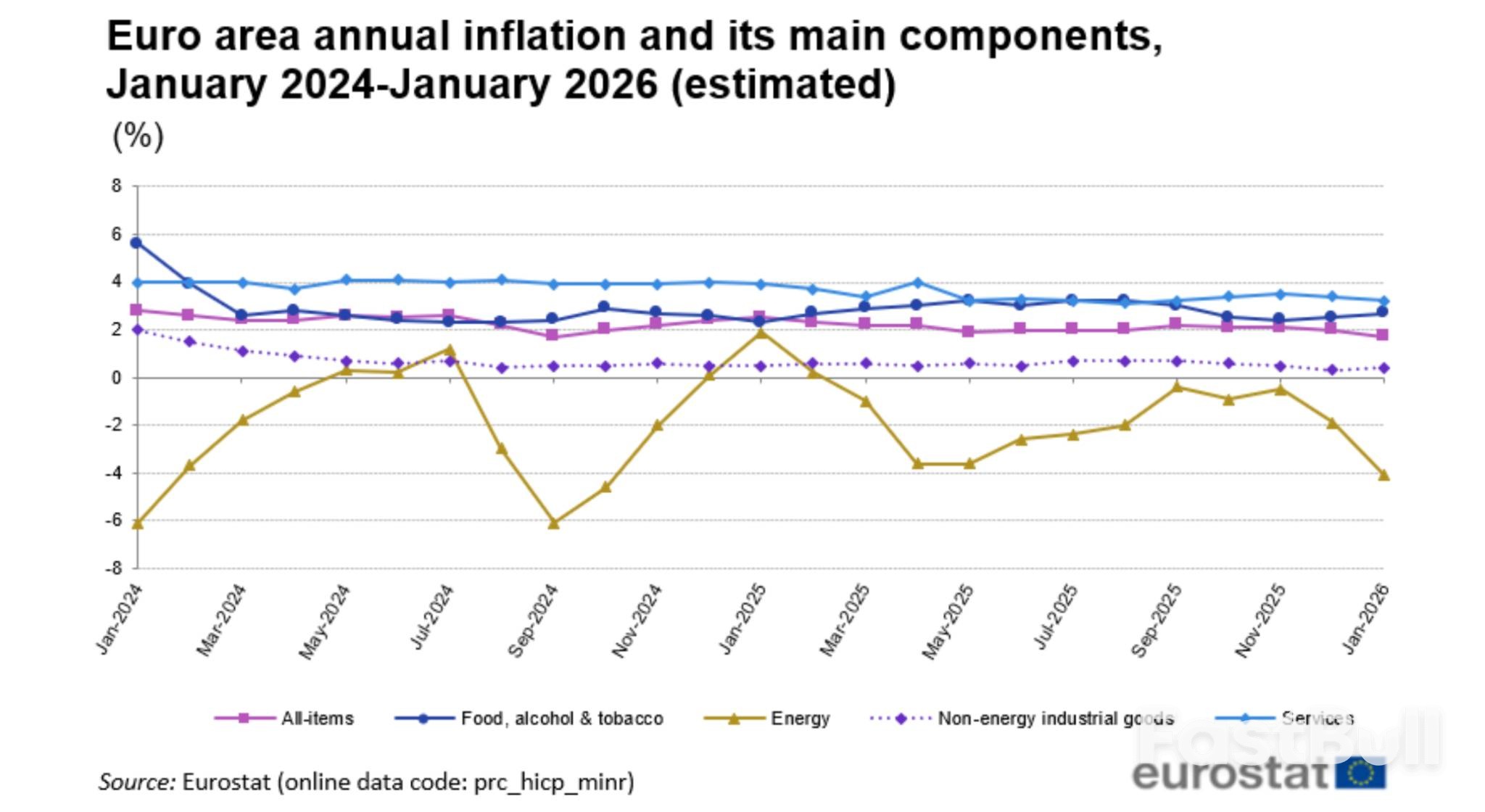

The European Central Bank is set to meet on February 5, 2026, and while no one expects a change in interest rates, the event is shaping up to be a pivotal moment for the euro. With EUR/USD trading below the key 1.20 level, all eyes will be on President Christine Lagarde's press conference for clues about the ECB's next major policy decision.

As cooling inflation and a strengthening currency cloud the outlook, policymakers and markets are divided. The central question is whether the ECB’s next move later in the year will be a rate hike or a rate cut. The answer will likely depend on the central bank's interpretation of an increasingly complex economic picture.

At its final meeting of 2025, the ECB presented a confident view of the eurozone economy. The central bank upgraded its growth forecasts, projecting 1.4% growth for 2025, followed by 1.2% in 2026, and a return to 1.4% in 2027 and 2028.

On the inflation front, the ECB's December projections showed prices normalizing around its 2% target. The forecast anticipated inflation averaging 2.1% in 2025, falling to 1.9% in 2026, and eventually settling at 2% by 2028. This outlook suggested that interest rates could remain unchanged throughout 2026, with the ECB describing its policy as being in a "good place."

However, recent data has complicated this narrative. January figures from Eurostat showed headline inflation in the euro area slowed to 1.7%, its lowest level since September 2024. More significantly, core inflation, which strips out volatile items, unexpectedly fell to 2.2% from 2.3%. This trend has fueled debate over whether disinflationary pressures are stronger than anticipated.

Two factors are at the center of this concern:

1. A Stronger Euro: The euro's recent appreciation against the dollar makes imports cheaper, dampening inflation.

2. Chinese Imports: An influx of lower-priced goods from China is putting downward pressure on prices across European markets.

ECB Governing Council member Gediminas Simkus recently noted the bank's success in bringing inflation back to target despite global challenges. Still, he warned that ongoing political instability remains a significant risk that could easily disrupt the ECB's current policy balance.

For the upcoming meeting, the market consensus is clear: the ECB will hold its key interest rates steady for the fifth consecutive time. The deposit facility rate is expected to remain at 2.00%, the main refinancing operations rate at 2.25%, and the marginal lending facility rate at 2.40%.

But beneath this surface-level agreement, a fierce debate is brewing over the direction of the next policy shift.

The Case for a Future Rate Hike

Despite inflation running below target, some ECB officials have not ruled out the possibility of raising rates later in 2026. This hawkish stance is driven by several considerations:

• Resilient Growth: The ECB's own upgraded growth forecasts suggest the eurozone economy could be more robust than expected. Sustained growth could generate fresh price pressures as economic capacity tightens.

• Sticky Inflation Risks: Some policymakers worry that the current 2% deposit rate may not be restrictive enough if inflation proves stubborn, especially with rising wage growth or a continued surge in energy prices. Oil and European natural gas prices have both climbed since the start of the year.

• Official Commentary: Recent remarks from key officials, including board member Isabel Schnabel, chief economist Philip Lane, and President Lagarde herself, have been interpreted by markets as keeping the option of a late-2026 hike alive.

The Argument for a Future Rate Cut

On the other side, a growing number of economists believe the ECB's next move is more likely to be a rate cut, potentially restarting the easing cycle paused in June 2025. The arguments for this dovish view include:

• Disinflationary Trend: With headline inflation at 1.7% and core inflation falling, both metrics are trending away from the ECB's 2% goal. If this continues, holding rates steady could become overly restrictive.

• Euro Appreciation: A stronger euro effectively tightens financial conditions by making imports cheaper. The ECB might need to offset this with lower interest rates if the currency continues to climb.

• Structural Pressures: The flood of competitively priced Chinese goods into Europe represents a persistent disinflationary force that could keep a lid on prices.

• Economic Fragility: Pockets of weakness remain in the eurozone, particularly in Germany's manufacturing sector, which is grappling with weak global demand and high energy costs.

The reality is that policymakers are genuinely split, with some officials stating that a hike and a cut are equally plausible outcomes depending on incoming data. This uncertainty reflects the unique position the ECB is in—having achieved its inflation target but now facing significant risks in both directions.

Diego Iscaro, head of European economics at S&P Global Market Intelligence, summarized the middle ground: "With underlying inflation still a little too high for comfort and expectations that the eurozone economy will regain momentum later in the year, we believe the most likely outcome is that the ECB will keep rates unchanged for the foreseeable future."

ECB chief economist Philip Lane articulated this balanced strategy in mid-January. He noted that the central bank will not debate a rate change in the near term if the economy stays on its projected course. However, he cautioned that new shocks could upset the outlook.

This statement perfectly captures the ECB's current posture: maintain the status quo for now, but stand ready to act decisively if economic conditions change.

The United States is hosting a high-stakes conference in Washington, D.C., gathering ministers from dozens of countries to address the future of critical mineral supply chains. The summit aims to build a global alliance to counter China's dominance over resources essential for defense, artificial intelligence, and the modern technology sector.

A central point of debate is a proposal to set a minimum price for critical minerals, an idea favored by many participating nations. However, reports suggest the U.S. is hesitant to support a price floor, creating a key tension point at the talks.

The meeting follows President Donald Trump's announcement of Project Vault, a strategic minerals stockpile for the U.S. This initiative will be capitalized with $2 billion from private sources and backed by a $10 billion loan from the U.S. Export-Import Bank.

The Critical Minerals Ministerial, hosted by Secretary of State Marco Rubio at the State Department, is a new U.S.-led effort to build a coalition that can diversify and secure the global supply of these vital resources. The main session is scheduled for Wednesday.

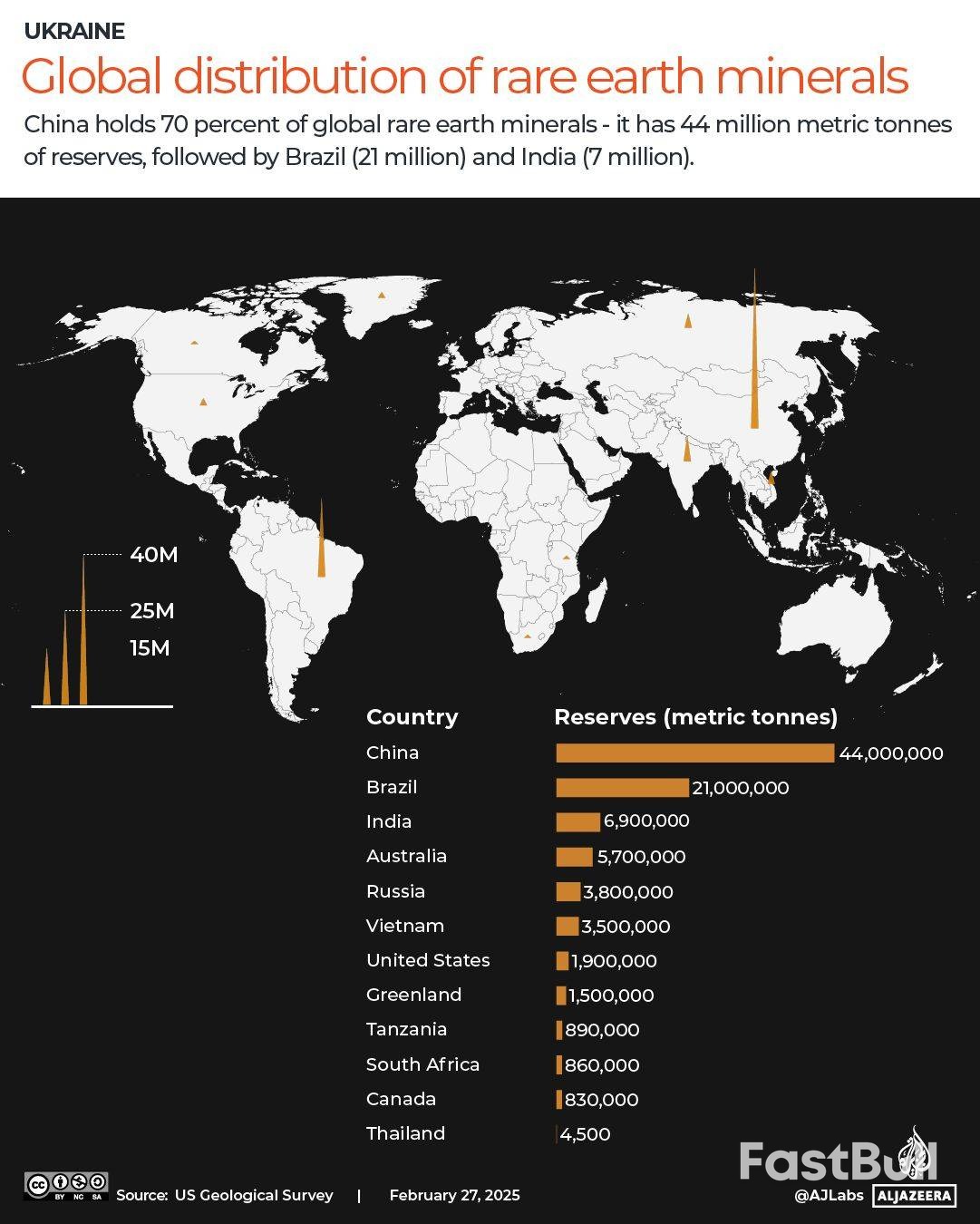

Currently, China dominates the landscape, controlling most of the world's rare earth minerals. It holds an estimated 60% of these minerals and, more importantly, processes 90% of the global supply, giving it immense leverage over everything from smartphones to fighter jets.

A Global Coalition Gathers

Delegations from over 50 countries are attending, including major economic powers like the G7 nations (Canada, France, Germany, Italy, Japan, the UK, and the US), the European Union, Australia, and New Zealand.

On the sidelines of the main event, Secretary Rubio held key bilateral meetings. He met with South Korean Foreign Minister Cho Hyun to discuss Seoul's commitments to investing in U.S. industries and securing mineral supply chains. He also met with Indian External Affairs Minister Subrahmanyam Jaishankar to explore cooperation on critical minerals.

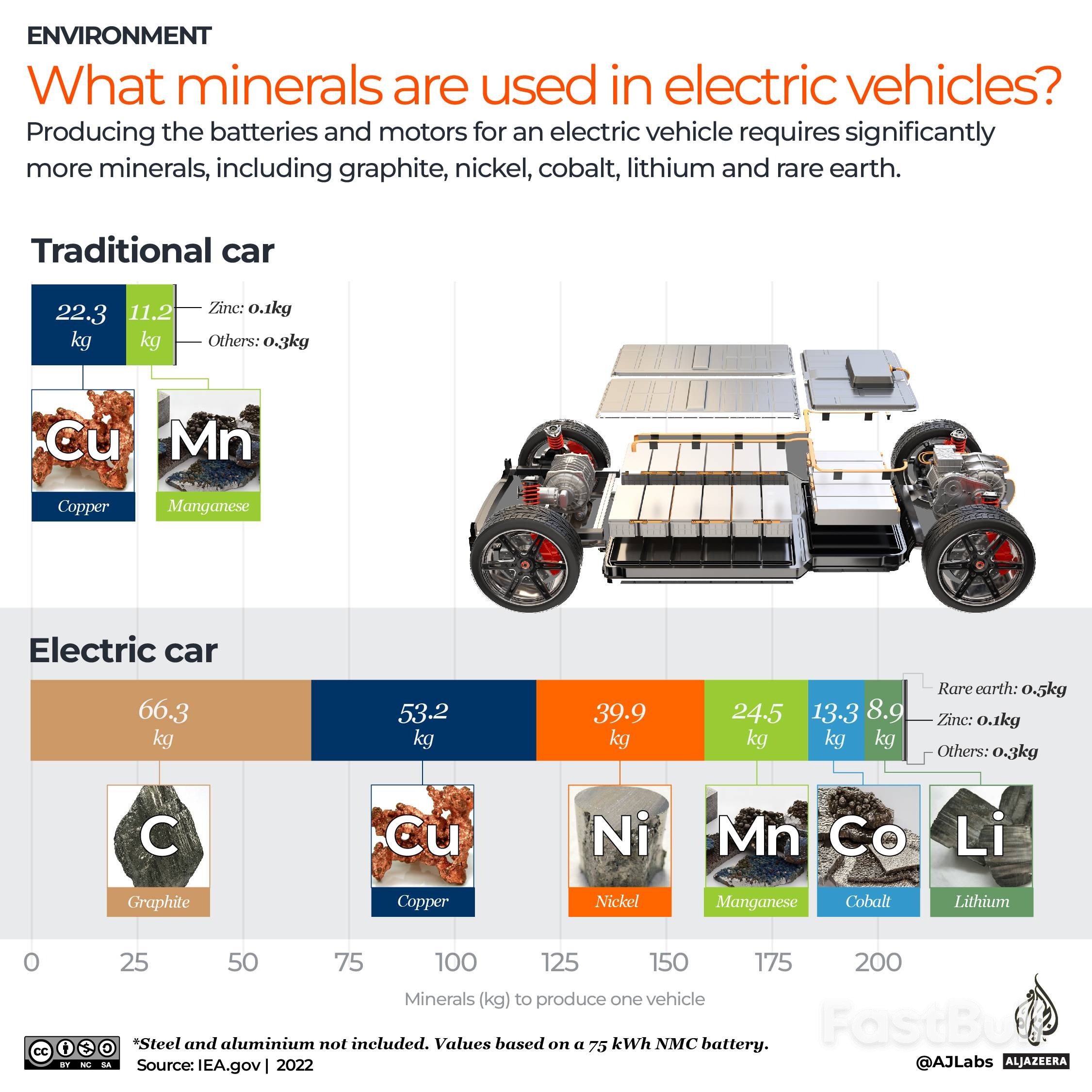

Critical minerals are non-fuel resources that form the backbone of modern technology. They are indispensable for manufacturing:

• Batteries and electric vehicles

• Semiconductors and advanced electronics

• Military hardware and defense systems

• Wiring and renewable energy generators

The U.S. government defines them as minerals "essential to the economic or national security" with supply chains that are "vulnerable to disruption." This vulnerability is stark: the U.S. is entirely dependent on imports for 12 critical minerals and imports at least half of its supply for another 29. Key examples include nickel, cobalt, lithium, aluminum, and zinc.

The Strategic Importance of Rare Earths

Within this group, 17 rare earth elements—which include the 15 lanthanides plus scandium and yttrium—are particularly crucial. China possesses deposits of 12 of these elements. Their unique magnetic properties make them necessary for producing the permanent magnets used in industrial automation, EV motors, wind turbines, and medical devices.

With Europe's supply of permanent magnets coming almost entirely from China, Western nations are increasingly concerned about their access to these materials. The high processing costs and the toxic environmental waste generated during mining add further complexity to developing alternative sources.

According to the U.S. Geological Survey (USGS), global rare earth reserves stood at approximately 110 million tonnes in 2024. A 2024 report from the Center for Strategic and International Studies described China's position as a "near monopoly," reinforced by thousands of patents for its advanced processing technologies.

Last year, Beijing began restricting exports of the 12 rare earth metals it controls, imposing curbs on seven in April and the remaining five in October. A temporary trade truce was reached between President Trump and Chinese President Xi Jinping in late October, where China agreed to pause the final five restrictions for one year in exchange for Trump dropping a threat of 100% tariffs on Chinese goods.

The ministerial's opening remarks will be delivered by Vice President JD Vance, Secretary Rubio, and other senior U.S. officials. A key topic for discussion is the implementation of a minerals price floor. Proponents argue that a minimum price would de-risk investment, encourage supply diversity, and prevent dominant players from using low prices to squeeze out smaller competitors.

However, Reuters reported that the Trump administration is backing away from guaranteeing a price floor. The news caused a drop in Australian mining stocks, as Australia has been a vocal supporter of the policy. With its own large rare earth reserves, Australia is positioning itself as a key alternative to China and is investing heavily in its processing capacity.

Analysts suggest the U.S. will use the conference to align partners with its own strategic goals. "The US is likely to push partner countries to sign minerals deals by which US companies get preferential or at least access to mineral deposits," Raphael Deberdt, a postdoctoral fellow at the Copenhagen Business School, told Al Jazeera.

Deberdt noted that while securing access is one goal, the U.S. also aims to encourage investment to expand production of rare earths, cobalt, nickel, and graphite. He added that the U.S. will likely promote a "reshuffling of critical minerals supply chains to orient processing towards its own territory and the territories of allied nations." However, he cautioned that this remains a long-term goal, as U.S. processing capabilities are still minimal compared to China's.

Besides Australia, which has the world's fourth-largest rare earth reserves, other regions are being explored. A critical minerals agreement signed by Prime Minister Anthony Albanese and President Trump in October gives the U.S. access to Australian minerals in exchange for investment. Still, Australia's reserves are only one-seventh the size of China's, prompting the U.S. to court other potential suppliers.

Greenland, which is rich in rare earth metals, is another potential source, though mining there is limited due to opposition from Indigenous Inuit communities.

In response to supply chain vulnerabilities, countries are increasingly stockpiling critical minerals. The U.S. Project Vault is part of a growing global trend:

• Japan: In March 2020, Japan reinforced its stockpiling system for rare earth minerals as part of its international resource strategy.

• South Korea: Maintains a long-running stockpile managed by a state-run corporation.

• European Union: In December, the European Commission adopted the RESourceEU Action Plan, which includes plans for a European Critical Raw Materials Centre to diversify supplies through stockpiling.

• Australia: In January, the government announced new details for its $1.2 billion Critical Minerals Strategic Reserve.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up