Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The Trump administration's $200B mortgage bond plan shows negligible impact on housing affordability, with experts citing a supply crisis, not financing, as the core problem while geopolitical risks loom.

The Trump administration's $200 billion plan to purchase mortgage-backed bonds was designed to make housing more affordable. However, early evidence suggests the initiative is having a negligible effect, with economists arguing it misdiagnoses the core problem facing the U.S. housing market.

Experts widely agree that the key to affordability is not cheaper financing but a significant increase in housing supply. Meanwhile, geopolitical tensions, driven in part by the administration itself, threaten to push borrowing costs higher, potentially canceling out any marginal benefits from the program.

Joseph Brusuelas, chief economist at RSM US LLP, called the bond purchases "mostly an exercise in burning cash." He added, "The U.S. does not have a demand or financing problem within the housing complex; it has a supply problem, and $200 billion in [mortgage bond] purchases is not going to do anything to bring relief to Americans on the housing front."

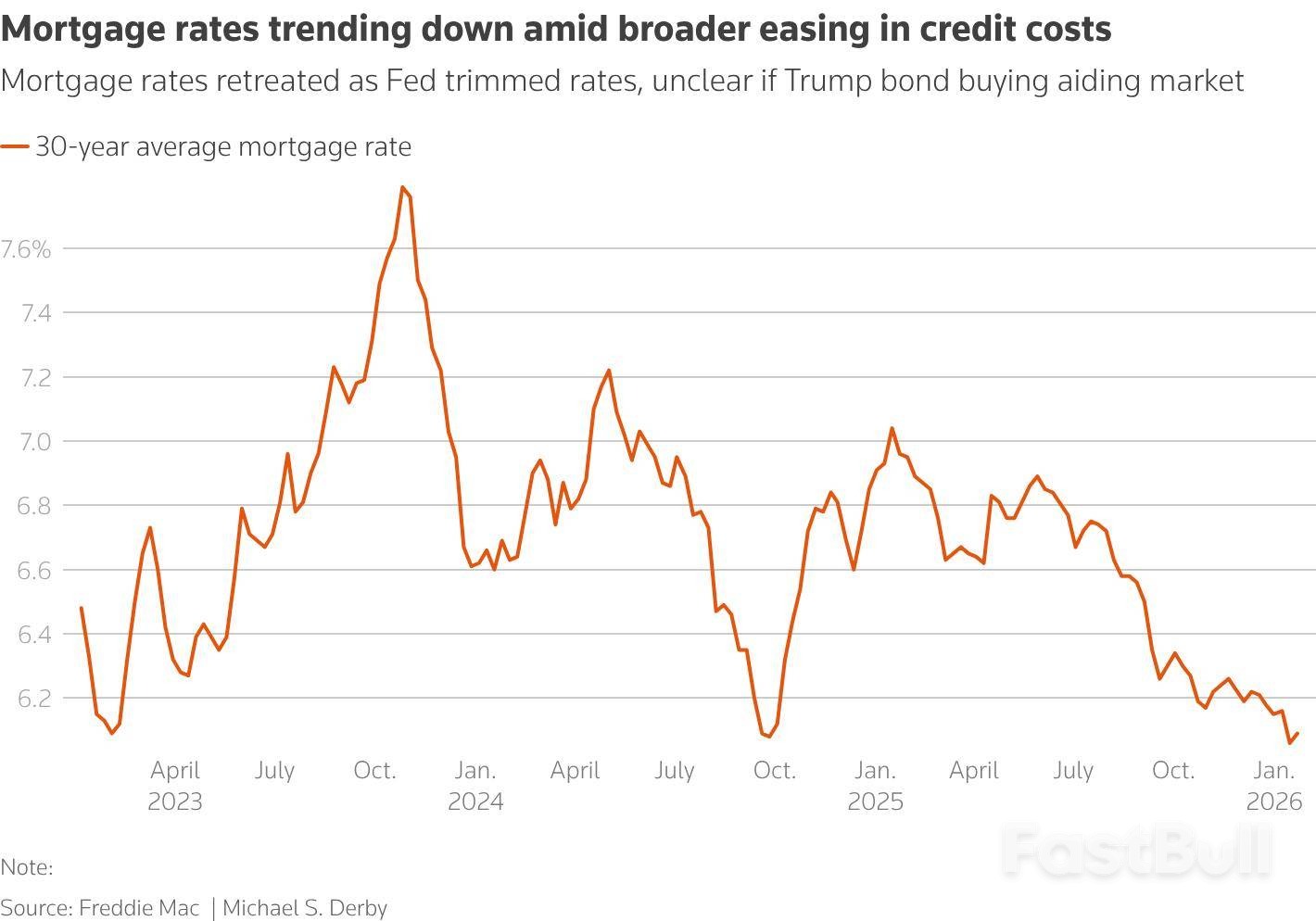

Long-term mortgage rates were already declining before the new policy, largely due to the Federal Reserve's cuts to its short-term interest rate. According to data from Freddie Mac, the average rate on a 30-year fixed-rate mortgage fell from a peak of nearly 8% in the fall of 2023 to 6.15% by the end of 2025.

After the administration directed Fannie Mae and Freddie Mac to begin buying bonds, the rate briefly touched 6.06%, its lowest point since 2022. However, it quickly edged back up to 6.09%.

Separately, the Mortgage Bankers Association reported that its measure of 30-year mortgage rates fell to its lowest level since September 2024, fueling a surge in refinancing activity to its highest point since September 2025.

Patricia Zobel, a former manager at the New York Fed and current head of macroeconomic research at Guggenheim Investments, remains skeptical. "It's not clear to me how much this will materially lower housing prices for consumers, but we'll see," she commented, while noting that mortgage bond yields have narrowed slightly relative to Treasury bonds.

Administration officials have provided few details on the purchases, but Treasury Secretary Scott Bessent explained that a key objective is to offset the Federal Reserve's ongoing reduction of its own mortgage bond holdings. The Fed has been allowing bonds acquired during the pandemic to mature without replacement.

Bessent stated the administration's buying pace would "roughly match" the roughly $15 billion in mortgage bonds rolling off the Fed's balance sheet each month. This plan to "sterilize" the Fed's runoff is viewed with skepticism by many economists. Most analysts agree that the market impact of the Fed's balance sheet changes comes primarily from the initial announcement, not the gradual runoff itself. They argue that the central bank's modest reduction in holdings—from $2.7 trillion in mid-2022 to $2 trillion—is creating no measurable upward pressure on home borrowing costs, questioning the need for an offsetting action.

Federal Reserve officials have also indirectly expressed doubts about the program's effectiveness, consistently pointing to the supply side of the housing equation.

"I do think that a lot of the housing affordability challenges are about more than just financing, and there's a supply and demand issue that has persisted in many major markets," said Atlanta Fed President Raphael Bostic in a January 9 interview.

Minneapolis Fed President Neel Kashkari was more direct. "The biggest barrier for the housing market is supply," he said. "Anything we can do to help get out of the way of allowing more supply to come online... that will help the housing market probably more than anything else."

Even if the bond-buying program were to lower rates, external factors could easily reverse the effect. A recent selloff in Japanese bonds has caused yields on longer-dated government bonds to spike, putting upward pressure on U.S. rates.

Furthermore, President Trump's own actions on the global stage, including tariff threats and diplomatic friction with allies over issues like the proposed purchase of Greenland, may be diminishing the appeal of U.S. assets. This could weaken demand for Treasuries, which would in turn push borrowing costs higher. The 10-year Treasury note yield, which heavily influences mortgage rates, recently rose to its highest level since August, creating a significant headwind for anyone hoping for lower mortgage payments.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up