Markets

News

Analysis

User

24/7

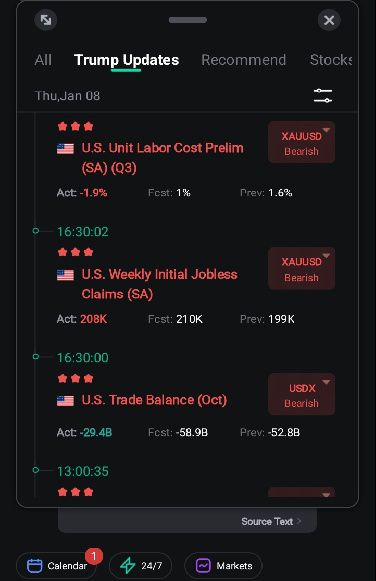

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Seoul seeks Beijing's help with North Korea's nuclear program, signaling a strategic diplomatic shift to improve ties.

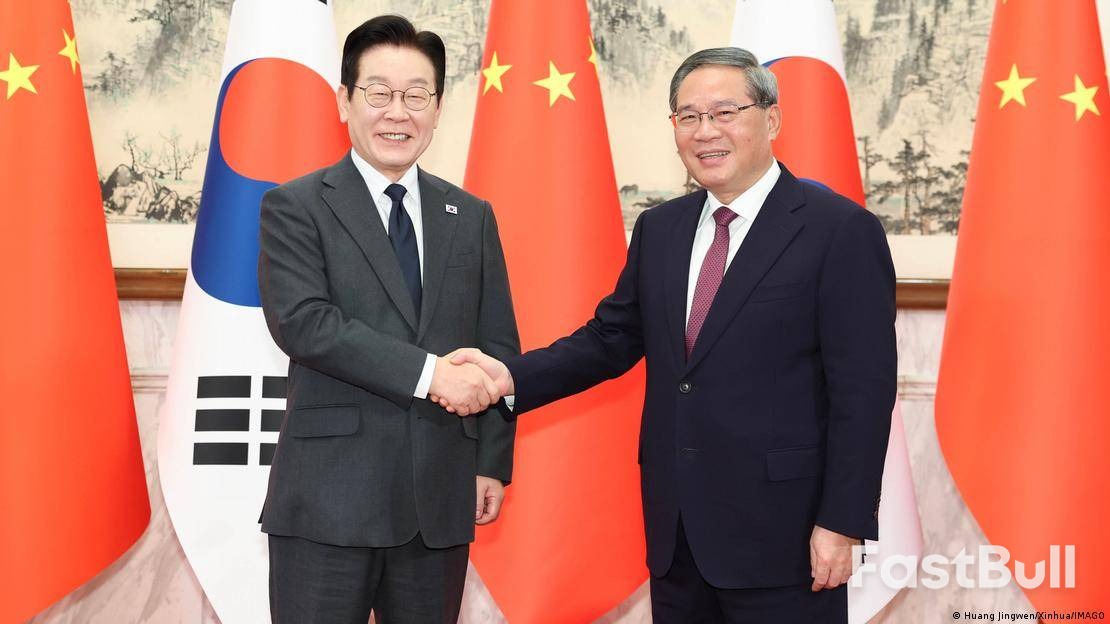

South Korean President Lee Jae Myung has formally requested China's assistance in containing North Korea's nuclear program, signaling a push to improve relations with Beijing and open a "new phase" of diplomatic ties.

The request was made during a meeting with Chinese President Xi Jinping in Beijing on Monday, with Lee later providing details to journalists in Shanghai on Wednesday. This marks the first visit to Beijing by a South Korean president in six years.

President Lee stated that he asked President Xi for China to assume a "mediating role" on the Korean Peninsula, particularly concerning North Korea's advancing nuclear capabilities.

"I would like China to play a mediating role on issues related to the Korean Peninsula, including North Korea's nuclear program. All our channels are completely blocked," Lee explained. "We hope China can serve as a mediator — a mediator for peace."

According to Lee, Xi advised him to show "patience" toward North Korea amid the current high tensions. Lee also acknowledged that past military actions by Seoul could have been perceived as threatening by Pyongyang.

While affirming that a "nuclear-free Korean Peninsula" remains Seoul's long-term goal, Lee outlined a more immediate objective aimed at freezing Pyongyang's progress.

"Just stopping at the current level — no additional production of nuclear weapons, no transfer of nuclear materials abroad, and no further development of [intercontinental ballistic missiles (ICBMS)] — would already be a gain," he said.

Lee reported that Seoul and Beijing had reached a "consensus" on these issues during his visit.

The diplomatic outreach comes as North Korea continues to conduct a series of ballistic missile tests and enhance its nuclear arsenal, which its leader, Kim Jong-un, has framed as a necessary deterrent against the United States.

Lee, who took office in June 2025, represents the left-leaning Democratic Party of Korea (DPK), which traditionally advocates for stronger engagement with China and a less confrontational stance toward North Korea than its rival, the People Power Party (PPP).

This diplomatic initiative highlights South Korea's complex strategic position. China stands as its top trading partner, yet Seoul maintains a robust defense alliance with the United States, requiring a delicate balance in its foreign policy.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up