Markets

News

Analysis

User

24/7

Economic Calendar

Education

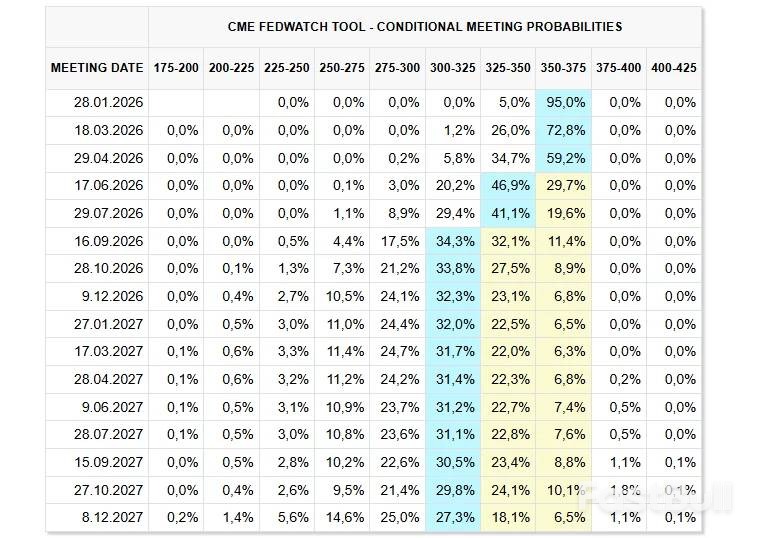

Data

- Names

- Latest

- Prev

US Treasury Secretary Bessent noted the won's depreciation contradicts Korea's strong economy amidst crucial trade talks.

U.S. Treasury Secretary Scott Bessent has stated that the Korean won's recent depreciation is inconsistent with South Korea's robust economic fundamentals, according to a statement from the Treasury Department on Wednesday.

The comments were made during a meeting in Washington this week with South Korea's Finance Minister, Koo Yun-cheol. The discussion comes amid growing concerns in Seoul over the won's decline against the U.S. dollar.

During the Monday meeting, Secretary Bessent noted that the won's performance does not align with the strength of Korea's economy. He also emphasized that "excess volatility" in the foreign exchange market is "undesirable."

The Treasury Department's release reaffirmed this stance, highlighting Bessent's view that Korea's strong economic output, particularly in key industries that support the American economy, makes it a "critical partner for the United States in Asia."

The two finance ministers also reviewed the implementation of a major bilateral trade and investment agreement. Under the terms of the deal, South Korea has committed to investing US$350 billion in the United States. In return, the U.S. will lower "reciprocal" tariffs on Korean products from 25 percent to 15 percent.

Secretary Bessent expressed his desire for a smooth implementation of the deal, underscoring its potential to deepen the economic partnership between the two nations and help "promote the revitalization of America's industrial might."

The meeting was part of a broader agenda. On the same day, Bessent and Koo participated in a U.S.-hosted meeting of finance ministers focused on securing supply chains for critical minerals. This initiative is a key component of Washington's strategy to counter China's increasing influence over the global supply of vital resources.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up