Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The new Complete Monthly CPI printed softer than we thought presenting downside risk to our December quarter estimates.

The new Complete Monthly CPI printed softer than we thought presenting downside risk to our December quarter estimates.

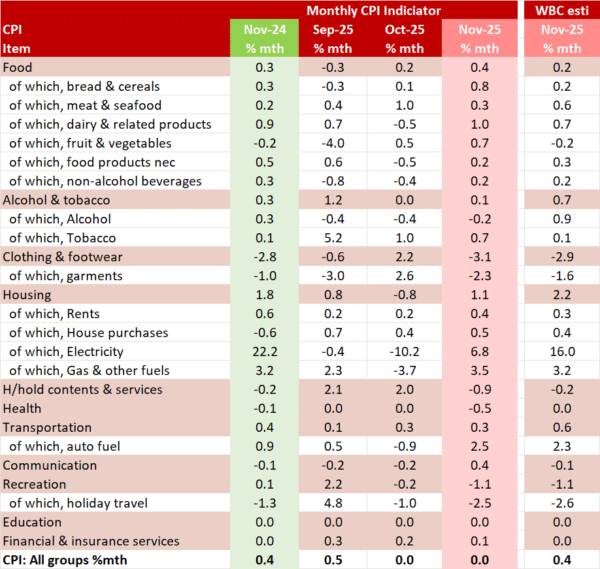

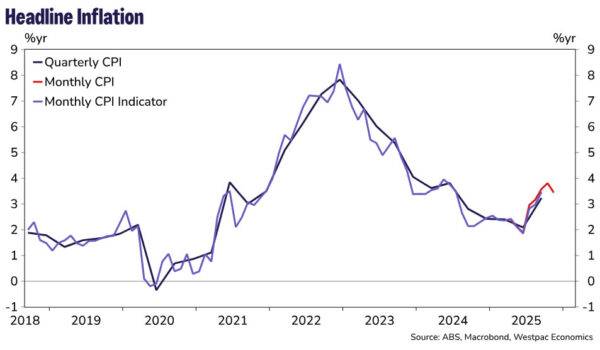

The new Complete Monthly CPI gained 3.4% in the year to November, softer than Westpac's estimate of 3.8%yr and the market estimate of 3.6%yr. At face value, this suggests downside risk to our December quarter estimates of 0.8%qtr for the Trimmed Mean (TM) and 0.6% for the CPI. However, we still need to complete a full review of the monthly data to confirm this.

November's headline figure was flat in the month, softer than Westpac's published near-cast of 0.4% on the back of a smaller than expected rise in electricity (6.8% vs 16.0% estimated), a larger than expected fall in household contents & services (–0.9% vs –0.2% estimated), clothing & footwear (–3.1% vs. –2.9% estimate) and health (–0.5% vs. 0.0% expected), a smaller than expected rise in transport (0.3% vs. 0.6% forecast) to be partially offset by stronger gains in food (0.4% vs 0.2% estimated), rents (0.4% vs 0.3% estimated), dwellings (0.5% vs 0.4% estimated) and communication (0.4% vs. –0.1% estimated).

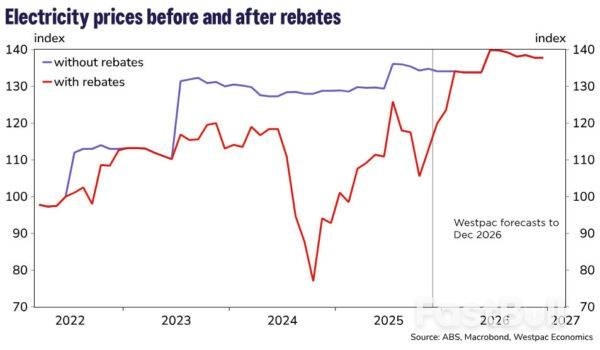

As has been the norm for some time, the energy rebates continue to have a significant impact on estimates of consumer price inflation. Electricity costs rose 19.7% in the year to November, held down by households using the Queensland State Government electricity rebate . This is a moderation from the 37.1%yr pace in October 2025 reflecting, as the ABS noted, that more households received catch-up payments of the Commonwealth Energy Bill Relief Fund (EBRF) rebate in 2024 compared to 2025.

The ABS estimates that excluding the impact of the Commonwealth and State Government electricity rebates over the past year, electricity prices rose 4.6% in the year to November compared to a 5.0% increase in the year to October. This reflects annual price reviews from energy retailers in July 2025.

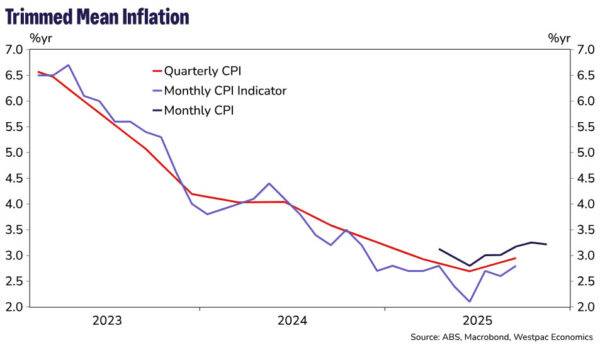

The TM measure was reported to have increased 3.2% in the year to November, a slight moderation from the 3.3%yr pace in October. Due to its short history, the annual pace of monthly TM inflation can only be calculated back to April 2025. Before then the ABS noted that annual movements are calculated by comparing each quarter to the same quarter in the previous year.

The TM lifted 0.3% in the month of November, the same monthly increase it has seen for the previous four months and down from the 0.5%mth increase in July but stronger than the 0.2%mth prints from March to June.

While we note that the current annual pace of the Monthly TM, at 3.2%yr, matches our current December quarter TM estimate of 3.2%yr, we do know that the RBA will, at least for the near term, remain focused on the quarterly TM, rather than the Monthly TM. This is because the ABS does not have enough history to complete a full seasonal adjustment process for all the components of the Monthly CPI. The ABS has also noted it will take at least 18 months to gather that data so it is likely to be a year and a half before we will be able to make a more detailed assessment of core inflation directly via the monthly TM. As such, we anticipate the RBA will use the December print to guide their decision. Our expectation is that the Monetary Policy will remain cautious and pause at its next meeting in February and remain on hold for the remainder of the year.

As we have noted, see our November CPI preview, while some series did have a longer monthly history coming from the previously published monthly CPI indicator and the ABS can potentially use historical seasonal analysis we caution that some of the new data sets have a different history to the old data and as such, we expect it is going to take some time to understand the seasonal behaviour of the new data.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up