- USDJPY

- XAUUSD

- XAGUSD

- WTI

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

ECB's complex outlook: cooling inflation vs. resilient growth, sparking debate on 2026 rate hikes or cuts.

The European Central Bank is set to meet on February 5, 2026, and while no one expects a change in interest rates, the event is shaping up to be a pivotal moment for the euro. With EUR/USD trading below the key 1.20 level, all eyes will be on President Christine Lagarde's press conference for clues about the ECB's next major policy decision.

As cooling inflation and a strengthening currency cloud the outlook, policymakers and markets are divided. The central question is whether the ECB’s next move later in the year will be a rate hike or a rate cut. The answer will likely depend on the central bank's interpretation of an increasingly complex economic picture.

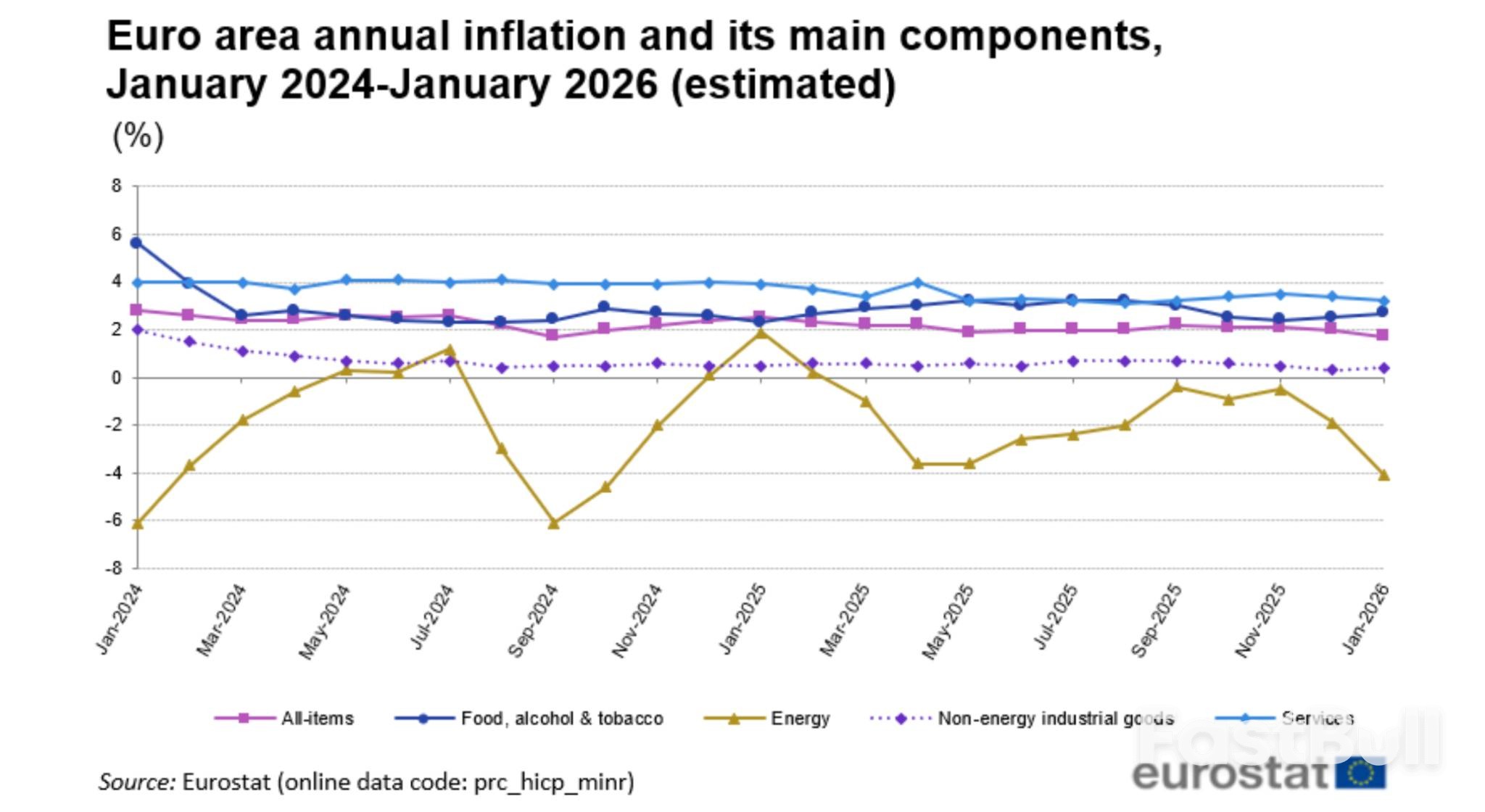

At its final meeting of 2025, the ECB presented a confident view of the eurozone economy. The central bank upgraded its growth forecasts, projecting 1.4% growth for 2025, followed by 1.2% in 2026, and a return to 1.4% in 2027 and 2028.

On the inflation front, the ECB's December projections showed prices normalizing around its 2% target. The forecast anticipated inflation averaging 2.1% in 2025, falling to 1.9% in 2026, and eventually settling at 2% by 2028. This outlook suggested that interest rates could remain unchanged throughout 2026, with the ECB describing its policy as being in a "good place."

However, recent data has complicated this narrative. January figures from Eurostat showed headline inflation in the euro area slowed to 1.7%, its lowest level since September 2024. More significantly, core inflation, which strips out volatile items, unexpectedly fell to 2.2% from 2.3%. This trend has fueled debate over whether disinflationary pressures are stronger than anticipated.

Two factors are at the center of this concern:

1. A Stronger Euro: The euro's recent appreciation against the dollar makes imports cheaper, dampening inflation.

2. Chinese Imports: An influx of lower-priced goods from China is putting downward pressure on prices across European markets.

ECB Governing Council member Gediminas Simkus recently noted the bank's success in bringing inflation back to target despite global challenges. Still, he warned that ongoing political instability remains a significant risk that could easily disrupt the ECB's current policy balance.

For the upcoming meeting, the market consensus is clear: the ECB will hold its key interest rates steady for the fifth consecutive time. The deposit facility rate is expected to remain at 2.00%, the main refinancing operations rate at 2.25%, and the marginal lending facility rate at 2.40%.

But beneath this surface-level agreement, a fierce debate is brewing over the direction of the next policy shift.

The Case for a Future Rate Hike

Despite inflation running below target, some ECB officials have not ruled out the possibility of raising rates later in 2026. This hawkish stance is driven by several considerations:

• Resilient Growth: The ECB's own upgraded growth forecasts suggest the eurozone economy could be more robust than expected. Sustained growth could generate fresh price pressures as economic capacity tightens.

• Sticky Inflation Risks: Some policymakers worry that the current 2% deposit rate may not be restrictive enough if inflation proves stubborn, especially with rising wage growth or a continued surge in energy prices. Oil and European natural gas prices have both climbed since the start of the year.

• Official Commentary: Recent remarks from key officials, including board member Isabel Schnabel, chief economist Philip Lane, and President Lagarde herself, have been interpreted by markets as keeping the option of a late-2026 hike alive.

The Argument for a Future Rate Cut

On the other side, a growing number of economists believe the ECB's next move is more likely to be a rate cut, potentially restarting the easing cycle paused in June 2025. The arguments for this dovish view include:

• Disinflationary Trend: With headline inflation at 1.7% and core inflation falling, both metrics are trending away from the ECB's 2% goal. If this continues, holding rates steady could become overly restrictive.

• Euro Appreciation: A stronger euro effectively tightens financial conditions by making imports cheaper. The ECB might need to offset this with lower interest rates if the currency continues to climb.

• Structural Pressures: The flood of competitively priced Chinese goods into Europe represents a persistent disinflationary force that could keep a lid on prices.

• Economic Fragility: Pockets of weakness remain in the eurozone, particularly in Germany's manufacturing sector, which is grappling with weak global demand and high energy costs.

The reality is that policymakers are genuinely split, with some officials stating that a hike and a cut are equally plausible outcomes depending on incoming data. This uncertainty reflects the unique position the ECB is in—having achieved its inflation target but now facing significant risks in both directions.

Diego Iscaro, head of European economics at S&P Global Market Intelligence, summarized the middle ground: "With underlying inflation still a little too high for comfort and expectations that the eurozone economy will regain momentum later in the year, we believe the most likely outcome is that the ECB will keep rates unchanged for the foreseeable future."

ECB chief economist Philip Lane articulated this balanced strategy in mid-January. He noted that the central bank will not debate a rate change in the near term if the economy stays on its projected course. However, he cautioned that new shocks could upset the outlook.

This statement perfectly captures the ECB's current posture: maintain the status quo for now, but stand ready to act decisively if economic conditions change.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up