Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Indexes: Dow down 0.3%, S&P 500 flat, Nasdaq up 0.2%.Strategy gains as MSCI keeps crypto treasury firms in indexes.Private payrolls rebound less than expected in December.

Jan 7 (Reuters) - Wall Street's main indexes were mixed on Wednesday, with the S&P 500 and the Dow coming off their intraday record highs after rallying in the previous two sessions, while investors assessed numerous economic datasets.

At 10:09 a.m. ET, the Dow Jones Industrial Average (.DJI), opens new tab fell 145.00 points, or 0.30%, to 49,317.08, the S&P 500 (.SPX), opens new tab gained 0.78 points, or 0.01%, to 6,945.60, and the Nasdaq Composite (.IXIC), opens new tab gained 53.51 points, or 0.23%, to 23,600.68.

The Dow slipped from its record high and remained about 1.5% below the historic 50,000 level, while modest moves in the S&P 500 kept it at a record high, leaving the benchmark 0.7% shy of the 7,000-point peak.

Wall Street surged on Tuesday amid renewed enthusiasm for artificial-intelligence-linked stocks.

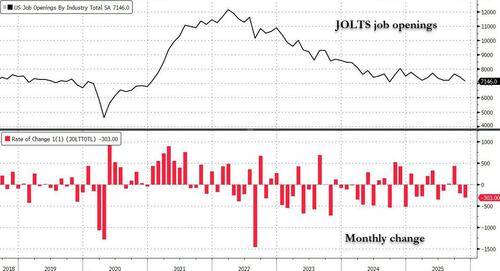

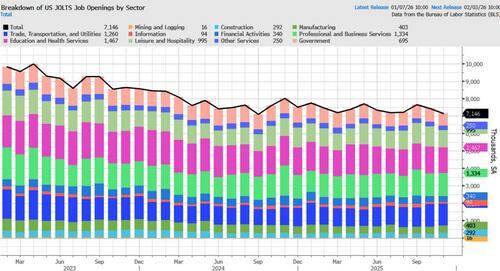

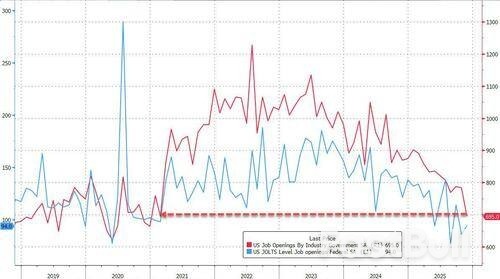

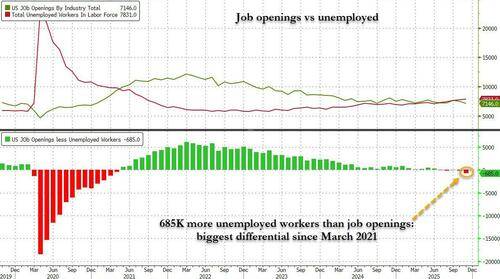

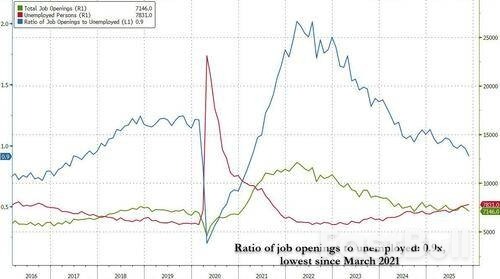

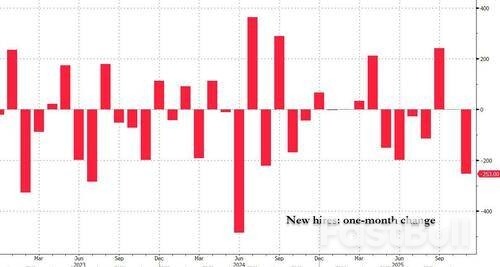

U.S. job openings fell more than expected in November after rising marginally in October, while a separate ADP report showed that private payrolls increased less than expected in December.

Kim Forrest, chief investment officer at Bokeh Capital Partners, said that investors could stay cautious over the next couple of days, avoiding any outsized bets until the key nonfarm payrolls report is released on Friday.

Healthcare (.SPXHC), opens new tab extended its gains on Wednesday, up 1.1% to hit a record high, boosted by a 4% rise in heavyweight drugmaker Eli Lilly (LLY.N), opens new tab. The Wall Street Journal reported on Tuesday that Eli Lilly was in advanced talks to buy Ventyx Biosciences (VTYX.O), opens new tab for more than $1 billion.

Memory chipmakers that had surged in the previous session on the prospect of chip shortages leading to price increases eased. SanDisk (SNDK.O), opens new tab and Western Digital (WDC.O), opens new tab fell 2.6% and 10.2% after climbing 27.5% and 10%, respectively, on Tuesday.

Materials (.SPLRCM), opens new tab also pulled back, down 1.6%, after climbing over 2% in the previous session.

Wall Street's three main indexes appear to have started 2026 on a positive note, after marking their third consecutive year of double-digit gains in 2025.

Markets will also keep an eye on geopolitical developments, including developments in Venezuela and the use of the country's oil resources, following the capture of Venezuelan President Nicolas Maduro over the weekend.

U.S. President Donald Trump said the U.S. would refine and sell up to 50 million barrels of crude stuck in the Latin American nation.

The U.S. said it has seized a Russian-flagged, Venezuela-linked tanker on Wednesday, marking Washington's efforts to dictate oil flows in America's backyard and force Caracas' socialist government to become its ally.

The White House said on Tuesday that Trump is discussing options for acquiring Greenland, including potential use of the U.S. military.

Among other stocks, Strategy (MSTR.O), opens new tab rose 1.5% before the bell after MSCI dropped a plan to exclude the bitcoin hoarder and other crypto treasury firms from its indexes.

First Solar (FSLR.O), opens new tab fell 8.2% after Jefferies downgraded the solar panel maker's rating to "hold" from "buy", citing recent project cancellations and margin pressures.

Declining issues outnumbered advancers by a 1.56-to-1 ratio on the NYSE, and by a 1.19-to-1 ratio on the Nasdaq.

The S&P 500 posted 24 new 52-week highs and 8 new lows, while the Nasdaq Composite recorded 62 new highs and 33 new lows.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up