Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The U.S. reinstated South Korea to its currency watch list, deeming the won's depreciation "excessive."

The U.S. government has decided to keep South Korea on its foreign exchange monitoring list, a move that market analysts believe will have a limited immediate impact on the currency market. However, the decision sends a strong signal, with both Washington and Seoul now indicating that the Korean won's recent slide against the dollar is "excessive," fueling expectations of future appreciation.

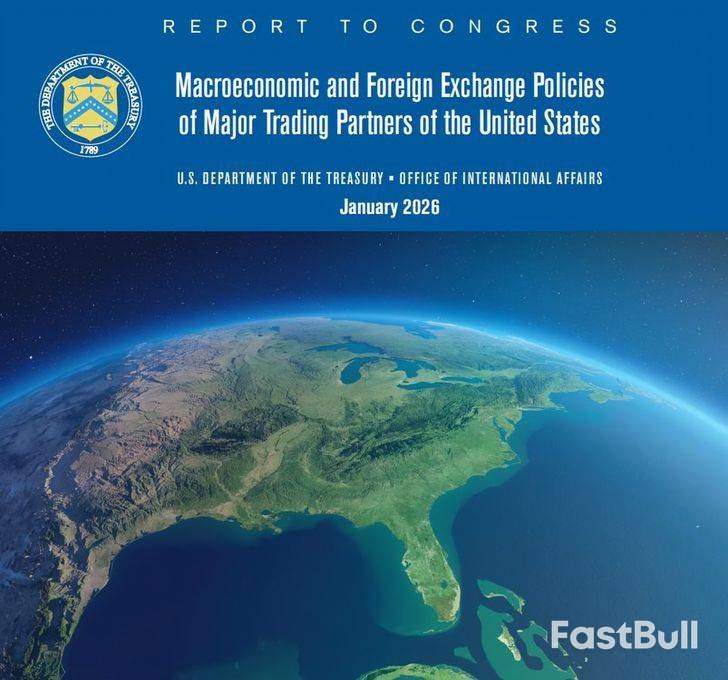

The U.S. Treasury Department announced the decision in its semiannual "Report to Congress on Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States." South Korea was removed from the list in November 2023 after more than seven years but was reinstated in November 2024, preceding the inauguration of the Donald Trump administration.

Treasury Secretary Scott Bessent linked the move to a broader policy shift. "In support of President Trump's America First trade policy, starting with this report, Treasury is strengthening its analysis of trading partners' currency policies and practices," he stated.

Officials in Seoul described the designation as a procedural matter. A senior presidential official noted the decision was made in a "mechanical manner" based on the U.S. Treasury's evaluation framework. "The Treasury reiterated in its report that the recent depreciation of the won does not correspond to Korea's economic fundamentals," the official said, adding that close communication between the two governments will continue.

This view was echoed by Korea's Ministry of Economy and Finance, which said the report reflects Washington's concern over the won's prolonged, one-sided weakening trend since the latter half of last year.

The U.S. Treasury report went beyond monitoring, identifying key drivers behind the won's weakness. It stated that the currency's decline in the latter half of 2025 was inconsistent with South Korea's strong economic fundamentals.

The primary source of downward pressure, according to the report, was capital outflows from the private sector. This trend was largely driven by a significant increase in overseas equity investments by individual Korean investors.

The report also pointed to several structural factors contributing to this capital flight:

• The dominance of large corporations in the domestic economy.

• Conservative corporate dividend policies.

• Limited return prospects in the domestic capital market.

These conditions have prompted both households and institutional investors to move capital abroad, adding to the depreciation pressure on the won.

Market experts agree that Korea's inclusion on the monitoring list is unlikely to cause significant short-term volatility.

"The impact of being placed on the list should be minimal," said Park Sang-hyun, an analyst at iM Securities. "What matters more is the U.S. Treasury's judgment that the won is undervalued relative to fundamentals, a view that has also been echoed by the presidential office. That assessment suggests upward pressure on the currency."

Lee Min-hyuk, chief economist at KB Kookmin Bank, also downplayed the immediate effect, calling the designation a "familiar issue" for markets. However, he emphasized the importance of the underlying message.

"With U.S. Treasury officials, including Secretary Bessent, having openly described the won's weakness as excessive... markets may interpret this as unease in Washington over current exchange-rate levels, potentially capping further increases in the rate," Lee explained.

In the Seoul foreign exchange market on Friday, the won-dollar exchange rate closed at 1,439.5 won, a rise of 13.2 won for the dollar.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up