Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Bitcoin's value falls below $75,000, challenged by stalled crypto legislation and a hawkish Fed nominee, despite President Trump's close ties to the sector.

Bitcoin's price fell below the $75,000 mark on Monday, retreating to levels last seen before the re-election of U.S. President Donald Trump. The drop comes as investors pivot away from riskier assets and crucial U.S. cryptocurrency legislation faces delays in Congress.

Digital asset markets had experienced a significant surge following Trump's election victory in November 2024, driven by the perception that his administration would be highly supportive of the crypto sector. Just one month after the election, Bitcoin crossed the $100,000 threshold for the first time—a milestone publicly celebrated by the president.

However, the asset’s trajectory has been volatile. After a sharp decline in April below $75,000, triggered by the announcement of wide-ranging U.S. tariffs that unsettled global markets, Bitcoin resumed its climb. It eventually reached a record high of $126,251.31 in October before beginning its latest pullback.

A primary driver behind the recent downturn is persistent regulatory uncertainty in the United States. While Congress successfully passed a law in July to regulate stablecoins, a more comprehensive crypto bill known as the Clarity Act has stalled in the Senate.

This legislative delay is creating a significant challenge for the market. "Expectations for progress on the Clarity Act have not been met," explained James Butterfill, a researcher at digital asset manager CoinShares. He described the ongoing uncertainty as a major "headwind" on cryptocurrency prices.

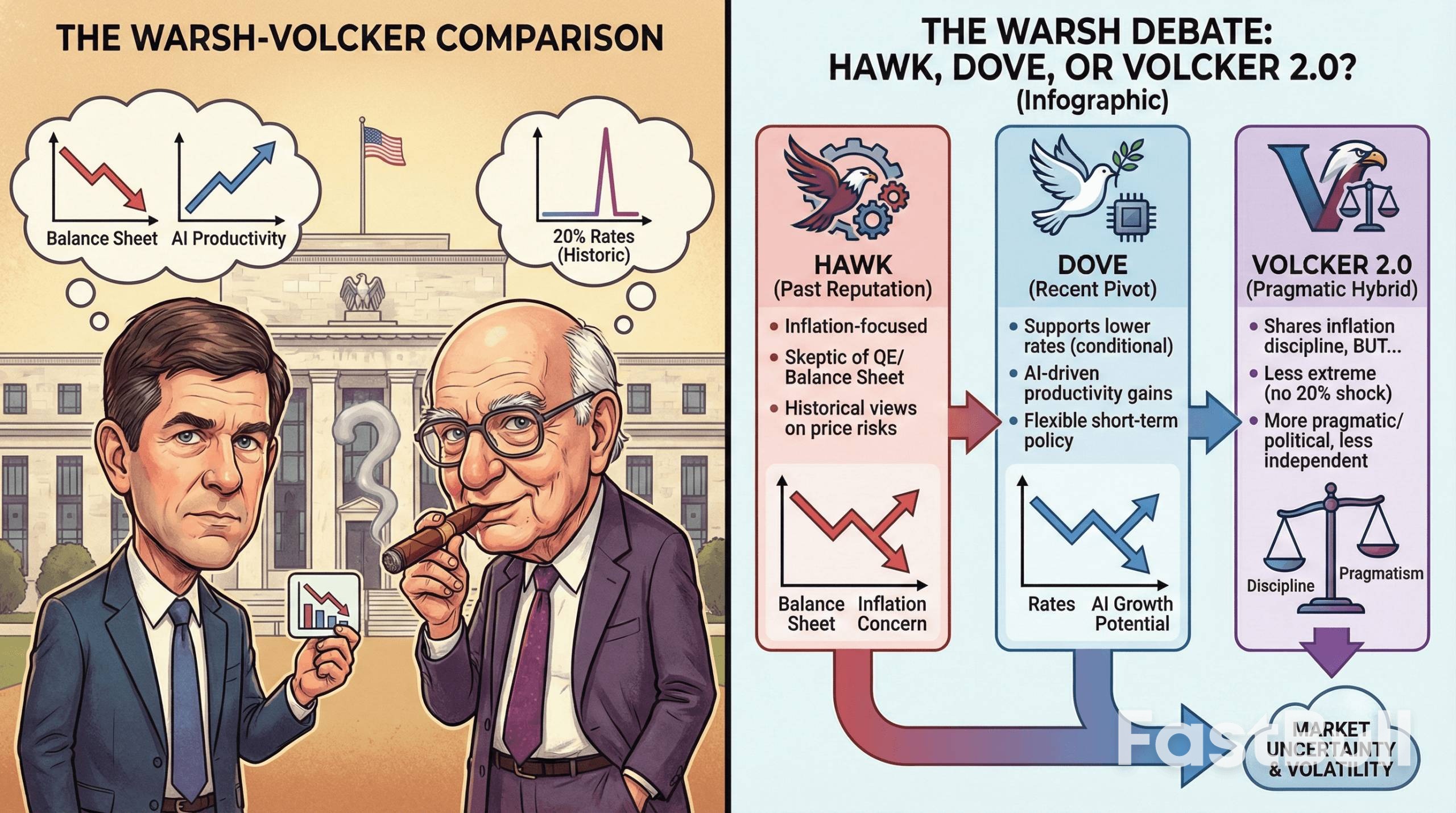

Bitcoin's decline accelerated after President Trump announced on Friday his nomination of former U.S. Federal Reserve governor Kevin Warsh to lead the central bank.

Market observers view Warsh as a strong defender of the Fed's independence. His nomination helped reassure traditional financial markets, leading investors to sell safe-haven assets like gold and silver, which saw their prices plunge. At the same time, many investors also liquidated their cryptocurrency holdings and other risky assets to raise cash.

President Trump's close connections to the cryptocurrency industry have drawn accusations of potential conflicts of interest since his return to the White House. He has actively promoted his own crypto-related ventures while in office.

According to recent estimates from Bloomberg, the Trump family's fortune increased by $1.4 billion in the last year from their digital asset holdings alone.

Further intertwining his presidency with the sector, the 79-year-old billionaire launched his own cryptocurrency, $TRUMP, just hours before his inauguration in January 2025. After an initial surge, the coin has since lost approximately 90% of its value from its peak.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up