Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

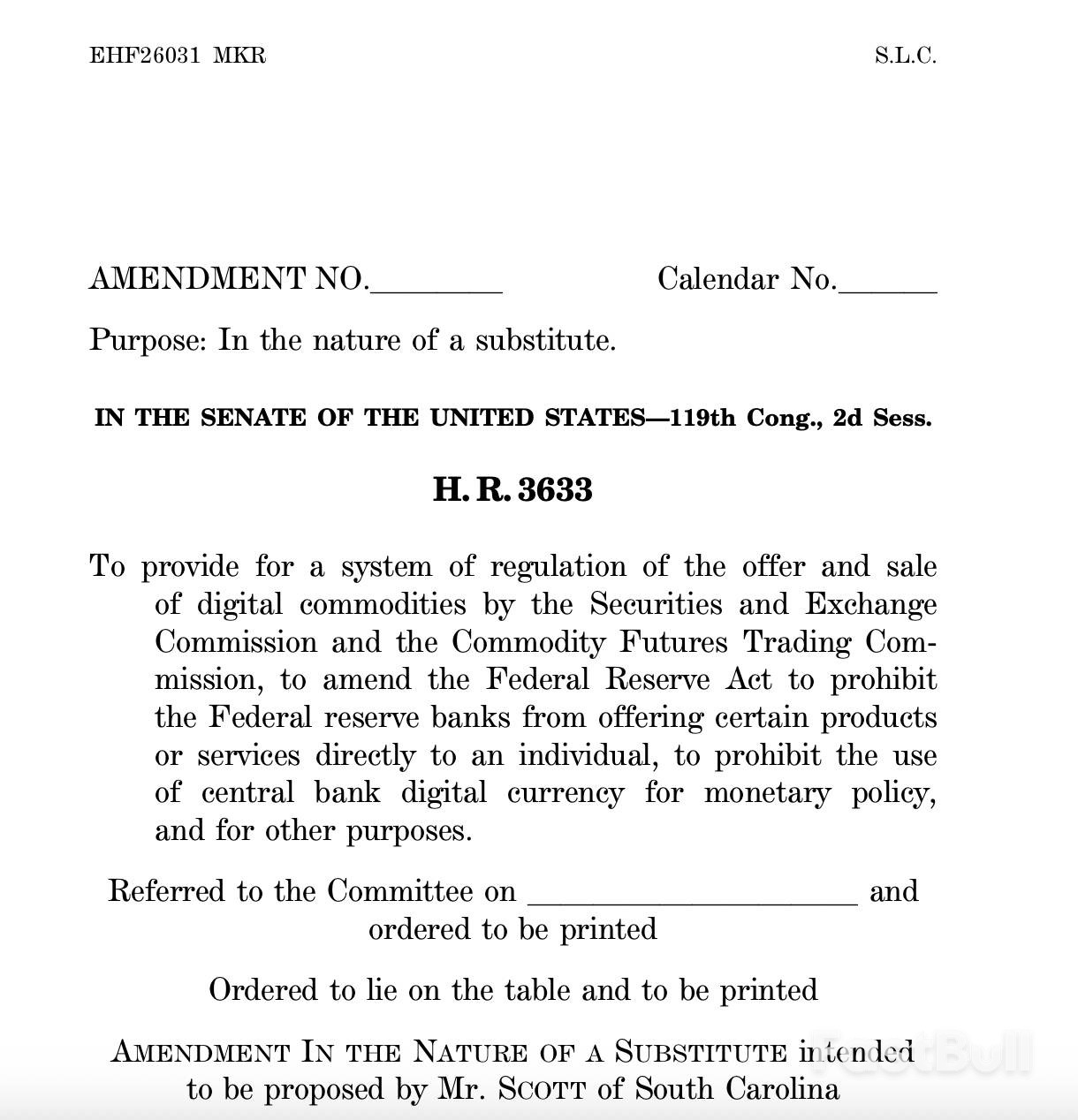

A new Senate crypto bill proposes banning passive stablecoin yields, aiming to balance industry and banking interests.

U.S. senators are preparing to review a major piece of crypto legislation this week that could fundamentally change how stablecoin holders earn rewards. An amended draft of the Digital Asset Market Clarity Act proposes new rules that would directly impact interest and yield payments on these digital assets.

According to the draft released on Monday, the bill aims to restrict certain types of returns. The text states that "a digital asset service provider may not pay any form of interest or yield [...] solely in connection with the holding of a payment stablecoin." This language effectively targets and bars passive, deposit-like returns that users might earn simply for holding stablecoins in an account.

However, the proposal doesn't eliminate all forms of stablecoin rewards. The draft carves out exceptions for more structured and active participation in crypto ecosystems.

What Types of Rewards Are Still Allowed?

The bill clarifies that stablecoin rewards would not be prohibited under specific circumstances, including earnings derived from:

• Providing liquidity or collateral

• Governance activities

• Validation or staking

• Other forms of ecosystem participation

This distinction signals that lawmakers may be responding to industry criticism calling for clearer rules, while also addressing concerns from traditional finance. Some banking groups have lobbied against stablecoin rewards in other legislation, such as the GENIUS Act signed into law in July.

Nic Puckrin, co-founder of Coin Bureau, views the proposal as a compromise between crypto industry demands and pressure from banks.

"The Senate's compromise on stablecoin yield in the proposed amendments to the crypto market structure bill is a clear sign that the powers that be are committed to ensuring stablecoins remain attractive to end users, while placating banks that have lobbied heavily against such rewards," Puckrin stated.

He added that regardless of the outcome, the competitive dynamic is set. "Whichever way the chips fall, though, it's clear stablecoins will remain a competitor to bank deposits. Short of an outright ban on any form of rewards, there's little that can stop this, and this is a new reality banks will have to reckon with."

The legislative journey for the bill is complex. The Senate Banking Committee is scheduled to hold a markup on Thursday, a key step that could advance it for a full Senate vote. However, the Senate Agriculture Committee announced on Monday that it would not review its version of the bill until the end of January.

This split timeline creates significant risk. "If the bill fails in either committee, then market structure is likely to be dead for this session," said Eli Cohen, Chief Legal Officer at Centrifuge. He noted that even a partisan approval could keep the bill alive, stating, "If the bills pass by Republican party line vote, there would still be time to get Democrats onboard before the unified bill goes to the floor for a full Senate vote."

The debate over stablecoin yields is not the only obstacle. Other political factors could derail the bill's progress.

At least two Senate Democrats have reportedly pushed for the CLARITY Act to include safeguards preventing public officials, including presidents, from profiting from investments in digital asset firms.

Furthermore, the upcoming U.S. midterm elections in November could divert legislative attention. The Washington Research Group at TD Cowen speculated that the bill is more likely to pass in 2027, as Democrats consider a potential shift in congressional control after the midterms.

Despite these challenges, some remain optimistic. U.S. Securities and Exchange Commission (SEC) Chair Paul Atkins said Monday he expects Trump to sign the bill into law by the end of 2026. If passed, the legislation would establish a clear regulatory framework for the SEC and the Commodity Futures Trading Commission to oversee the digital asset market.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up