- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Gold hits record highs amid geopolitical and trade uncertainty, while silver's dramatic rally prompts overbought warnings.

Gold prices climbed on Tuesday, continuing a powerful rally driven by geopolitical uncertainty and renewed trade tensions. The precious metal is holding near record highs as investors seek safe-haven assets.

Spot gold rose 1.6% to $5,092.70 per ounce after hitting an all-time high of $5,110.50 on Monday. This marks the first time the metal has breached the significant $5,100 level. Meanwhile, U.S. gold futures for February delivery saw a modest increase of 0.1%, trading at $5,088.40 per ounce.

Analysts point to President Donald Trump's aggressive trade policy as a key catalyst for gold's recent performance. "Trump's disruptive policy approach this year is playing into the hands of precious metals as a defensive play," said Tim Waterer, chief market analyst at KCM Trade. "The threats of higher tariffs to Canada and South Korea are doing enough to keep gold a safe-haven choice."

On Monday, President Trump announced plans to raise tariffs to 25% on certain South Korean imports, including autos, lumber, and pharmaceuticals, citing Seoul's failure to implement a trade deal. This followed recent tariff threats against Canada, which emerged after Canadian Prime Minister Mark Carney's visit to China.

This policy unpredictability, coupled with the risk of a U.S. government shutdown, has pressured the U.S. dollar. A weaker greenback typically makes gold cheaper for buyers holding other currencies, further boosting its appeal.

Christopher Wong, a strategist at OCBC, noted that gold's rally reflects a "material geopolitical, or uncertainty premium" that is "driven less by cyclical factors and more by the persistent uncertainty around geopolitics, policy unpredictability and (loss of) confidence in the dollar."

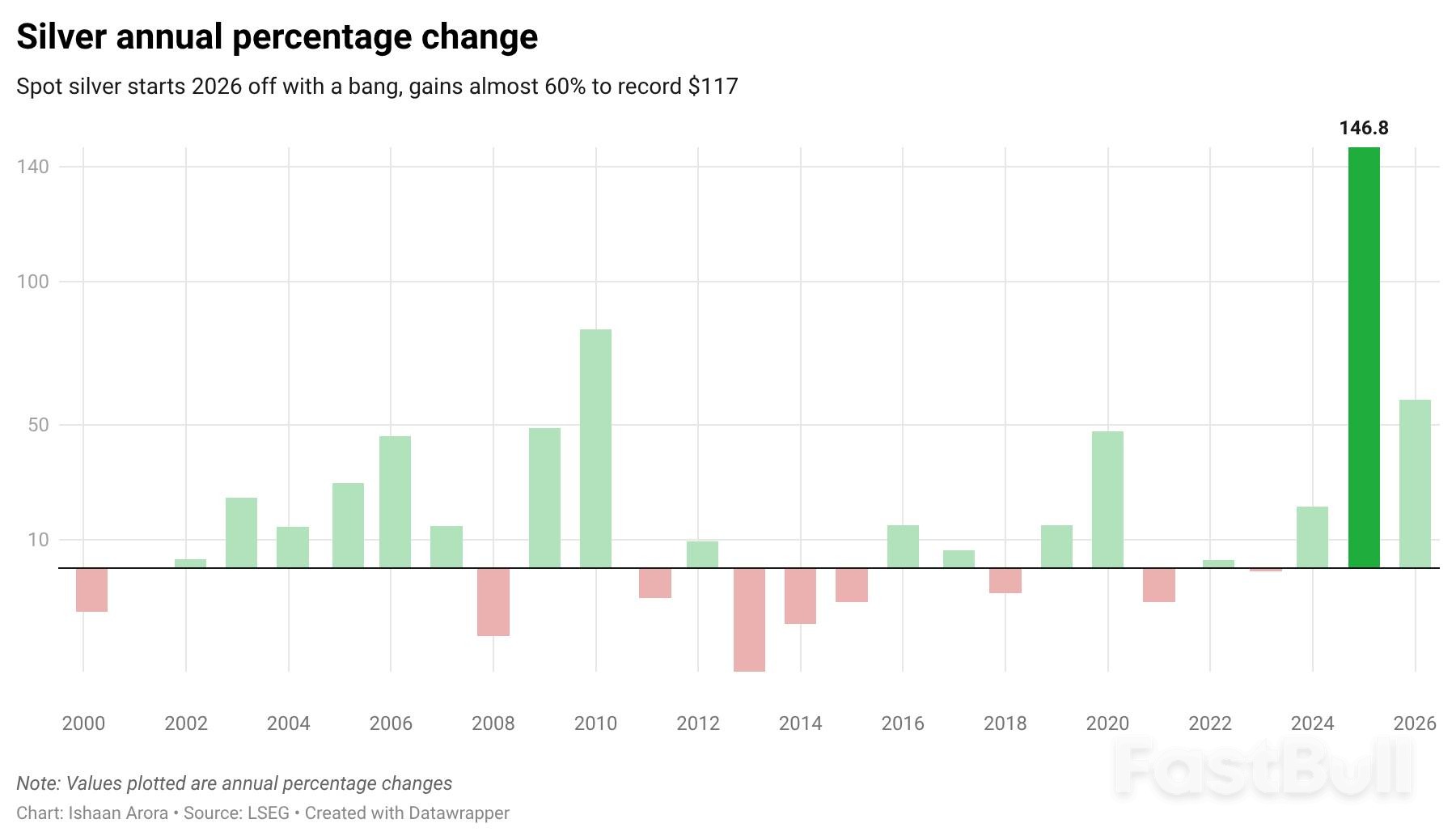

Silver has also experienced a dramatic surge, with spot prices jumping 6.1% to $110.19 an ounce. This follows a record high of $117.69 set on Monday. So far this year, silver is up more than 50%.

However, some analysts are sounding a note of caution. According to a note from BMI, a unit of Fitch Solutions, silver now appears expensive relative to gold. The gold-to-silver ratio has fallen to a 14-year low, suggesting a potential imbalance.

BMI attributed the latest rally to speculative buying and expects prices to ease in the coming months. The firm anticipates that easing supply tightness and peaking industrial demand, partly due to a slowing Chinese economy, could cool the market.

The rally has not extended to all precious metals. Spot platinum fell 2.2% to $2,697.45 per ounce after setting its own record of $2,918.80 in the previous session. In contrast, palladium added 1.1% to reach $2,004.37.

Market participants are also watching the U.S. Federal Reserve, which begins its policy meeting later today. The central bank is widely expected to hold interest rates steady, especially given the challenges posed by the Trump administration's policies to its independence.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up