Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

U.S. President Donald Trump's threatened 30% tariff on European Union imports is complicating the European Central Bank's decision-making but is unlikely to derail plans for a pause in rate cuts next week, five ECB policymakers told Reuters.

U.S. President Donald Trump's threatened 30% tariff on European Union imports is complicating the European Central Bank's decision-making but is unlikely to derail plans for a pause in rate cuts next week, five ECB policymakers told Reuters.

The ECB signalled after its June meeting that it was likely to keep interest rates unchanged on July 23-24.

But the 30% duty floated by Trump is steeper than the ECB had anticipated even under the most negative of three scenarios for the euro zone economy it released last month.

That means the ECB has been forced to come up with new estimates and policymakers to contemplate a more negative outcome than they thought possible in June, said the five sources, all members of the ECB's Governing Council.

They said governors remain reluctant to act on the basis of what is still a threat, however, especially given the sometimes contradictory statements made by Trump's administration since his first announcement of global tariffs in April. Any discussion about rate cuts is therefore likely to be kept for the ECB's September meeting, the sources said.

Trump said on Sunday that his tariffs would kick in on August 1, and the European Commission has also paused its countermeasures until that date.

Market economists have largely said they think it unlikely that Trump will follow through with his tariff threat because of the damage it would cause to the U.S. economy in terms of higher inflation and lower growth.

But should the 30% levy be imposed, they expect the ECB to cut interest rates in response.

Barclays analysts predicted a lowering of the ECB's deposit rate to just 1% by next March from 2% now if the U.S. imposes an average tariff rate on EU goods of 35%, which they estimated would subtract 0.7 percentage points from euro zone growth.

The ECB's latest macroeconomic projections, released in June, pointed to a gradual recovery in the euro zone economy in coming years, with inflation hovering around its 2% target.

Those projections assumed as their baseline a 10% tariff on EU good exports to the U.S., which would put euro zone economic growth at 0.9% this year, 1.1% next year and 1.3% in 2027.

But forecasts under an alternative scenario released at the same time showed that a 20% U.S. tariff would curb growth by 1 percentage point over the same period and also pull down inflation to 1.8% in 2027, from 2.0% in the baseline scenario.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

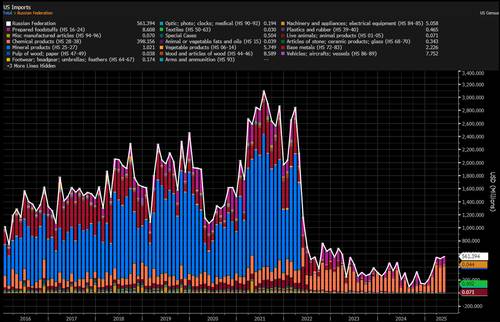

Russia had been gradually but relentlessly taking over more territory (via

Russia had been gradually but relentlessly taking over more territory (via

BTC/USDT order-book liquidity data. Source: Material Indicators/X

BTC/USDT order-book liquidity data. Source: Material Indicators/X Binance BTC/USDT liquidation heatmap. Source: CoinGlass

Binance BTC/USDT liquidation heatmap. Source: CoinGlass