Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

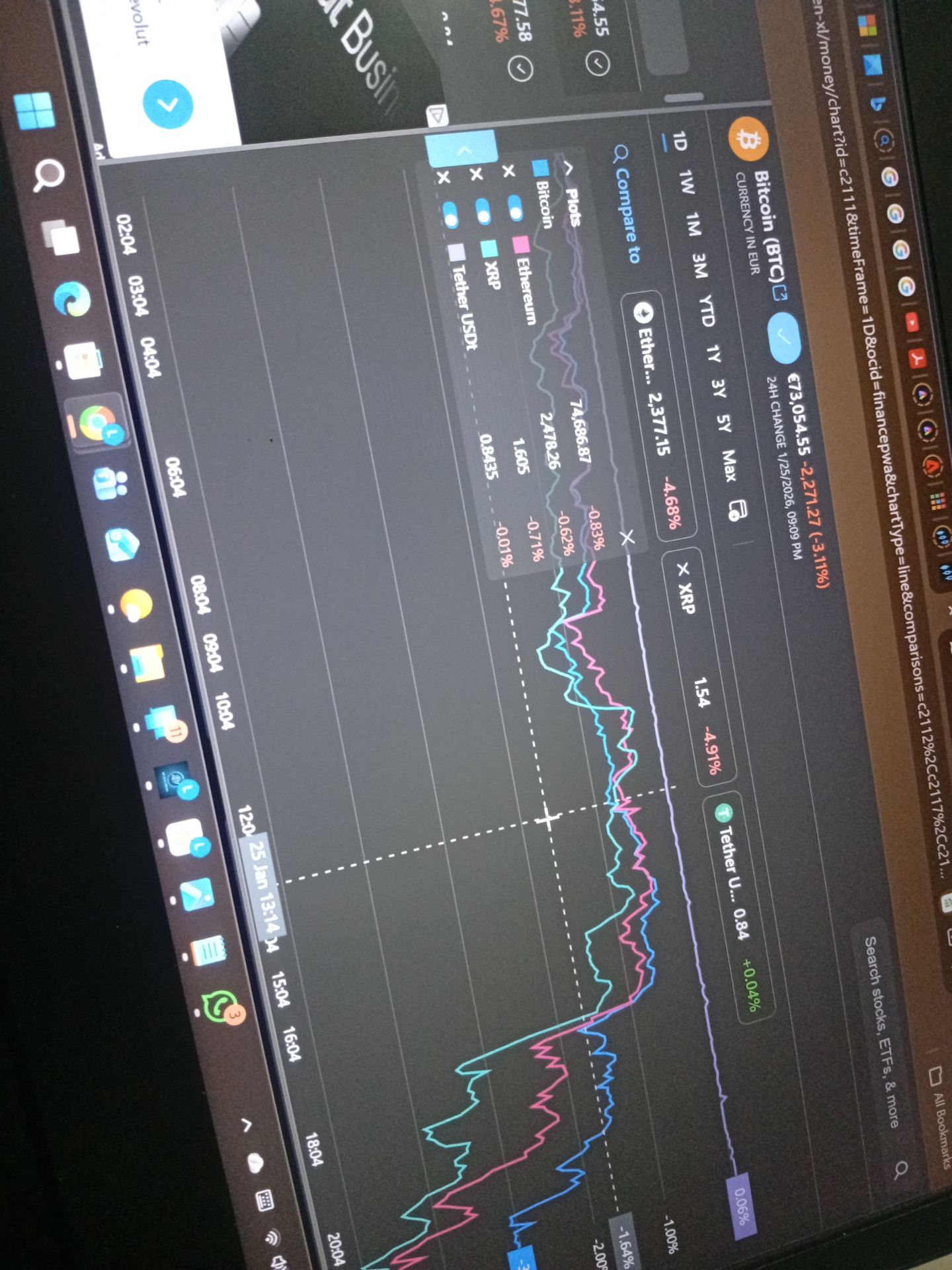

Bitcoin surges past $97K amid Fed policy debates, with deregulation emerging as a potential inflation-buster.

Bitcoin's price has soared past $97,000, hitting a high not seen since last November as U.S. markets opened for trading. The surge comes as traders navigate a complex economic landscape, with a postponed Supreme Court decision on tariffs and an anticipated January announcement from the White House adding to the uncertainty.

Amid these developments, the central question for investors is what to expect from the Federal Reserve's upcoming financial declarations.

Federal Reserve official Miran, who also serves as a representative for Trump, has been a vocal advocate for reducing interest rates. He has repeatedly stressed the need for rate cuts to support the economy.

However, strong employment data from last week has tempered expectations for an immediate policy shift. The robust jobs report makes it highly unlikely that the Federal Reserve will lower rates during its January session.

A key argument for a more accommodative monetary policy centers on the potential impact of deregulation. Proponents believe that reducing regulatory burdens could stabilize prices and enhance economic productivity by expanding supply capabilities.

According to Miran, failing to align monetary policy with deregulation would lead to an "overly restrictive" environment that unnecessarily hinders growth. His long-term vision includes a goal to lift approximately 30% of regulations by 2030, a move he estimates could slice inflation by half a percentage point each year.

He explained his reasoning:

"Deregulation should exert downward pressure on prices, offering another reason for us. The central bank is expected to reduce interest rates. Deregulation introduces a positive supply and productivity shock, enhancing the economy's capacity while alleviating price pressures. If central banks do not counteract the effects of deregulation, policy becomes overly restrictive, unnecessarily inhibiting growth."

While today's Producer Price Index figures were conflicting, any clear sign that inflation is falling below 3% would make it easier for the Fed to consider a shift toward a neutral interest rate. President Trump has also argued that a combination of tariffs, deregulation, and immigration policies would contribute to lower inflation.

The current scenario presents several key takeaways for investors and market watchers:

• No Imminent Rate Cut: The Federal Reserve is widely expected to hold interest rates steady in its upcoming January meeting, primarily due to strong employment figures.

• Deregulation's Potential: Proposed deregulation stands out as a potential catalyst for significant economic benefits, including reduced inflation and enhanced productivity.

• Persistent Uncertainty: The deferral of the Supreme Court's decision on tariffs adds another layer of uncertainty to market expectations.

Although Miran's perspective on interest rate cuts may not yet represent the consensus view within the Federal Reserve, the broader economic and regulatory environment continues to fuel speculation and drive volatility in markets like Bitcoin.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up