Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Canada's pivotal data week reveals inflation's tenacity and cautious sentiment, guiding the BoC's stable policy into 2026.

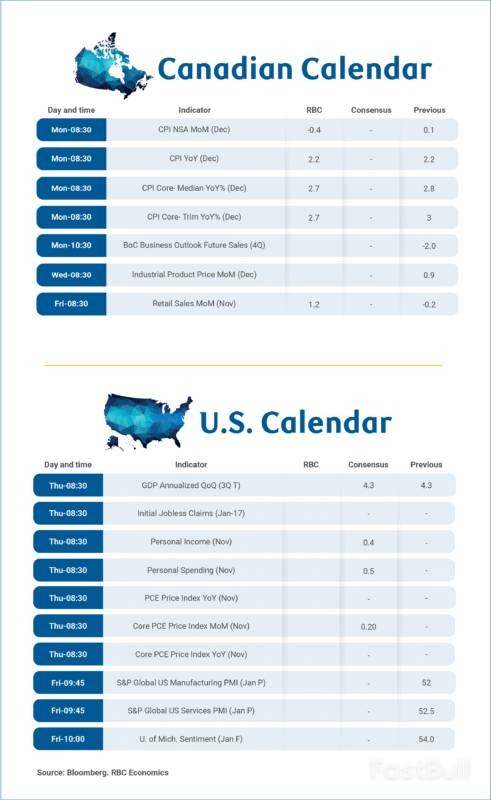

A critical week of Canadian economic data is ahead, featuring the final monthly inflation report for 2025 and the Bank of Canada's (BoC) Q4 Business Outlook Survey on Monday, followed by November's retail sales figures on Friday. These releases will offer crucial insights into the country's economic trajectory heading into the new year.

Headline inflation for December is expected to remain largely unchanged, holding steady at the 2.2% year-over-year rate seen in November. Core price growth trends are also anticipated to show little movement, leaving inflation running moderately above the Bank of Canada's 2% target.

Conflicting Price Pressures

Two key components are pulling the headline number in opposite directions:

• Energy Prices: A significant 8% drop in gasoline prices during December should drag overall energy costs further below last year's levels.

• Food Prices: Food inflation has remained high throughout 2025 after a brief easing in late 2024. Price growth is forecast to climb above 5% in December. This is partly due to base effects from a temporary GST/HST tax holiday on restaurant meals a year prior, but high grocery price inflation, which stood at 4.7% in November, continues to be a major driver.

Core Inflation Remains a Concern

When volatile food and energy products are excluded, inflation is projected to edge down to 2.3% from 2.4% in November. While this would be the second consecutive month of improvement, it's not enough to bring inflation back to the central bank's comfort zone.

The BoC's preferred measures—the median and trim CPI—both registered 2.8% year-over-year increases in November, highlighting persistent underlying price pressures that remain well above the 2% target.

How Tax Policies Skew the Numbers

Year-over-year inflation figures continue to be distorted by government policy changes. The removal of the consumer carbon tax in most provinces last April is still suppressing annual energy price growth. Conversely, the temporary GST/HST tax break that ran from mid-December 2024 to mid-February 2025 will artificially inflate the annual price growth figure for December, though this impact may be limited by an offsetting rise in pre-tax prices a year ago.

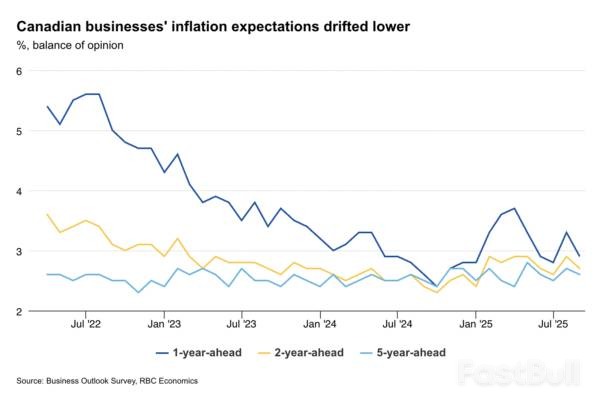

The Q4 Business Outlook Survey, released just ahead of the BoC's next interest rate decision, is expected to paint a familiar picture. The Q3 survey pointed to an economy stabilizing at a subdued level, and the upcoming report will likely show more of the same: muted demand, cautious pricing behavior, and restrained hiring plans among Canadian firms.

Despite some weaknesses, the Bank of Canada likely remains cautiously optimistic. While heavily trade-exposed sectors have underperformed, the worst-case international trade scenarios feared earlier in the year have not materialized.

Furthermore, domestic consumer demand appears resilient. The upcoming retail sales report for November is expected to reinforce this, with Statistics Canada's advance estimate pointing to a strong 1.2% monthly increase. Data from our cardholder spending tracker also showed domestic purchases firming up through the holiday season.

Given this backdrop, the forecast is for the Bank of Canada to leave its overnight rate unchanged throughout 2026. The next policy move is more likely to be a hike, but that is not expected to occur until 2027.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up