- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

A US-India trade deal targeting global oil flows faces market realities, challenging its geopolitical aims.

A sweeping trade deal announced by U.S. President Donald Trump and Indian Prime Minister Narendra Modi aims to redirect global crude oil flows, but the plan is poised to collide with the fundamental laws of market economics.

Following tense negotiations, the agreement includes a commitment from India to purchase over $500 billion worth of U.S. energy, technology, and agricultural products. In exchange, the U.S. will lower its tariff on Indian goods from 25% to 18%.

A key component of the deal involves India, the world's third-largest oil importer, ceasing its purchases of Russian crude. Instead, it will buy "much more" oil from the United States and potentially Venezuela. While the pact serves clear U.S. strategic interests, its real-world execution faces significant economic headwinds.

This agreement advances two major White House objectives.

First, the administration seeks to revitalize Venezuela's struggling oil industry. This follows Washington's move to take effective control of the country's oil sector after the seizure of President Nicolas Maduro last month.

Second, the deal is designed to tighten the economic squeeze on Moscow. By pushing Russian crude out of Asia—one of its last major markets following Western sanctions over the war in Ukraine—the Trump administration hopes to further limit Russia's export revenues.

The pact underscores a willingness to use U.S. geopolitical influence to shape global markets. However, political directives often struggle to override powerful market incentives.

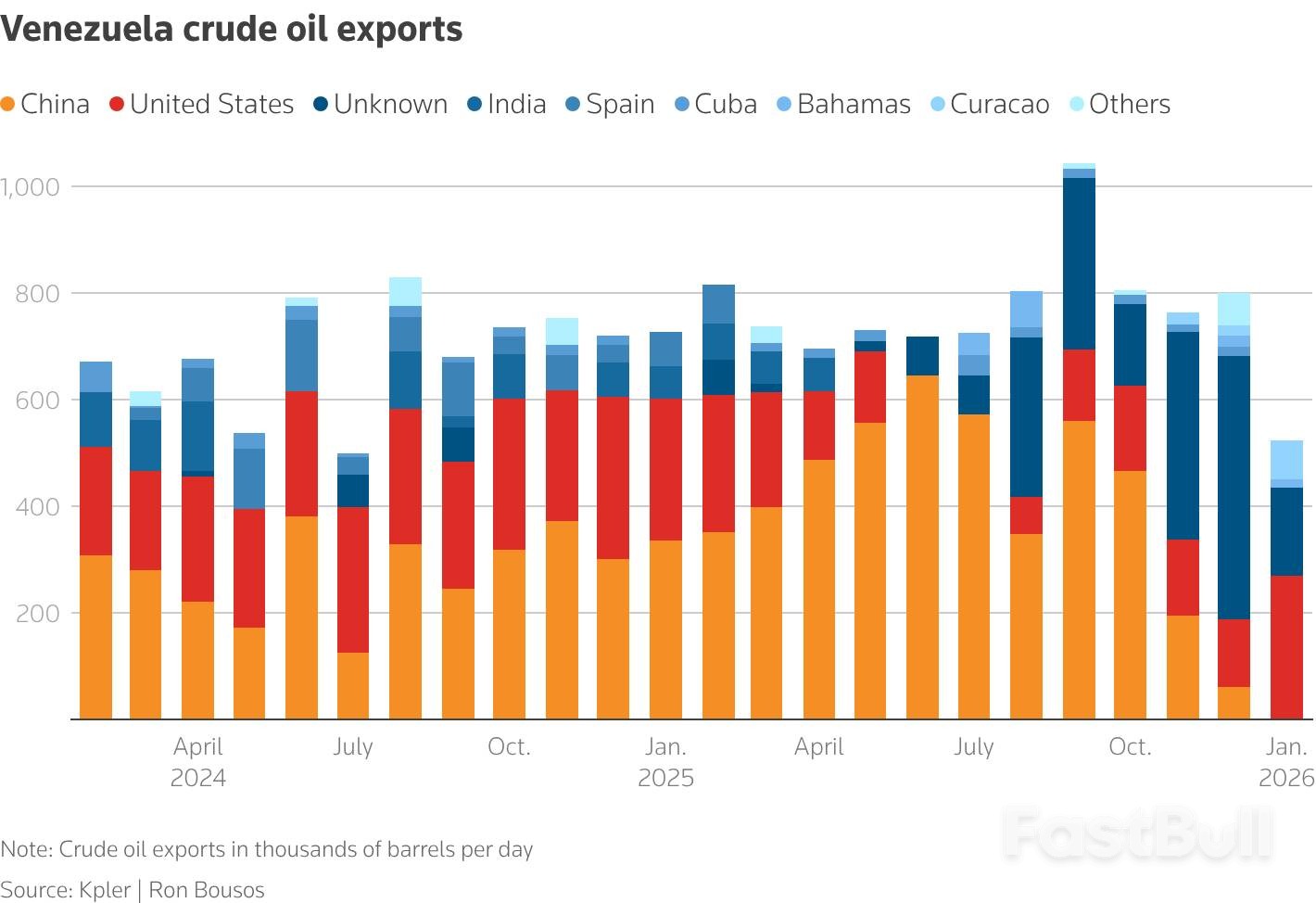

Efforts are underway to revive Venezuela's energy sector, including moves to sell up to 50 million barrels of crude, reform hydrocarbon laws to attract investment, and ease some sanctions. Asia, particularly China and India, might seem like a natural destination for this oil. China bought over half of Venezuela's crude exports last year, and India was a major buyer before Trump imposed a 25% tariff in March on countries purchasing Venezuelan oil.

Despite this, several factors limit Venezuela's ability to become a dominant supplier to India.

Production and Export Constraints

Venezuelan oil production remains limited at around 900,000 barrels per day (bpd) and is expected to take months, if not years, to recover fully. Although exports jumped to approximately 800,000 bpd in January from 498,000 bpd in December, sustained growth is needed to clear stored inventory and reverse previous production cuts.

The Economics of Sanctioned Crude

The more significant issue is simple economics. Venezuelan oil was previously attractive to Asian buyers primarily because sanctions forced it to be sold at steep discounts.

Recently, when cargoes of heavy Venezuelan crude were offered to Asian buyers at a $5 per barrel discount to the Brent benchmark, they were rejected. Traders noted the markdown was insufficient to make the heavy, sulfurous crude competitive with other available grades. Unless Venezuelan output rises so much that U.S. refiners cannot absorb it—forcing producers to offer larger discounts—Asia is likely to remain a marginal market.

Pivoting India toward U.S. oil presents its own set of challenges. Last year, India's price-sensitive buyers purchased an average of only 320,000 bpd of U.S. oil, valued at around $7.5 billion. A significant increase appears unfeasible due to higher freight costs and the fact that the U.S. government has limited ability to control private market dynamics.

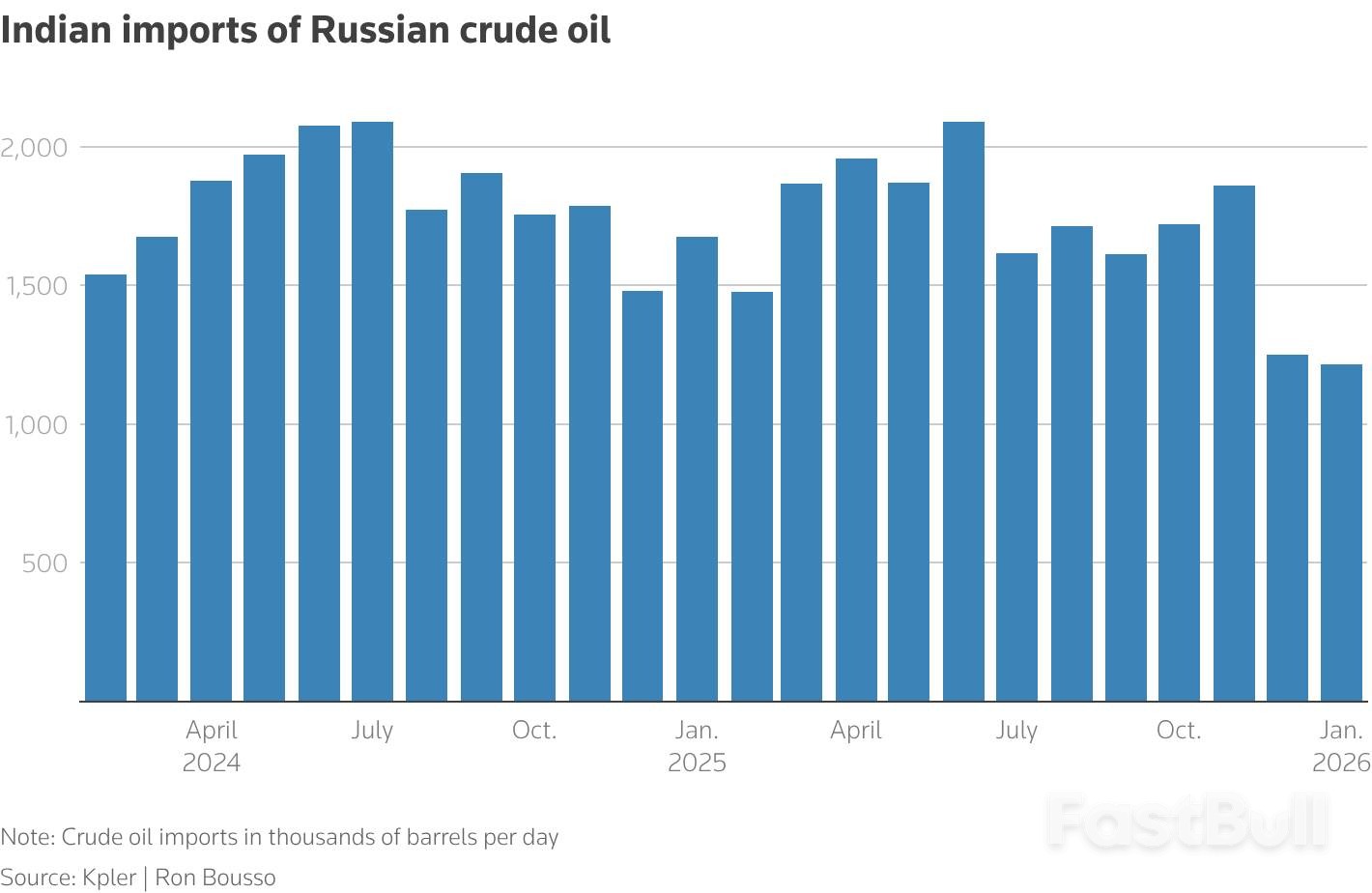

India, once the top buyer of discounted Russian crude after 2022, did reduce its purchases after the Trump administration doubled duties on Indian imports to 50% in August. This was followed by U.S. sanctions on Russia's top oil companies, Rosneft and Lukoil, in October and new EU restrictions on fuels made from Russian crude.

As part of the new trade deal, the White House confirmed it will drop the additional 25% tariff.

Even with past pressure, India imported 1.2 million bpd of Russian crude in January, accounting for over a fifth of its total imports. While this is down from the 2025 average of 1.7 million bpd, it is far from zero. The primary reason is the compelling price.

Russian oil is currently being offered at a discount of more than $20 to Brent—the steepest markdown since April 2023. While Indian refiners heavily focused on exports to Europe, like Reliance Industries' Jamnagar complex, are unlikely to resume large-scale Russian purchases due to EU rules, refiners serving India's domestic market will find such discounts difficult to resist.

Ultimately, economics will likely prevail over politics. While the U.S. wields significant influence, even President Trump cannot single-handedly steer crude flows in a highly liquid and transparent global oil market.

New Delhi may also push back against U.S. pressure to prioritize lower domestic fuel prices, a critical issue for any government. In the end, price signals—not political directives—will determine the final destination of Russian and Venezuelan oil barrels.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up