Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

France Trade Balance (SA) (Nov)

France Trade Balance (SA) (Nov)A:--

F: --

France Current Account (Not SA) (Nov)A:--

F: --

P: --

South Africa Manufacturing PMI (Dec)

South Africa Manufacturing PMI (Dec)A:--

F: --

P: --

Italy Unemployment Rate (SA) (Nov)

Italy Unemployment Rate (SA) (Nov)A:--

F: --

P: --

France 10-Year OAT Auction Avg. YieldA:--

F: --

P: --

Euro Zone Consumer Inflation Expectations (Dec)

Euro Zone Consumer Inflation Expectations (Dec)A:--

F: --

P: --

Euro Zone Unemployment Rate (Nov)A:--

F: --

P: --

Euro Zone PPI MoM (Nov)A:--

F: --

P: --

Euro Zone Selling Price Expectations (Dec)A:--

F: --

P: --

Euro Zone PPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Climate Index (Dec)A:--

F: --

P: --

Euro Zone Economic Sentiment Indicator (Dec)A:--

F: --

Euro Zone Services Sentiment Index (Dec)A:--

F: --

Euro Zone Consumer Confidence Index Final (Dec)A:--

F: --

P: --

Mexico 12-Month Inflation (CPI) (Dec)

Mexico 12-Month Inflation (CPI) (Dec)A:--

F: --

P: --

Mexico Core CPI YoY (Dec)A:--

F: --

P: --

Mexico PPI YoY (Dec)A:--

F: --

P: --

Mexico CPI YoY (Dec)A:--

F: --

P: --

U.S. Challenger Job Cuts MoM (Dec)

U.S. Challenger Job Cuts MoM (Dec)A:--

F: --

P: --

U.S. Challenger Job Cuts (Dec)A:--

F: --

P: --

U.S. Challenger Job Cuts YoY (Dec)A:--

F: --

P: --

U.S. Exports (Oct)A:--

F: --

P: --

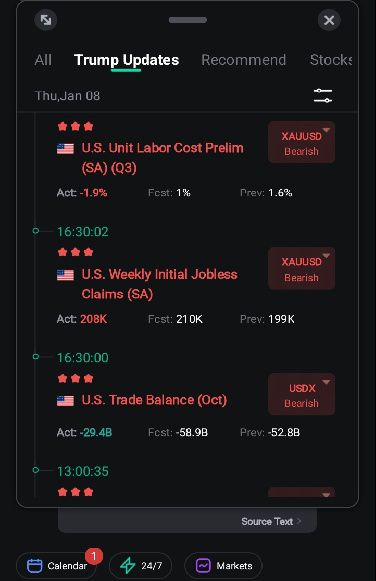

U.S. Trade Balance (Oct)A:--

F: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)A:--

F: --

Canada Imports (SA) (Oct)

Canada Imports (SA) (Oct)A:--

F: --

U.S. Weekly Initial Jobless Claims (SA)A:--

F: --

U.S. Weekly Continued Jobless Claims (SA)A:--

F: --

Canada Exports (SA) (Oct)A:--

F: --

Canada Trade Balance (SA) (Oct)A:--

F: --

U.S. Unit Labor Cost Prelim (SA) (Q3)A:--

F: --

P: --

U.S. Wholesale Sales MoM (SA) (Oct)--

F: --

P: --

U.S. EIA Weekly Natural Gas Stocks Change--

F: --

P: --

U.S. Consumer Credit (SA) (Nov)--

F: --

P: --

U.S. Weekly Treasuries Held by Foreign Central Banks--

F: --

P: --

China, Mainland CPI YoY (Dec)

China, Mainland CPI YoY (Dec)--

F: --

P: --

China, Mainland PPI YoY (Dec)--

F: --

P: --

China, Mainland CPI MoM (Dec)--

F: --

P: --

Indonesia Retail Sales YoY (Nov)

Indonesia Retail Sales YoY (Nov)--

F: --

P: --

Japan Leading Indicators Prelim (Nov)

Japan Leading Indicators Prelim (Nov)--

F: --

P: --

Germany Industrial Output MoM (SA) (Nov)

Germany Industrial Output MoM (SA) (Nov)--

F: --

P: --

Germany Exports MoM (SA) (Nov)--

F: --

France Industrial Output MoM (SA) (Nov)--

F: --

P: --

Italy Retail Sales MoM (SA) (Nov)--

F: --

P: --

Euro Zone Retail Sales MoM (Nov)--

F: --

P: --

Euro Zone Retail Sales YoY (Nov)--

F: --

P: --

Italy 12-Month BOT Auction Avg. Yield--

F: --

P: --

India Deposit Gowth YoY

India Deposit Gowth YoY--

F: --

P: --

Brazil IPCA Inflation Index YoY (Dec)

Brazil IPCA Inflation Index YoY (Dec)--

F: --

P: --

Mexico Industrial Output YoY (Nov)--

F: --

P: --

Brazil CPI YoY (Dec)--

F: --

P: --

U.S. Building Permits Revised MoM (SA) (Sept)--

F: --

P: --

U.S. Building Permits Revised YoY (SA) (Sept)--

F: --

P: --

U.S. Unemployment Rate (SA) (Dec)--

F: --

P: --

U.S. Nonfarm Payrolls (SA) (Dec)--

F: --

P: --

U.S. Average Hourly Wage YoY (Dec)--

F: --

P: --

Canada Full-time Employment (SA) (Dec)--

F: --

P: --

Canada Part-Time Employment (SA) (Dec)--

F: --

P: --

Canada Unemployment Rate (SA) (Dec)--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Dec)--

F: --

P: --

Canada Employment (SA) (Dec)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

French construction activity continued its steep decline in December, extending the sector's downturn to over three-and-a-half years, according to the latest HCOB PMI survey.

French construction activity continued its steep decline in December, extending the sector's downturn to over three-and-a-half years, according to the latest HCOB PMI survey.

The headline HCOB France Construction PMI Total Activity Index registered 43.4 in December, slightly below November's 43.6, indicating a marginally sharper contraction. Any reading below 50 signals a decline in activity.

Unlike November, when housing and commercial activity drove the overall contraction, December's downturn was primarily fueled by the civil engineering sub-sector, which saw its steepest decline since February. Residential building work fell at its softest rate since August 2022, while commercial construction posted its slowest drop in four months.

New orders decreased rapidly as companies reported weak demand conditions and fewer calls for tender. This slump in new business led French constructors to become increasingly pessimistic about the future, with sentiment reaching its lowest level since October 2014.

Approximately 35% of surveyed firms expect activity levels to be lower by the end of 2026, while only 6% anticipate growth.

In response to weak conditions, construction companies continued to reduce purchasing activity, though the pace of decline was the slowest in seven months. Employment in the sector has fallen continuously since May 2024, with December showing the weakest drop in seven months.

Cost pressures intensified for the third consecutive month, with input price inflation reaching its highest level in almost a year, though still below the survey's historical average.

Jonas Feldhusen, Junior Economist at Hamburg Commercial Bank, noted that the construction recession, which began alongside the ECB's rate-hiking cycle in summer 2022, remains deep and persistent. He added that while there are "tentative signs of recovery in residential construction," civil engineering activity "collapsed in December."

Feldhusen pointed to several factors weighing on the sector's outlook, including weak order books, limited room for further ECB rate cuts, France's ongoing fiscal concerns, and political uncertainty.

Following US attacks on Venezuela and the capture of President Nicolás Maduro, President Donald Trump declared that American companies would move in to develop the nation's vast oil sector. His announcement framed Venezuela's resources as a source of "tremendous amount of wealth" ripe for extraction.

This move marks a stark departure from an international system based on rules, suggesting a new era where military power dictates economic rights. For President Trump, however, it's a clear economic opportunity. Venezuela holds the world's largest proven crude oil reserves, accounting for 19.4% of the global total in 2024. Yet, it's currently a minor player, producing just 960,000 barrels per day (b/d) in 2024—a fraction of its 3.3 million b/d peak in 2006.

Reviving this dormant giant is the goal, but the price tag is staggering.

Years of underinvestment, corruption, and sanctions have left Venezuela's oil infrastructure in ruins. According to an estimate from Rystad Energy, simply tripling the country's output from 1 million to 3 million b/d by 2040 would require an investment of $183 billion.

The underlying economics are just as challenging. Most of Venezuela's reserves consist of a viscous, heavy crude that is difficult and expensive to produce. It requires specialized techniques like steam injection for extraction and must be mixed with diluents to flow through pipelines.

This heavy crude also sells at a discount because it demands complex refining to be turned into consumer products like gasoline and diesel. While the sheer scale of the reserves could justify the cost in a high-priced market, global trends are pointing in the opposite direction.

The world consumed roughly 104 million barrels of oil per day in 2025, but a market flooded with supply is putting downward pressure on prices. Since the highs of mid-2022, which were driven by post-lockdown demand and Russia's invasion of Ukraine, the price of Brent crude has been in a gradual decline.

This trend was officially acknowledged by the US Energy Information Administration in a January 5 bulletin titled: "Crude oil prices fell in 2025 amid oversupply."

Since the shale revolution of the 2010s, American oil and gas firms have focused on shareholder returns rather than major upstream investments. Persistently low prices give them little incentive to pour billions into a high-risk venture like Venezuela.

Weak global economic growth is partly to blame for falling oil prices, but a more permanent structural shift is underway. The rise of low-carbon technologies, especially electric vehicles (EVs), is steadily eroding demand for fossil fuels.

This transition is visible across major economies:

• Europe: Wind, solar, and battery storage are increasingly displacing natural gas for electricity generation.

• China: An explosive boom in EVs—including cars, buses, and trucks—is cutting into oil consumption in the world's second-largest market.

In China, the share of electric and hybrid vehicles in all new vehicle sales hit 50% between January and September 2025, a massive jump from just 6.5% during the same period in 2020. As a result, oil demand in China's transport sector has likely already peaked, with a peak in the country's overall oil demand expected to follow.

China may be a frontrunner, but EV adoption is accelerating globally. Cars are becoming more affordable, battery capacity is improving, and charging infrastructure is expanding, all of which reduces "range anxiety" for consumers. For policymakers in oil-importing nations, EVs offer a path to greater energy security by reducing reliance on foreign suppliers, volatile prices, and the US dollar.

As the electrification of transport—the single largest consumer of oil—dampens demand, global supply continues to rise with new production coming from Argentina, Brazil, Guyana, and the United States itself. This dynamic suggests prices are set to fall further, making large-scale investment in new oil projects a questionable bet.

The oil bonanza promised by President Trump has so far been met with a muted public response from America's energy majors. The president has even suggested that if profits fail to materialize, the government could reimburse corporate losses—a move that would amount to a massive public subsidy for some of the world's most profitable companies.

Whether this offer is enough to incentivize investment remains uncertain, especially given the political instability in both post-intervention Venezuela and the US.

However, other strategic motives may be at play:

• Energy Security: Many US refineries are designed to process heavy crude, like Venezuela's. Securing a new source would reduce dependence on Canadian tar sands.

• Market Influence: Controlling one of the world's largest oil reserves provides leverage over global prices, a classic energy strategy.

• Geopolitical Leverage: China is currently the primary buyer of Venezuelan oil and has companies operating there. US control would be a direct challenge to a key rival.

• Historical "Compensation": President Trump has framed the move as payback for past actions by the Venezuelan government, like the 1976 nationalization of its oil industry, which harmed American corporate interests.

Regardless of the motive, attempting to exploit Venezuela's oil reserves is a risky economic gambit. It is a bet that the global transition to electric vehicles will stall—a bet against the future of energy.

Despite being encircled by Israeli forces and facing threats of annihilation under a US peace plan, Hamas is methodically rebuilding its governance in the parts of Gaza it still holds. The defiant Islamist group is re-establishing a semblance of its pre-war authority, creating a direct challenge to international efforts to secure a lasting peace.

Surviving civil servants are returning to their posts, and tax collection has resumed—even from Palestinians now living in tents. Courts are reopening for those who can afford legal action, while Hamas functionaries, some of whom were recently fighting Israeli troops, now patrol street corners to maintain order.

This resurgence highlights Hamas's rejection of the disarmament mandated by President Donald Trump's peace proposal, which is currently stalled in a fragile ceasefire. While the group can no longer deploy the large force that invaded southern Israel on October 7, 2023, its remaining armed presence is enough to give any foreign intervention force serious pause.

"Hamas is taking advantage of delaying the second phase of Trump's plan by rebuilding its political and security control," says Mkhaimar Abusada, a political science professor from Gaza's Al-Azhar University, now at Northwestern University in Chicago.

For many Palestinians who remain in Gaza, Hamas's authority is the only system they have known for two decades. However, private conversations and social media posts reveal growing frustration with the group's increasingly firm methods.

Hamas claims it is simply trying to restore order amid the chaos of a two-year war, ongoing Israeli airstrikes, and humanitarian aid shortages. Since the ceasefire began on October 10, Israel has killed more than 400 Palestinians in strikes it says target Hamas attacks or military threats. In turn, Hamas has accused Israel of violating the truce, cracked down on rival militias, and held public shootings of individuals accused of looting or insurrection.

The group's control extends deep into daily life. A Hamas-formed "Petroleum Commission" has seized control over cooking gas, a critical resource for heating. Families now receive half-full cylinders in a stated effort to distribute limited supplies more widely. However, this nationalization of a previously private market has drawn criticism. Ahmed Shaldan, a restaurant owner, claims businesses like his are forced to pay high prices to "middlemen" to secure the gas needed to operate. The commission denies selling gas directly to restaurants.

In Gaza City's once-thriving Remal shopping district, vendors whose stores were destroyed have set up tents along main roads. The Hamas-run city hall is now demanding rent from them, classifying their makeshift stalls as municipal property.

One resident, Maisara Mohammed, posted a screenshot of a message from the Hamas-run Land Authority demanding two years of back-fees within a week. "This is after my house, my apartment and the building I had were destroyed," he wrote. Another vendor reported receiving a demand for 4,200 shekels ($1,320) for the last three months. "Our livelihoods are shattered," he said. "Why aren't they letting us make a living?"

The Land Authority later claimed the messages were a "software error."

Hamas is working to rebuild its internal structure. A spokesman confirmed that government departments have resumed operations with "flexible work plans based on crisis management."

Before the war, the group employed 50,000 Palestinians. That number has been reduced by a third due to casualties, detentions, and displacement. Still, the basic monthly wage of 800 shekels is a powerful incentive in a population heavily dependent on aid.

Militarily, Hamas has been severely weakened. The loss of senior commanders has crippled its armed wing, and Israel estimates its fighting force is now around 20,000—half its pre-war strength and bolstered by teenage recruits and field-promoted junior operatives.

Despite these losses, the organization remains defiant. "Hamas will never give up its arms as long as the occupation continues, and will never surrender even if it has to fight with its nails," a spokesman stated.

Three Hamas members confirmed the group is streamlining its command structure and selecting a replacement for its politburo head, Ismail Haniyeh, who was assassinated by Israel in Iran in 2024.

The core of the Trump plan hinges on the complete demilitarization of Gaza, a condition Israel insists upon. Hamas has indicated it might relinquish its remaining rockets and explosives but refuses to give up its small arms. The group also demands a full Israeli withdrawal from the territory.

Progress is further complicated by other issues, such as Hamas's failure to return the body of the last hostage from the October 7 attack, which it claims it cannot locate.

Under the current ceasefire, Israeli forces have redeployed to eastern Gaza. The peace plan calls for them to hand over control to an International Stabilization Force (ISF), which would facilitate a transition to non-Hamas Palestinian rule. However, Israel wants assurances the ISF will control the entire Gaza Strip. With contributing countries for the ISF yet to be decided and none likely willing to fight Hamas, the situation is heading toward a stalemate.

This deadlock could ultimately lead to a renewed Israeli offensive. As Professor Abusada noted, Hamas's actions are providing a rationale for continued Israeli presence. "Hamas will give Netanyahu the justification to delay Israeli withdrawal from Gaza," he said.

Yen recovered modestly during the Asian session as Japanese equities edged lower, but both moves lacked conviction. The pullback in the Nikkei 225 was mild, and the corresponding FX response suggests investors see little reason to reassess the broader trend.

Geopolitical developments are weighing on Japanese sentiment after China imposed export curbs on selected dual-use items destined for Japan. The measures cover goods and technologies with both civilian and military applications, including rare earths essential for chipmaking and drone production. The restrictions appear linked to comments by Prime Minister Sanae Takaichi last November on Taiwan. Beijing reacted strongly after Takaichi warned that a Chinese attack on the island could represent an existential threat to Japan, further straining already fragile ties.

Japan's dependence on China remains significant, with around 60% of rare-earth imports sourced from country. Still, the lack of clarity on which items are affected makes it difficult to gauge the real economic impact for now. Meanwhile, some observers argue the move may be largely symbolic. China has historically avoided actions that would severely disrupt Japanese industry, and the latest step may be intended to stir domestic criticism of Takaichi rather than materially damage bilateral trade.

In contrast, Australian Dollar stayed well bid after extending gains earlier in the day, even as inflation data surprised slightly to the downside. The softer CPI reduced pressure for an immediate February hike by the RBA, but did little to derail the broader tightening narrative. Even with the softer headline outcome today, disinflation in underlying pressures remains modest. That persistence keeps the door open for rate hikes later in the year, even if February proves too soon.

Markets currently price around a two-thirds chance of a February hold, with a hike expected by June and a strong probability of a second before year-end. Nevertheless, RBA policymakers are expected to place greater weight on the full Q4 inflation report later this month. A 0.9% quarter-on-quarter or higher rise in core inflation could still push the RBA toward tightening in February.

In FX performance terms this week so far, Aussie continues to lead, followed by Sterling and Yen. Loonie sits at the bottom, with Swiss Franc and Euro also under pressure. Dollar and Kiwi are trading d in the middle. Focus now shifts to US ADP jobs and ISM Services PMI later today, though the decisive catalyst is expected to be Friday's non-farm payrolls.

In Asia, Nikkei fell -1.06%. Hong Kong HSI is down -1.12%. China Shanghai SSE rose 0.05%. Singapore Strait Times is flat. Japan 10-year JGB yield fell -0.008 to 2.122. Overnight, DOW rose 0.99%. S&P 500 rose 0.62%. NASDAQ rose 0.65%. 10-year yield rose 0.014 to 4.179.

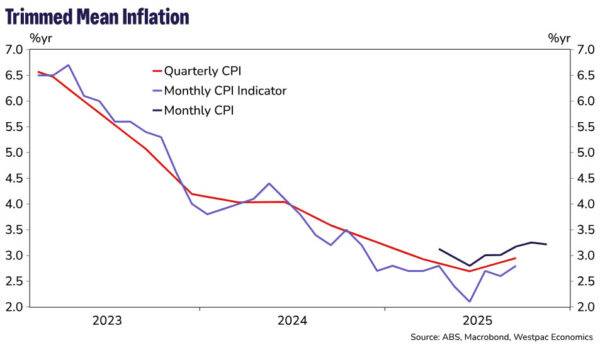

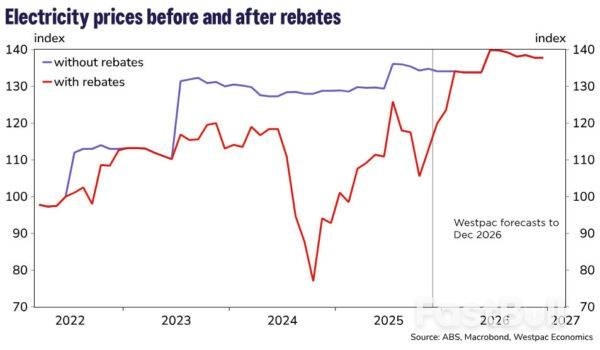

Australia's inflation cooled more than expected in November, offering some relief after months of intensifying price pressure. Headline CPI slowed from 3.8% yoy to 3.4%, undershooting expectations of 3.6%. Trimmed mean inflation eased modestly from 3.3% yoy to 3.2%, pointing to a gradual moderation in underlying pressures.

The slowdown was broad-based. Annual goods inflation fell to 3.3% yoy from 3.8%, driven largely by a sharp deceleration in electricity prices, which rose 19.7% over the year compared with 37.1% previously. Services inflation also eased, slowing to 3.6% yoy from 3.9%, helped by a pullback in domestic holiday travel costs after October's school-holiday and major sporting-event surge.

Despite the moderation, price pressures remain elevated in key areas. Housing inflation stayed firm at 5.2% yoy, while rents and medical services continued to rise at a solid pace. The data ease immediate pressure on the RBA for rate hike. But with inflation still well above target range, policymakers are likely to remain cautious about declaring victory too early.

Japan's service sector lost some momentum at the end of 2025, with Services PMI finalized at 51.6 in December, down from 53.2 in November. Composite PMI eased to 51.1 from 52.0, marking a seven-month low.

According to S&P Global Market Intelligence Economics Associate Director Annabel Fiddes, services firms reported slower growth in activity and new orders, while manufacturing showed relative improvement. Despite softer demand signals, business confidence across Japan's private sector remained firm, supporting a "solid and accelerated rise in employment".

Cost pressures, however, remain a key challenge. Input prices rose at the fastest pace since April, driven by higher costs, prompting firms to lift selling prices at a solid rate. With demand conditions softening slightly, companies face a "difficult balance" between passing on higher costs to protect margins and maintaining competitiveness.

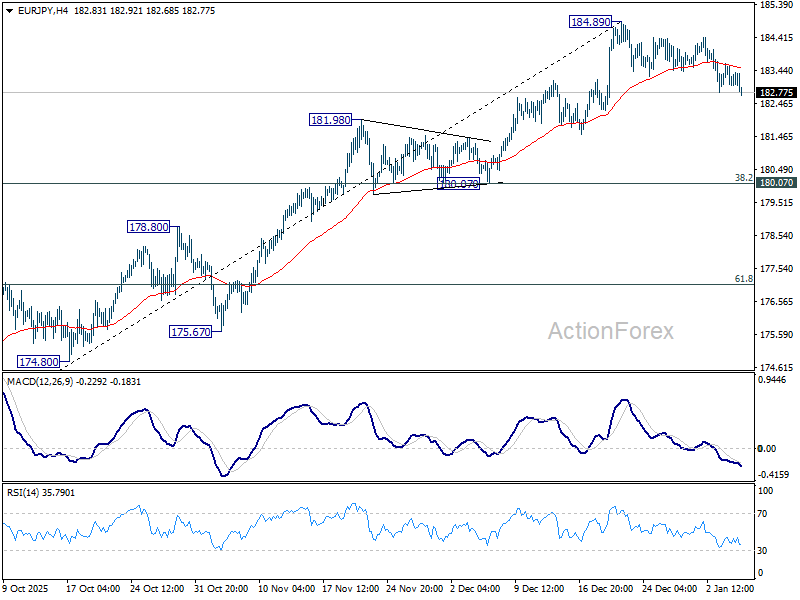

Daily Pivots: (S1) 182.87; (P) 183.26; (R1) 183.53;

EUR/JPY edges lower today and the sustained trading below 55 4H EMA (now at 183.45) argues that fall from 184.89 short term top is already correcting the rally from 172.24. Intraday bias is mildly on the downside for 55 D EMA (now at 180.74). But strong support should emerge from 180.07 cluster (38.2% retracement of 172.24 to 184.89 at 180.05) to bring rebound. ON the upside, firm break of 184.89 will resume larger up trend to 186.31 fibonacci level.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.16) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 100% projection at 205.81 next.

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Services PMI Dec F | 51.6 | 52.5 | 52.5 | |

| 00:30 | AUD | CPI M/M Nov | 0.00% | 0.10% | 0.00% | |

| 00:30 | AUD | CPI Y/Y Nov | 3.40% | 3.60% | 3.80% | |

| 00:30 | AUD | Trimmed Mean CPI M/M Nov | 0.30% | 0.20% | 0.30% | 0.40% |

| 00:30 | AUD | Trimmed Mean CPI Y/Y Nov | 3.20% | 3.30% | ||

| 00:30 | AUD | Building Permits M/M Nov | 20.20% | 2.10% | -6.40% | -6.10% |

| 07:00 | EUR | Germany Retail Sales M/M Nov | -0.60% | 0.20% | -0.30% | |

| 08:55 | EUR | Germany Unemployment Rate Nov | 6.30% | 6.30% | ||

| 08:55 | EUR | Germany Unemployment Change Nov | 5K | 1K | ||

| 09:30 | GBP | Construction PMI Dec | 42.4 | 39.4 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Dec P | 2.10% | 2.10% | ||

| 10:00 | EUR | Eurozone Core CPI Y/Y Dec P | 2.40% | 2.40% | ||

| 13:15 | USD | ADP Employment Change Dec | 50K | -32K | ||

| 15:00 | USD | ISM Services PMI Dec | 52.3 | 52.6 | ||

| 15:00 | USD | Factory Orders M/M Oct | -1.00% | 0.20% | ||

| 15:00 | CAD | Ivey PMI Dec | 49.5 | 48.4 | ||

| 15:30 | USD | Crude Oil Inventories (Jan 2) | -1.2M | -1.9M |

The British Pound remained supported for more gains against the US Dollar. GBP/USD climbed above 1.3450 to start another increase.

Looking at the 4-hour chart, the pair settled above 1.3450, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even spiked above 1.3550 before the bears appeared.

A high was formed at 1.3567, and the pair is now correcting some gains. On the downside, immediate support is near the 1.3490 level. The first major area for the bulls might be near 1.3450 and a bullish trend line.

The 100 simple moving average (red, 4-hour) is also near 1.3450. A close below 1.3450 might spark heavy bearish moves. The next support could be 1.3420, below which the bears might aim for a move toward 1.3350.

Immediate resistance sits near 1.3550. The first key hurdle is seen near 1.3565. A close above 1.3565 could open the doors for a move toward 1.3620. Any more gains could set the pace for a steady increase toward 1.3650.

Looking at XPR, the bulls took control and pushed the price above many key hurdles such as $2.20, $2.30, and $2.35.

Upcoming Key Economic Events:

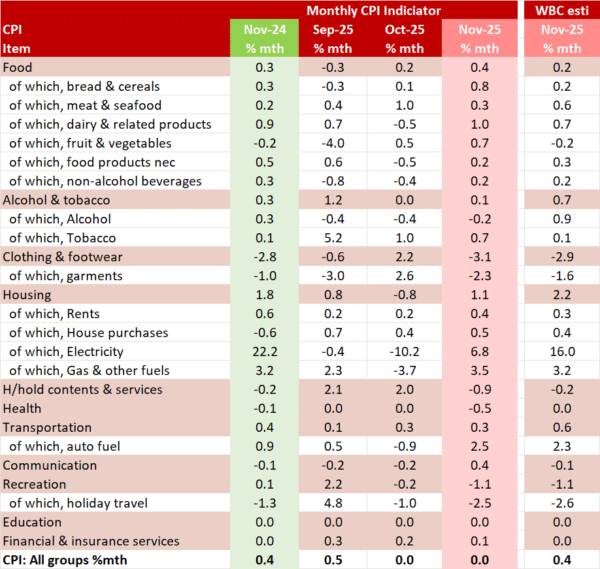

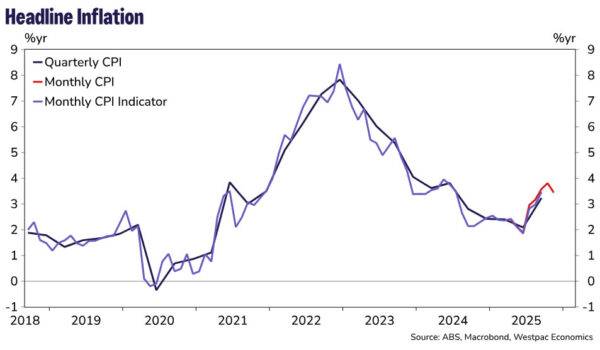

The new Complete Monthly CPI printed softer than we thought presenting downside risk to our December quarter estimates.

The new Complete Monthly CPI gained 3.4% in the year to November, softer than Westpac's estimate of 3.8%yr and the market estimate of 3.6%yr. At face value, this suggests downside risk to our December quarter estimates of 0.8%qtr for the Trimmed Mean (TM) and 0.6% for the CPI. However, we still need to complete a full review of the monthly data to confirm this.

November's headline figure was flat in the month, softer than Westpac's published near-cast of 0.4% on the back of a smaller than expected rise in electricity (6.8% vs 16.0% estimated), a larger than expected fall in household contents & services (–0.9% vs –0.2% estimated), clothing & footwear (–3.1% vs. –2.9% estimate) and health (–0.5% vs. 0.0% expected), a smaller than expected rise in transport (0.3% vs. 0.6% forecast) to be partially offset by stronger gains in food (0.4% vs 0.2% estimated), rents (0.4% vs 0.3% estimated), dwellings (0.5% vs 0.4% estimated) and communication (0.4% vs. –0.1% estimated).

As has been the norm for some time, the energy rebates continue to have a significant impact on estimates of consumer price inflation. Electricity costs rose 19.7% in the year to November, held down by households using the Queensland State Government electricity rebate . This is a moderation from the 37.1%yr pace in October 2025 reflecting, as the ABS noted, that more households received catch-up payments of the Commonwealth Energy Bill Relief Fund (EBRF) rebate in 2024 compared to 2025.

The ABS estimates that excluding the impact of the Commonwealth and State Government electricity rebates over the past year, electricity prices rose 4.6% in the year to November compared to a 5.0% increase in the year to October. This reflects annual price reviews from energy retailers in July 2025.

The TM measure was reported to have increased 3.2% in the year to November, a slight moderation from the 3.3%yr pace in October. Due to its short history, the annual pace of monthly TM inflation can only be calculated back to April 2025. Before then the ABS noted that annual movements are calculated by comparing each quarter to the same quarter in the previous year.

The TM lifted 0.3% in the month of November, the same monthly increase it has seen for the previous four months and down from the 0.5%mth increase in July but stronger than the 0.2%mth prints from March to June.

While we note that the current annual pace of the Monthly TM, at 3.2%yr, matches our current December quarter TM estimate of 3.2%yr, we do know that the RBA will, at least for the near term, remain focused on the quarterly TM, rather than the Monthly TM. This is because the ABS does not have enough history to complete a full seasonal adjustment process for all the components of the Monthly CPI. The ABS has also noted it will take at least 18 months to gather that data so it is likely to be a year and a half before we will be able to make a more detailed assessment of core inflation directly via the monthly TM. As such, we anticipate the RBA will use the December print to guide their decision. Our expectation is that the Monetary Policy will remain cautious and pause at its next meeting in February and remain on hold for the remainder of the year.

As we have noted, see our November CPI preview, while some series did have a longer monthly history coming from the previously published monthly CPI indicator and the ABS can potentially use historical seasonal analysis we caution that some of the new data sets have a different history to the old data and as such, we expect it is going to take some time to understand the seasonal behaviour of the new data.

From the US, ISM Services index and ADP private sector employment report are due for release for December, and the JOLTs report for November. ADP's weekly employment estimates signalled improving jobs growth momentum towards late November and early December.

In the euro area, we expect HICP inflation to decline to 1.9% y/y in December from 2.1% y/y in November with a risk that it could round down to 1.8% y/y. We expect core inflation at 2.3% y/y. Hence, the December inflation should be seen as a dovish surprise, although sticky services inflation somewhat limits how dovishly it should be interpreted.

In Sweden, services PMI for December are released today. The November service PMI outcome for Sweden was the highest since summer 2022 and significantly stronger than the outcomes in both Europe and the US. Given that we have seen a decline in most countries for the December outcome, it would not be surprising if we also see some pullback in today's December release for Sweden.

What happened overnight

China imposed a ban on the export of dual-use items to Japan for military use, escalating a diplomatic dispute over Japanese Prime Minister Takaichi's recent remarks on Taiwan. Japan has called the measure "absolutely unacceptable," as the ban includes rare earth elements critical for manufacturing. Beijing is reportedly considering broader rare earth curbs, which could significantly impact Japan's economy and key industries like automotives. Market reaction has been muted so far, though Japanese shares fell on Wednesday, led by declines in mining stocks.

Overnight, US President Trump once again rekindled his ambition to acquire Greenland, citing national security priorities in the Arctic region and the island's untapped mineral resources. While the White House stated that purchasing Greenland is being discussed, it also explicitly stated that military action to acquire it is an option. That said, WSJ also reported that Secretary of State Marco Rubio had downplayed the threats as a negotiation tactic in a recent internal briefing. European leaders and US lawmakers have expressed strong opposition, stressing respect for Denmark's sovereignty and NATO obligations, but the administration insists the goal "is not going away".

What happened yesterday

In Germany, December inflation came in weaker than expected, with HICP inflation falling to 2.0% y/y (cons: 2.2%, prior: 2.6%) and CPI inflation declining to 1.8% y/y (cons: 2.1% y/y, prior: 2.3% y/y). The surprise was driven by sharp declines in goods and food prices, while energy prices fell as anticipated. However, services inflation remained very sticky at 3.5% y/y, limiting the dovish interpretation of the weaker headline figures.

In France, HICP inflation fell to 0.7% y/y in December from 0.8% y/y in November, as expected. The decline was driven by lower energy prices, while food inflation rose and services inflation held steady at 2.2% y/y. These prints point to lower than initially expected euro area headline inflation today, which we now expect to decline to 1.9% y/y.

In the US, Federal Reserve Governor Stephen Miran argued for aggressive interest rate cuts in 2026, calling for over 100 basis points of reductions to support economic growth. Miran stated that policy remains overly restrictive despite inflation being close to the Fed's 2% target and warned that failing to lower rates could hinder robust growth expectations for the year. His term as a Fed governor ends on 31 January, and he is serving at the Fed while on leave from his role as a top economic adviser to President Trump.

In geopolitics, Venezuelan opposition leader Maria Corina Machado praised US President Trump for the capture of Nicolas Maduro and expressed confidence that her movement would win a free election. Machado escaped Venezuela in October and received the Nobel Peace Prize and now vows to return as soon as possible. However, Trump appears to be working with interim President Delcy Rodriguez, a Maduro ally, to stabilise Venezuela before an election, disappointing the opposition. International backlash against the US intervention continues, with concerns over the precedent it sets for global norms. Overnight, Trump announced plans to refine and sell up to 50 million barrels of sanctioned Venezuelan oil, with revenues controlled by the US administration to allegedly benefit both Venezuelans and Americans

In the euro area, final December services PMI was revised slightly down to 52.4 from the flash estimate of 52.6, while the composite PMI fell to 51.5 from 51.9 due to the manufacturing print being revised down. Despite the downward revisions, the euro area economy ended the year on a positive footing, with the Q4 average composite PMI significantly higher than in Q3, indicating decent growth and supporting the ECB's assessment of the economy being in a "good place".

In Norway, house prices (SA) were unchanged in December, falling short of Norges Bank's December MPR estimate of +0.8%. While this is unlikely to affect monetary policy in the short term, the data could support lower rate expectations in the market.

Equities: Global equities extended gains yesterday, marking the third consecutive positive trading day to start 2026. In Europe, the advance was more defensively led, with healthcare outperforming. Oil prices reversed lower after a brief uptick, weighing on energy stocks, which underperformed on the day.

More importantly, the first three trading days of the year have been characterised by a broadening of the equity rally. Performance has rotated away from some last year's winners (not least tech) and towards more classic deep cyclical sectors. Likewise small caps have outperformed large caps for three days in a row, reinforcing the message of broader participation. Putting this into perspective: since our last tactical shift in mid-December, the materials sector is up 8.2%, while global technology is down 1.7%.

Part of this reflects the exceptional strength in both industrial and precious metals, but the broader takeaway remains clear. Global equities are up 2.2% over the same period, despite technology underperforming. In other words, equities can rise even when tech does not lead! In the US yesterday, Dow +1.0%, S&P 500 +0.6%, Nasdaq +0.7%, and Russell 2000 +1.4%. This morning, Asian markets are mixed, and futures in both Europe and the US point to a more cautious open.

FI and FX: The USD outperformed most of the rest of the G10 currency space yesterday closely followed by the Scandies on another day marked by positive sentiment in the stock market. The bond market was overall steady with US yields inching higher and European yields lower. The DKK market came under pressure. The culprit was a rise in EUR/DKK close to past central bank FX intervention levels, which led widening of the spread between Danish and German government bonds.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up