Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Data Interpretation

Bond

Political

Forex

Remarks of Officials

Economic

Central Bank

Technical Analysis

Traders' Opinions

Stocks

Daily News

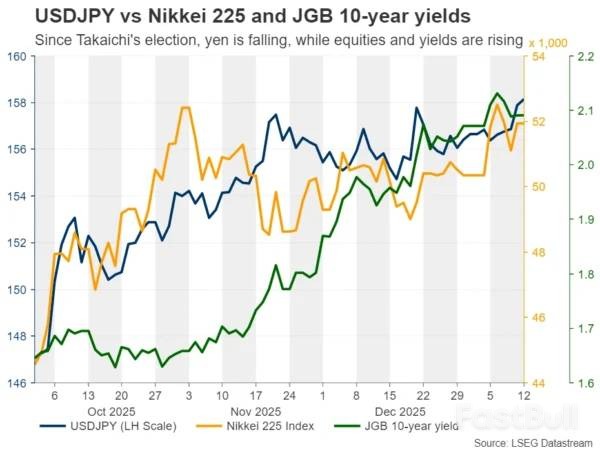

Snap election prospects and fiscal spending plans are fueling a "Takaichi trade," sinking Japan's yen and challenging BoJ policy.

The Bank of Japan (BoJ) started 2025 with a hawkish stance, raising interest rates to their highest level in three decades and signaling more hikes could follow. However, this failed to lift the Japanese yen, as traders sought more specific timing for the next policy move.

The yen's situation worsened dramatically after Kyodo News reported that Prime Minister Sanae Takaichi is considering a snap election in February. The news sent the currency into a steep decline, reaching lows not seen since July 2024.

With a 70% approval rating, Takaichi may be positioning for a decisive victory to push through her spending plans, which would further increase Japan's already large government debt. This prospect has triggered what analysts are calling the "Takaichi trade": a falling yen accompanied by soaring stock prices and Japanese Government Bond (JGB) yields. This trend could intensify if the ruling Liberal Democratic Party appears likely to secure a single-party majority.

Compounding the pressure on the yen is the market expectation that the BoJ will be reluctant to tighten monetary policy ahead of an election. This suggests the next interest rate hike may not come until after the spring wage negotiations, and only if they result in substantial salary increases.

As the USD/JPY exchange rate pushes back toward the psychological 160.00 level, talk of government intervention is resurfacing. Finance Minister Satsuki Katayama expressed concern over the "one-way weakening of the yen" during a meeting with US Treasury Secretary Scott Bessent, who shared her concerns and called for the BoJ to raise interest rates.

This follows Katayama's warning in December, when USD/JPY crossed 157.00, that Japan has a "free hand" to act. Her recent meeting with Bessent may have been to secure tacit approval from the U.S., making direct intervention near the 160.00 zone a more credible threat.

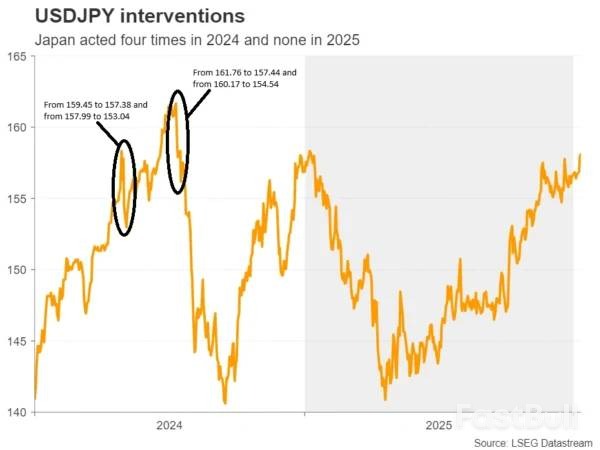

Despite these warnings, the yen has continued its slide, raising questions about the potential effectiveness of intervention. In 2024, Japanese authorities intervened four times to support the currency.

• April 2024: Two interventions provided only temporary relief before the yen resumed its decline.

• July 2024: Two more interventions had a more lasting impact, driving USD/JPY from around 162.00 to below 140.00 by September. This success was attributed to the intervention being followed by a BoJ rate hike.

Given Takaichi's agenda of increased spending, any currency intervention on its own may have a limited and short-lived effect. A lasting reversal for the yen likely requires a supporting rate hike from the BoJ, especially since a weaker currency could fuel inflation through higher export costs and ultimately harm economic growth.

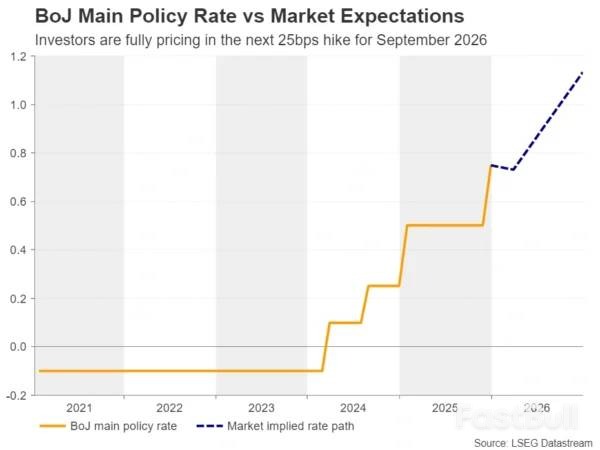

However, financial markets are not convinced a rate hike is imminent. According to Japan's Overnight Index Swaps (OIS) market, a 25-basis-point hike is not fully priced in until September. If the BoJ holds off on tightening policy, intervention alone may not be enough to stop the yen's decline.

Without a policy shift, yields on Japanese debt will likely continue to rise as fewer investors are willing to finance the nation's growing debt. While Japanese equities have rallied on the prospect of fiscal stimulus, this may not last. Eventually, concerns about inflation and an economic slowdown could lead investors to sell off Japanese assets in a "Sell Japan" event.

Ultimately, unless the Ministry of Finance intervenes and the Bank of Japan follows with a rate hike, the yen is likely to extend its downtrend, with USD/JPY potentially trading above 160.00 soon.

From a technical perspective, the USD/JPY pair is currently challenging the 158.90 resistance level, which marks the peak from January 10, 2025. A decisive close above this level could open the door to a test of the 160.00 mark.

The broader uptrend, defined by the trendline drawn from the September 17 low, remains firmly in place. If the pair breaks above 160.00, the next major target would be the July 3, 2024 high of around 162.00. For the bullish trend to be questioned, bears would need to force a decisive break below the 154.55 support zone.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up

Nasdaq - daily

Nasdaq - daily Nasdaq - 4 hour

Nasdaq - 4 hour Nasdaq - 1 hour

Nasdaq - 1 hour