Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Japan's politicians eye record forex profits for policy, but experts warn of currency intervention implications.

A hot-button topic has emerged in Japan's lower house election campaign: using the nation's massive foreign currency reserves to pay for new policies. Prime Minister Sanae Takaichi brought the issue to the forefront, but analysts warn that tapping into this fund is more complicated than it seems.

During a campaign speech, Takaichi, who leads the ruling Liberal Democratic Party, pointed to a potential source of cash. "There's something called the Foreign Exchange Fund Special Account (FEFSA), and its coffers are brimming now," she said.

Both ruling and opposition parties are now eyeing this account as a way to finance their agendas.

The FEFSA is the government's tool for managing foreign currency reserves and intervening in currency markets. Its operation is straightforward:

• To weaken the yen: The government issues bills to raise yen, sells that yen to buy dollars, and then invests those dollars in assets like U.S. Treasurys.

• To strengthen the yen: It sells its dollar-denominated assets to buy back yen.

The account generates profit primarily because Japan's interest rates have been lower than those of other countries. It earns higher interest on its foreign assets than it pays on the bills it issues. A weaker yen also boosts profits by increasing the yen-denominated value of interest income earned overseas.

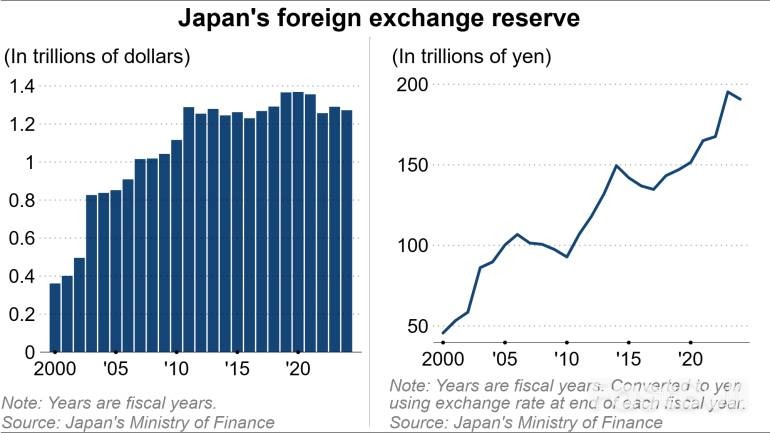

Japan's foreign exchange reserves stood at $1.37 trillion at the end of 2025, according to the Finance Ministry. This figure has been hovering around the $1.3 trillion mark since 2012, swelled by past interventions to buy up dollars.

The FEFSA logged a record gain of 5.36 trillion yen ($34.5 billion) in fiscal 2024, the highest since financial disclosures began in fiscal 2008.

These profits already contribute to the government's general budget. Current rules permit 70% of the gains to be transferred. For fiscal 2025, 3.2 trillion yen was moved to the general account, with about 1 trillion yen allocated to defense spending. Under the existing framework, it would be difficult to extract more funds.

While politicians talk about using unrealized gains from foreign assets, significant obstacles stand in the way.

"By the special forex account's very nature, converting its foreign currency assets to yen would be currency intervention, which imposes some limits on its use as a funding source," said Takahiro Hattori, a project associate professor at the University of Tokyo.

International norms permit currency market intervention only on a limited basis, typically to counter speculative swings. If Japan were to sell its dollar assets for domestic funding when no such crisis exists, it would likely face opposition from the U.S. and could reduce its capacity for necessary interventions in the future.

The idea of using the FEFSA is not limited to the ruling party. Opposition parties also see it as a potential funding source.

The Democratic Party for the People has proposed using investment profits and asset sales from the account, along with pension reserves and Bank of Japan-held ETFs, to fund proactive fiscal policy. Similarly, in last summer's upper house election, the Constitutional Democratic Party suggested using forex account gains to help finance a temporary suspension of the consumption tax on food.

Prime Minister Takaichi later elaborated on her comments in a post on X, stating her goal was not to praise a weak or strong yen but to "build a strong economy that is resilient to exchange rate fluctuations." She pushed back on the interpretation that she "stress[ed] the benefits of yen depreciation" but did not address her remarks about the special account.

As Takaichi noted, a weak yen has both pros and cons. It boosts the profits of Japanese exporters and can lift stock prices. However, it also drives up the cost of imported energy, food, and raw materials, fueling inflation. In recent years, Japan's export volume has stagnated even as the yen has weakened.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up