Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

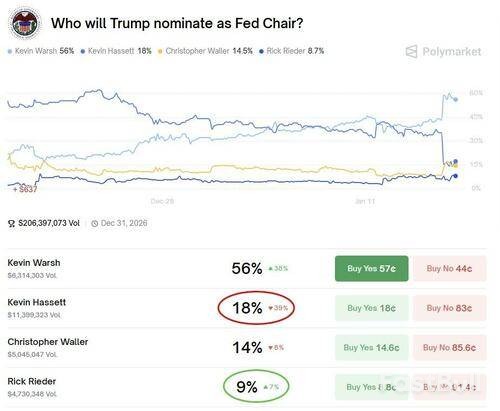

BlackRock's Rieder meets Trump, igniting Fed Chair speculation with his unconventional low-rate stance.

BlackRock executive Rick Rieder’s recent meeting with President Donald Trump has ignited speculation that the bond market heavyweight is a serious contender to become the next chair of the Federal Reserve.

The meeting immediately raises the profile of Rieder, who serves as BlackRock's chief investment officer for global fixed income. Over the last decade, this role has made him one of the most powerful voices in global bond markets. While he lacks direct experience within the Fed or in a government policy position, his opinions on monetary policy are closely monitored by investors and officials.

Rieder has built a reputation on his view that interest rates have been kept higher than necessary for the current economic landscape. He has consistently argued that the Federal Reserve should be prepared to lower rates toward a more neutral level, which he suggests is closer to 3 percent.

His perspective is shaped by decades of navigating credit markets, leading him to worry that overly restrictive monetary policy could unnecessarily strain the financial system and curb economic growth. Rieder believes the Fed has focused too much on historical inflation data and risks overtightening, especially as financial conditions are already helping to cool the economy. He advocates for a broader focus on overall financial health rather than a narrow obsession with inflation metrics.

Adding to his unique profile, Rieder has often downplayed concerns about large government deficits. He contends that structural forces, such as aging demographics, high global savings, and strong demand for U.S. assets, make these deficits more manageable than many critics believe.

At times, Rieder has also questioned the conventional wisdom that inflation must be strictly controlled, suggesting that a rate slightly above the Fed's target may not be harmful if it helps stabilize debt and support employment. These views resonate with Trump's long-standing calls for a central bank leader who favors lower interest rates. Still, nominating a Wall Street asset manager to lead the world's most important central bank would be a highly unconventional move.

As Rieder’s candidacy gains momentum, the field of potential nominees is shrinking. Last week, Trump indicated that economic adviser Kevin Hassett is no longer in the running, stating he prefers to keep Hassett in his current role at the White House. This removes a prominent name from the list of contenders.

With Hassett out, the race now centers on a smaller group. Besides Rieder, the most frequently mentioned candidates are former Fed governor Kevin Warsh and current governor Christopher Waller. Both Warsh and Waller offer deep experience within the central banking system and would represent more traditional choices compared to Rieder's market-oriented background.

Treasury Secretary Scott Bessent has confirmed that a decision is expected soon, noting that Trump aims to announce his pick before or shortly after the Davos forum. Rieder’s meeting at the White House signals that the president is actively considering both conventional and non-traditional candidates to shape the future of U.S. monetary policy.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up