Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The S&P 500 has “gone green” for the year to date. A few days ago, the US headline stock market index climbed to a point where it is now higher than it was at the start of January.

The S&P 500 has “gone green” for the year to date. A few days ago, the US headline stock market index climbed to a point where it is now higher than it was at the start of January.

It’s still below its (US dollar terms) all-time high set on 19th February. But it really doesn’t have to climb that much further to set a fresh record.

That’s quite the turn-up for the books really, I think most of us would agree. I mean, what about all that tariff stuff? I know that US president Donald Trump has been rowing back a bit from the most extreme levels of tariffs, but the status quo has not returned by any manner of means.

And what about the whole question of interest rates and what happens next with the bond market? Because, you know, if tariffs aren’t going to be the thing that fills the US deficit now, what will? And how will those promised tax cuts be paid for?

You can see why people might be feeling a bit confused. And the truth is, I think it’s sensible to feel confused, or at least not to place too much conviction in any one view. Uncertainty is, of course, the nature of things, but there are times when conditions are supportive of higher levels of confidence in certain outcomes.

This is most definitely not one of those times. Something that has stood out to me in recent weeks is that the traders and investors whose work I follow most closely — those on my “must read” list — are in “low conviction” mode. They’re taking stock, rather than piling in with big aggressive views on what’s going to happen next.

The “End Of US Exceptionalism” Trade Is Still On

So let’s take a step back ourselves, so as not to lose sight of our current thesis here — which is that “US exceptionalism” is over.

US exceptionalism (in the markets sense at least) refers to the fact that US markets have outperformed “non-US” markets handsomely since just after the global financial crisis in 2008. You can tell a long story about why that’s happened but it’s irrelevant to this particular conversation.

The recent period of outperformance was unusually long, and that has led to a certain sense among investors who’ve been trained by experience to “buy the dip,” that the US will never be a place to “underweight.”

Yet US outperformance is not a natural law or an inevitability. There have been many periods during which the US has underperformed — the period between the tech bust and the lead-up to the financial crisis being just one of those. And it’s certainly my view that we’re returning to one of those periods now — where “the rest” beat the US for a while.

Those who have watched the S&P 500 rocket back to its 2025 starting point might be thinking, “well, so much for that.” But there are a number of ways in which the gap between the US and the rest of the world can close.

The obvious one is that US stocks go down and the rest go up. But the gap would also close if all stocks fall, but US ones fall faster — or, as the case is right now, US stocks go up, but others go up faster still.

And so far, this is exactly what’s been happening. I’ll switch to using sterling as the measuring stick, because the majority of my readers pay their taxes in pounds.

In sterling total return (ie including dividends) terms, since the start of the year, the S&P 500 is still down 6%. The FTSE 100 by contrast, is up 5.5%. That’s a punchy outperformance in anyone’s book. The MSCI World index excluding the US — which is an index of 22 developed markets — is up by 6%. And the MSCI Emerging Markets index is up 3%.

In short, the gap is still closing. And so far I don’t see any reason to expect this theme to end soon. Clearly, I’ve been talking about the UK a lot here as an under-appreciated market to explore as a potential beneficiary of the US losing its “only place to own” status.

But there are many other options to investigate too. As I’m writing this, Michael Hartnett of Bank of America (for my money, one of the best mainstream strategists out there), has put out a note arguing that “nothing will work better than emerging market stocks.”

There’s a big wide world out there. Don’t get panicked into ignoring it by a sense of FOMO because the US has rebounded from its April lows.

Send any feedback to jstepek2@bloomberg.net and I’ll print the best. Or ping any questions to merrynmoney@bloomberg.net.

Looking at wider markets — the FTSE 100 is up 0.5% at around 8,670. The FTSE 250 is up 0.5% at 20,950. The 10-year gilt yield is sitting at 4.61%, lower on the day, as are yields on its German and French peers.

Gold is down 2.5% at $3,160 an ounce, and oil (Brent crude) is up about 0.2% to $64.70 a barrel. Bitcoin is up 0.2% at $103,690 per coin, while Ethereum is up 3.3% at $2,620. The pound is down 0.1% against the US dollar at $1.328, and down 0.2% against the euro at €1.186.

Follow UK Markets Today for up-to-the-minute news and analysis that move markets.

Sign up for Bloomberg UK’s daily morning market newsletter, The London Rush. It’s all you need to get you up to date on the most important UK market-moving stories every morning. Get it delivered every day.

The main stories to watch out for next week include:

If you haven’t yet subscribed to the Merryn Talks Money podcast, I highly recommend you do so. Apple folk can subscribe here ; fellow Android users, you could go with Spotify , or just the podcast app of your choice.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

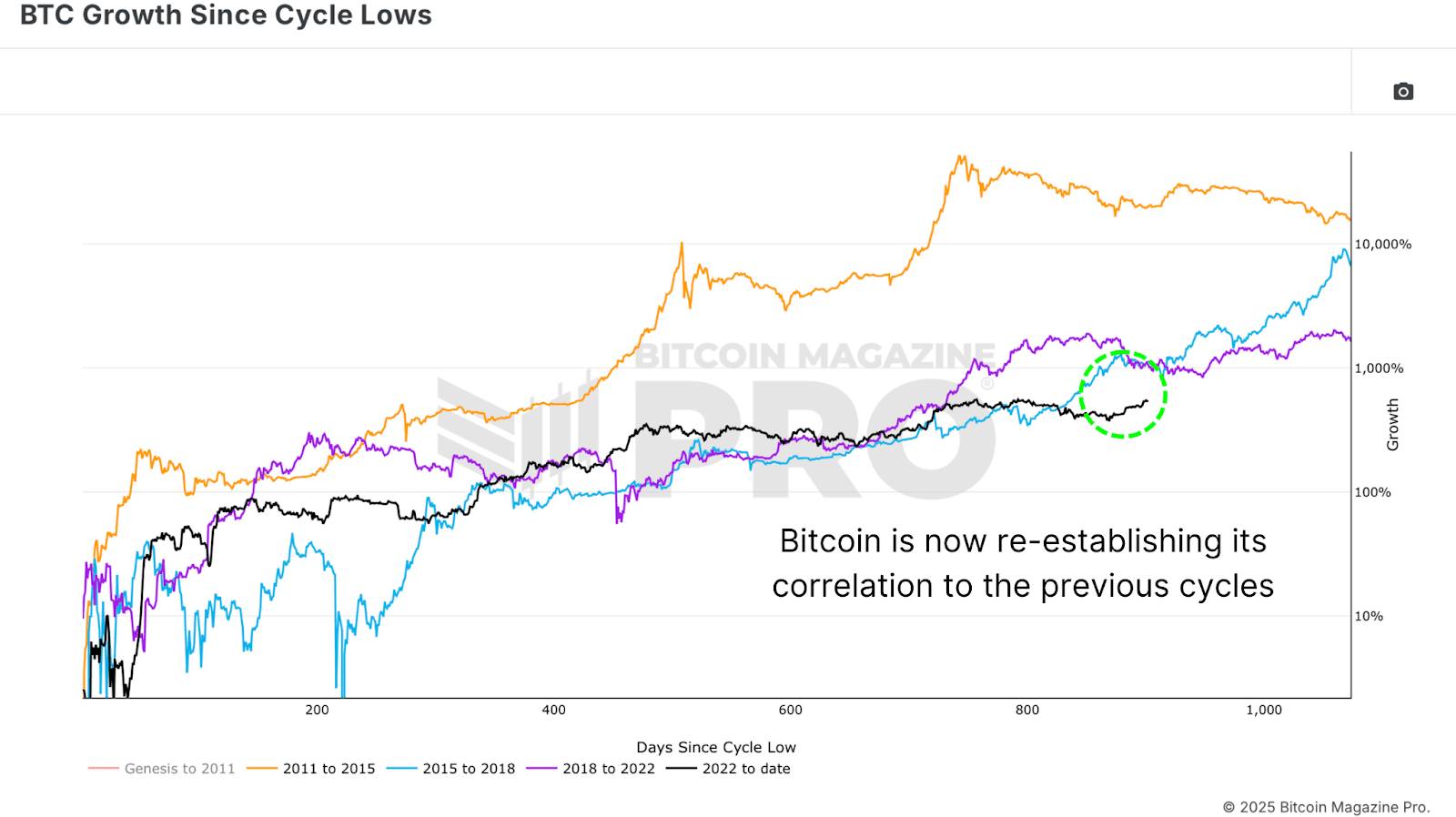

Figure 1: Bitcoin’s 2025 bullish price action mirrors previous cycles.

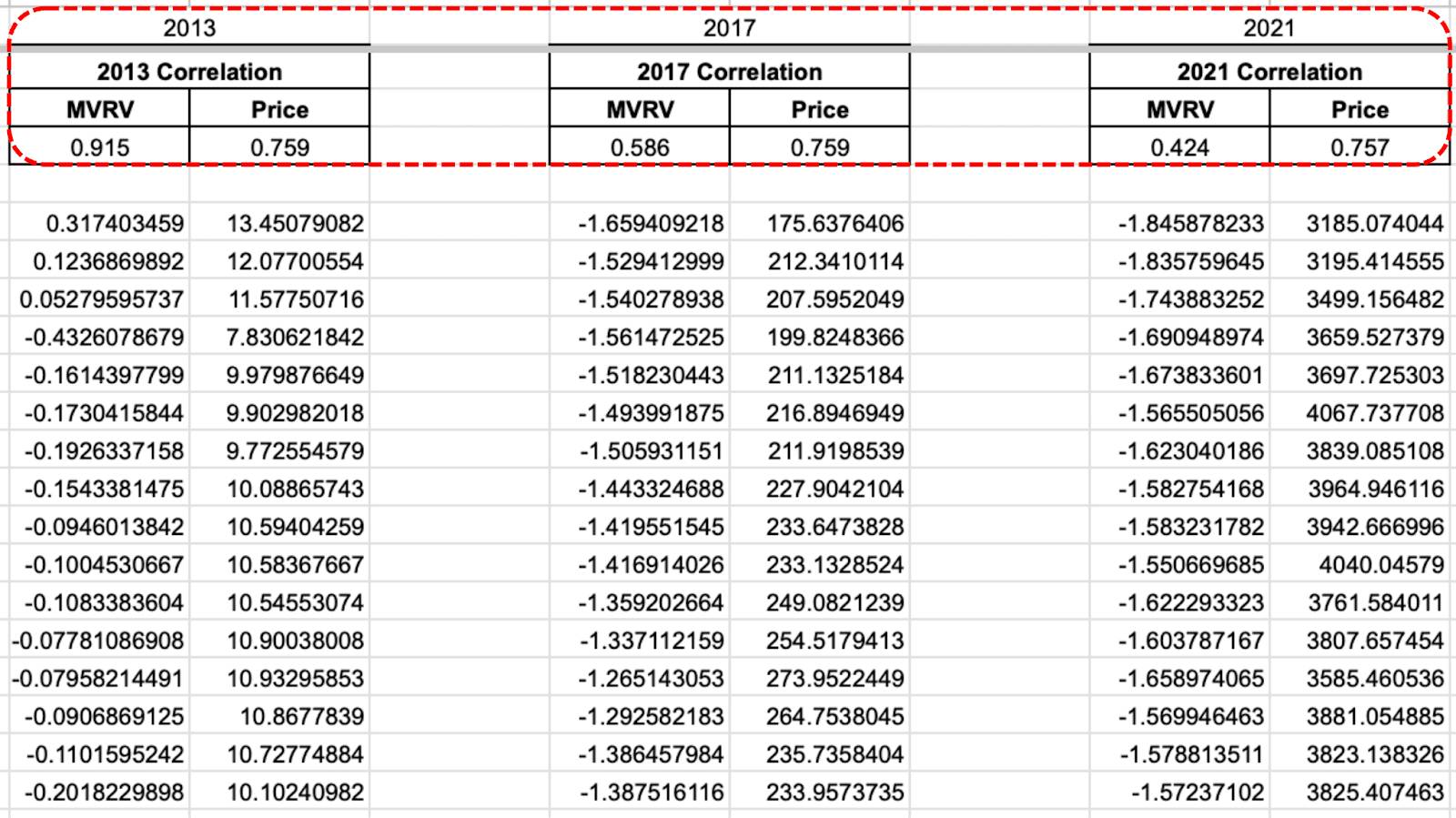

Figure 1: Bitcoin’s 2025 bullish price action mirrors previous cycles. Figure 2: MVRV-Z Score shows behavioral similarities to the 2017 Bitcoin bull run.

Figure 2: MVRV-Z Score shows behavioral similarities to the 2017 Bitcoin bull run.  Figure 3: Cross-cycle behavioral correlations using rolling MVRV-Z scores and price action.

Figure 3: Cross-cycle behavioral correlations using rolling MVRV-Z scores and price action. Figure 4: The rate of change in the 1+ Year HODL Wave suggests confidence in future Bitcoin prices.

Figure 4: The rate of change in the 1+ Year HODL Wave suggests confidence in future Bitcoin prices.  Figure 5: A repeat of 2017’s exponential Bitcoin price growth may be ambitious.

Figure 5: A repeat of 2017’s exponential Bitcoin price growth may be ambitious.