- USDX

- XAUUSD

- XAGUSD

- WTI

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

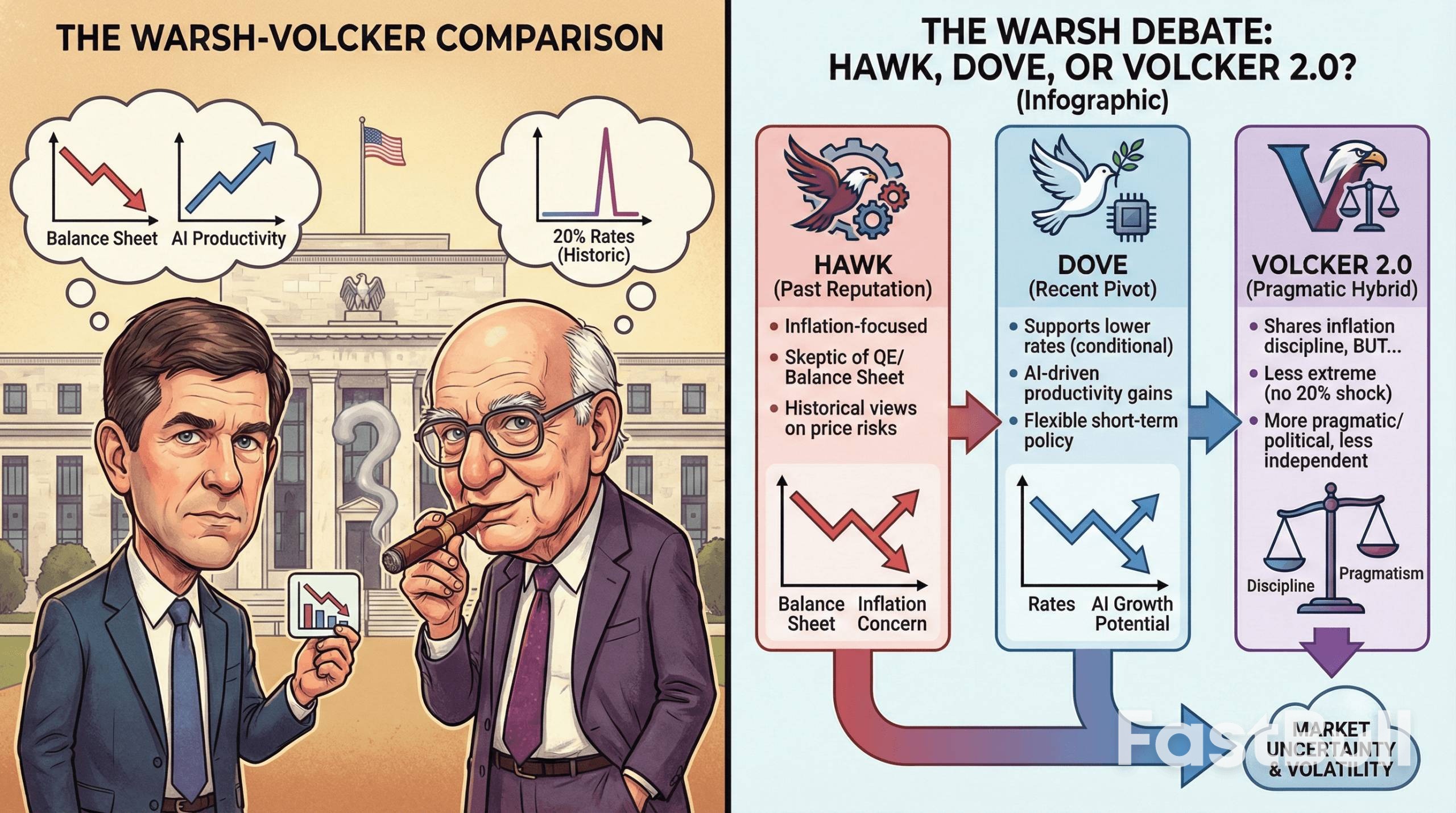

Kevin Warsh's Fed Chair nomination reveals a complex figure, blending hawkish discipline with pragmatic flexibility.

Investors are trading the nomination of Kevin Warsh for Federal Reserve Chair as if Paul Volcker himself just walked back into the Eccles Building. But is Warsh truly the inflation hawk his reputation suggests? The answer is far more complicated.

President Trump announced the nomination on January 30, 2026, positioning Warsh as a figure who can restore discipline at the central bank as Jerome Powell's term ends in May. The move comes after Trump's repeated criticism of the Fed's rate policy and independence, placing Warsh’s monetary philosophy squarely in the spotlight.

Warsh’s record provides ample fuel for the hard-money narrative. As a Fed governor from 2006 to 2011, he built a reputation as one of the board's most consistent voices on inflation. Even as the 2008 financial crisis unfolded, pushing unemployment up and sparking fears of deflation, Warsh persistently warned that inflation expectations could become unanchored.

"Inflation risks, in my view, continue to predominate as the greater risk to the economy," he stated at the time.

After leaving the Fed, this view solidified. Warsh became a prominent critic of quantitative easing (QE), arguing that the central bank's expanding balance sheet distorted capital allocation and dangerously blurred the lines between monetary and fiscal policy. He has maintained that inflation isn't a random event but the direct result of excessive spending and money creation.

"My overriding concern about continued QE, then and now, involves the misallocations of capital in the economy and the misallocation of responsibility in our government," Warsh said in 2018.

This history triggered a classic hawkish reaction in markets upon his nomination. Gold and silver sold off, the dollar strengthened, and traders immediately began making comparisons to Volcker.

However, the full picture is more complex. In recent years, Warsh has also criticized Powell’s policy for being too restrictive and hindering economic growth. He has argued for both lower interest rates and a smaller Fed balance sheet, signaling a willingness to cut rates if accompanied by structural reforms.

This dual position has divided analysts.

• One camp sees intellectual consistency: They believe Warsh's goal is to shrink the Fed's overall footprint, which in turn creates the flexibility to ease short-term rates.

• Another camp sees political pragmatism: They suggest Warsh is adapting his views to align with Trump's well-known preference for lower interest rates.

The tension in Warsh's platform fuels comparisons to Paul Volcker, but the analogy has clear limits. Volcker, the Fed's 12th chairman, inherited runaway inflation in the late 1970s and broke its back by raising the federal funds rate above 20%, knowingly inducing a recession to restore the Fed's credibility. Warsh has neither faced such an extreme scenario nor indicated he would deploy similar economic shock therapy.

Furthermore, Volcker was defined by his staunch independence from political pressure. Warsh is widely seen as more pragmatic and attuned to political realities, making it less likely he would wage a public war against the administration that appointed him.

This doesn't make him a dove; it makes him conditional. While Warsh views inflation control as non-negotiable, he also believes productivity gains, particularly from artificial intelligence, could enable lower rates without stoking price pressures. If the economy delivers on that productivity promise, he may appear accommodative. If inflation surges, the hawk would likely reemerge.

Markets are still trying to solve the puzzle. Fed funds futures are pricing in more rate cuts for 2026, even as traders prepare for a potentially faster reduction of the Fed's balance sheet. This suggests the market is bracing for a hybrid Fed—one that is structurally tighter but potentially looser in its rate signaling.

If confirmed, Warsh could also bring back an old-school communication style. This would mean less forward guidance and more emphasis on actions over promises. Such a shift away from verbal interventions could increase market volatility as traders adjust to a central bank that speaks less but acts more decisively.

Ultimately, Warsh is not a simple Volcker successor. He shares a skepticism of easy money but not an appetite for inflicting economic pain. For investors, the message is clear: ignore the simple labels. Warsh is neither a committed hawk nor a predictable dove. He is a pragmatist who believes in credibility and will likely respond to data, not dogma, making his tenure anything but certain.

Key Points on a Warsh-Led Fed

• Hawkish Credentials: Warsh has a long-standing record of prioritizing inflation control and opposing prolonged quantitative easing.

• Dovish Flexibility: He has recently supported lower interest rates, provided they are paired with balance-sheet reduction and productivity gains.

• The Volcker Parallel: He shares Volcker's focus on monetary discipline but likely lacks his predecessor's tolerance for extreme rate hikes and political confrontation.

• Potential Policy Mix: A Warsh-led Fed might combine faster balance-sheet runoff with targeted rate cuts and a less predictable communication strategy.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up