Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

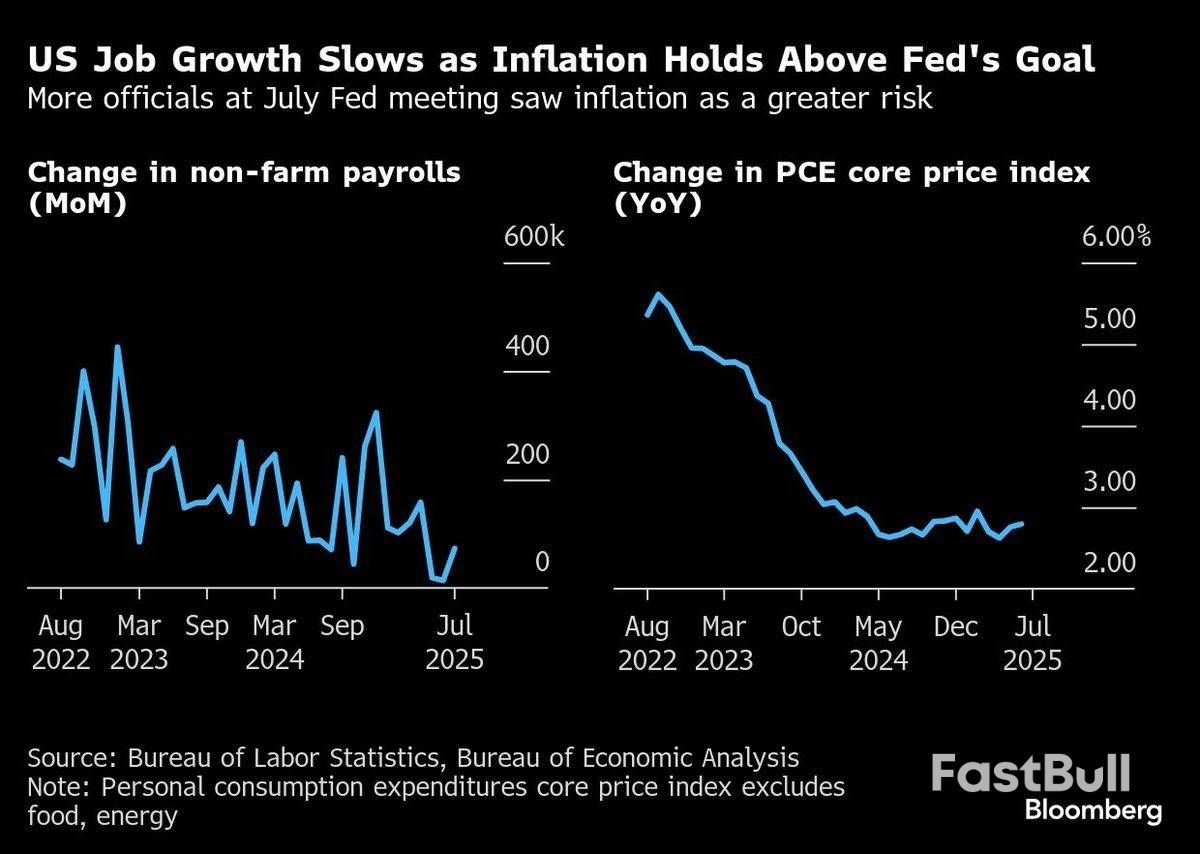

On Friday, Powell hinted the Fed may cut rates next month, saying both labor demand and supply are slowing.

Markets were quiet for most of last week as traders waited for Fed Chair Jerome Powell’s speech at Jackson Hole. Until Friday, the U.S. dollar traded sideways and stocks moved lower as investors wanted to hear if the Fed would confirm a rate cut in September. Economic data before the speech was mostly better than expected, with stronger PMI figures in the U.S., U.K., and Eurozone, higher U.K. CPI, and U.S. home sales beating forecasts. Japan’s core inflation slipped to 3.1% in July, just above expectations, while Canada’s removal of retaliatory tariffs was seen as positive for global trade.

On Friday, Powell hinted the Fed may cut rates next month, saying both labor demand and supply are slowing. He stressed that while tariffs are lifting prices, these effects are likely temporary. His tone was more dovish, and markets reacted strongly—equities surged with the Dow hitting a record high, and the U.S. dollar weakened as the chance of a September rate cut rose to about 90%.

Powell also emphasized that the Fed remains data-driven and independent despite political pressures. With job growth slowing and unemployment risks rising, markets are now waiting for this week’s labor and inflation data to confirm whether the Fed will move at the September meeting.

Markets This Week

The Dow hit new record highs last week after Fed Chair Powell’s Jackson Hole speech, with a September rate cut now seen as highly likely. With the negative impact of U.S. tariffs proving less severe than expected, U.S. stocks remain in a strong upward trend. However, the Dow is currently looking overbought, so a pullback or sideways move is likely at the start of the week, which could provide a buying opportunity for both short- and long-term traders. Key resistance levels are at 46,000 and 47,000, while support is seen at 45,000, 44,000, and 43,000.

After hitting a record high early last week, the Nikkei faced profit-taking ahead of Powell’s speech but later found support at previous highs and closed strongly, following the surge in U.S. equities. The index has risen sharply over the past month and has now moved back below the 10-day moving average, suggesting sideways trading in the short term as investors look ahead to when the Bank of Japan may raise interest rates. Key resistance levels are at 44,000円 and 45,000円, while support is seen at 42,250円, 42,000円, 41,500円, and 41,000円.

The USD/JPY traded sideways for most of last week ahead of the Jackson Hole meetings, before falling sharply after Powell’s speech, as a September U.S. rate cut now looks highly likely. The pair remains in a range, with the 10-day moving average also pointing sideways, making range trading the preferred strategy. However, risks lean to the downside if the Bank of Japan signals it is close to raising interest rates or if upcoming U.S. data disappoints. Resistance is at 148, 149, and 150, while support is at 146 and 145.

Gold initially tested lower last week but recovered strongly as expectations of a U.S. interest rate cut in September supported demand. The market has moved back above the 10-day moving average, breaking the recent downtrend. Overall, gold remains range-bound, but with support holding, the market could continue to test higher levels, making buying on weakness the preferred strategy. Resistance is at $3,400 and $3,450, while support is at $3,300, $3,250, and $3,200.

Crude Oil

Crude oil rebounded in a quiet week, breaking the recent downtrend after closing above the 10-day moving average. Buyers returned as talks to end the Russia–Ukraine war showed little progress, while Powell’s comments on future rate cuts were seen as supportive for demand. With the downtrend now broken, prices are expected to trade sideways in the short term as traders wait for further news from the negotiations. Resistance is seen at $65, $70, and $75, while support is at $60 and $55.

Further selling continued through most of last week after the negative key reversal signal on the daily chart, but the market found strong support at $112,000, the August lows and previous record highs. Powell’s speech was positive for Bitcoin, as lower interest rates make the asset more attractive, though Bitcoin remains in a short-term downtrend. For now, the market is likely to trade sideways, offering range-trading opportunities between $112,000 and $120,000 this week. Resistance is at $120,000, $125,000, and $150,000, while support is at $112,000, $110,000, and $105,000.

This Week’s Focus

This week, traders are still reacting to Fed Chair Powell’s speech at Jackson Hole. His dovish comments raised hopes for a September rate cut, but the question now is whether the dollar will keep falling or if the cut is already fully priced in, leading to a rebound. Powell stressed that the Fed is data-driven, so important U.S. reports on durable goods, GDP, inflation, and consumer confidence will be key. These numbers could quickly change market expectations and create new trading opportunities.

Geopolitics may also play a role. A possible breakthrough in Russia–Ukraine peace talks, though unlikely, would likely lift equities but push oil lower. At the same time, traders are watching the Bank of England for signs of another rate cut, and Japan for a possible rate hike after strong GDP. With central bank signals and global risks in focus, volatility is likely to stay high across currencies, stocks, and commodities.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up