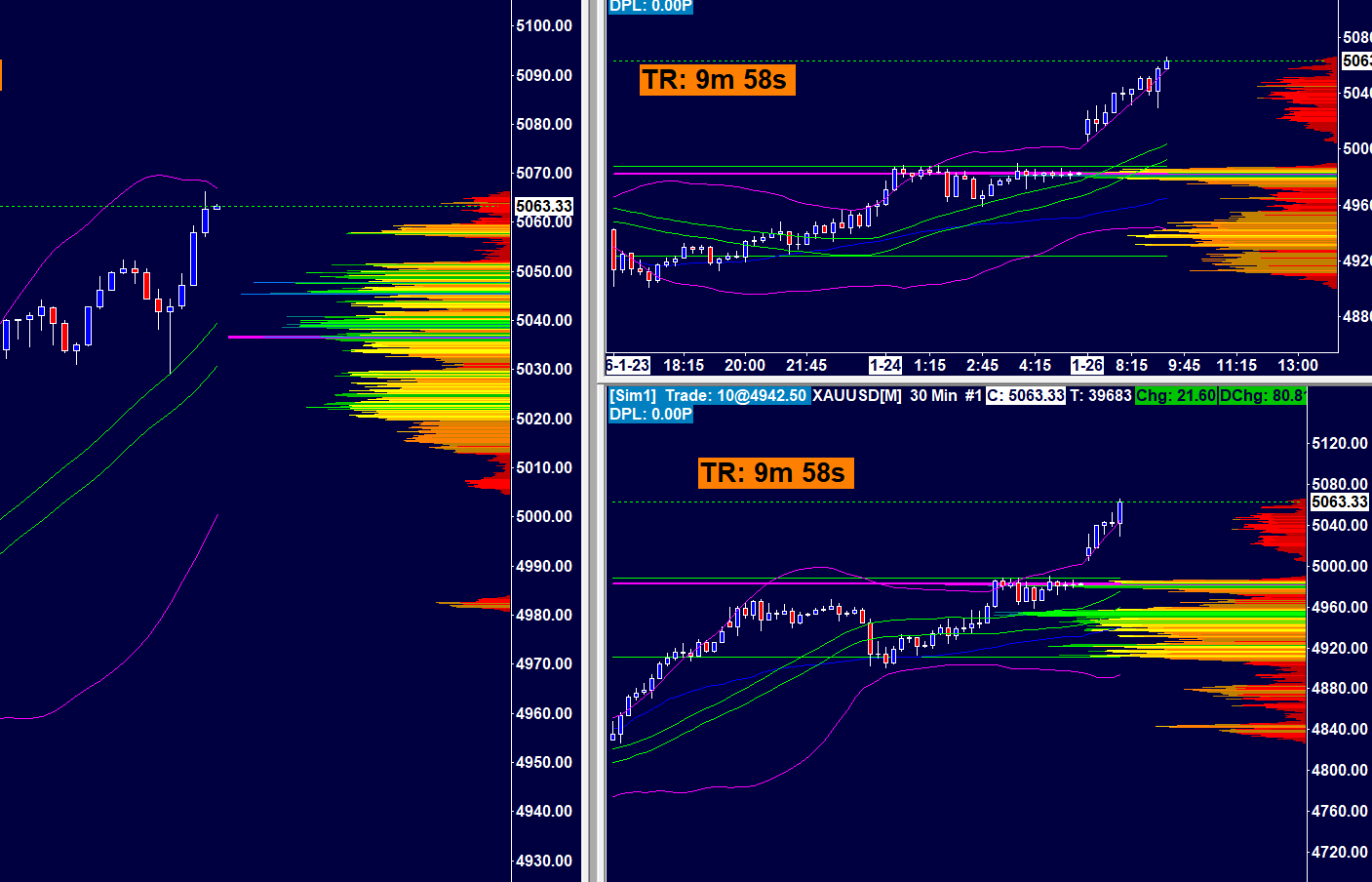

Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Canada halts China FTA talks, bowing to a US tariff threat and recalibrating its global trade strategy.

Canadian Prime Minister Mark Carney has officially halted plans for a comprehensive free trade agreement (FTA) with China, a major strategic shift in North American trade policy. The move comes in direct response to a threat from former U.S. President Donald Trump to levy 100% tariffs on Canadian exports if Ottawa moved forward with the Beijing negotiations.

The announcement, first reported by Solidintel, signals a critical turning point for Canada’s economic and foreign policy, forcing the nation to prioritize its relationship with the United States over deeper ties with China.

The Carney administration has suspended all formal discussions on an FTA with China, reversing years of exploratory talks. The government’s new focus is on strengthening existing trade partnerships, citing the paramount need to maintain stable economic relations within North America. This strategic retreat also reflects the broader geopolitical realignments reshaping global trade.

While Canada's bilateral trade with China previously reached about $100 billion annually, several persistent challenges have prevented deeper economic integration:

• Security Risks: Concerns over cybersecurity and the protection of intellectual property have remained a major hurdle.

• Human Rights: Ongoing diplomatic disagreements have strained the relationship.

• Supply Chain Vulnerabilities: The pandemic exposed the risks of over-reliance on single sources for critical goods.

• U.S. Relations: Preserving privileged access to the massive American market remains Canada's top economic priority.

Former President Donald Trump’s warning, delivered via Truth Social, fundamentally changed the Canadian government's calculations. His threat to impose 100% tariffs on Canadian goods promised severe economic consequences, prompting urgent impact assessments in Ottawa.

The potential damage would be catastrophic for Canada’s export-driven economy, with key sectors facing complete disruption. Projections indicated devastating impacts:

• Automotive: The $50 billion export market to the U.S. would face total collapse.

• Agriculture: A potential wave of farm bankruptcies could hit the $30 billion sector.

• Energy: The $80 billion energy export industry would likely see pipeline projects canceled.

• Manufacturing: The $40 billion sector would face the risk of massive job losses.

Trade experts agree that Canada was caught in an exceptionally difficult position. Dr. Sarah Chen, Director of the North American Trade Institute, described the situation as a "classic geopolitical trilemma." She explained that Canada cannot simultaneously maintain full sovereignty, pursue an independent trade deal with China, and preserve its privileged market access to the United States.

This dilemma is not new. The previous Trudeau administration had also explored diversifying trade toward China, particularly after difficult USMCA renegotiations. However, shifting global dynamics and consistent pressure from the U.S. under both the Biden and Trump administrations have made that strategy increasingly unfeasible. Trump's explicit ultimatum simply forced the issue to a head.

In response, the Carney government is rolling out a multi-pronged alternative strategy designed to build domestic resilience and diversify its trade partnerships beyond both the U.S. and China.

The new approach focuses on several parallel initiatives:

• CPTPP Enhancement: Deepening trade ties with partners in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership.

• EU-Canada CETA: Expanding the existing comprehensive economic agreement with the European Union.

• UK-Canada FTA: Finalizing a post-Brexit trade deal with the United Kingdom.

• ASEAN Engagement: Building stronger economic connections with Southeast Asian nations.

• Domestic Innovation: Investing in Canada's technological sovereignty to reduce external dependencies.

This diversified strategy aims to mitigate the risks of dependency on any single market while aligning Canada with broader Western economic security goals.

Beijing has reacted to Canada's decision with measured disappointment. Chinese officials have reiterated their interest in comprehensive trade deals but acknowledged the geopolitical realities complicating the negotiations. For now, existing trade between the two countries will continue under current frameworks.

The Canada-China relationship is now entering a new phase of pragmatic, but limited, engagement. Cooperation is expected to continue in areas of mutual interest, such as:

• Climate change and green technology

• Educational and research collaborations

• Limited agricultural and resource trade

• Coordination in multilateral forums

However, the prospect of comprehensive economic integration is officially off the table, highlighting the complex challenges middle powers face while navigating great power competition in 2025.

What was Carney's announcement on the China FTA?

Prime Minister Carney confirmed that Canada has suspended plans for a comprehensive free trade agreement with China. This decision was a direct result of former President Trump's threat to impose 100% tariffs on Canadian goods if the deal proceeded.

How severe would Trump's proposed tariffs be?

The proposed 100% tariffs would devastate key Canadian industries, including the automotive, agriculture, energy, and manufacturing sectors. Economic models predicted a potential GDP contraction of 3-5% and widespread job losses.

Is Canada-China trade ending completely?

No. Existing trade will continue under current agreements and frameworks. The decision specifically cancels negotiations for a new, comprehensive FTA that would have significantly deepened economic integration.

What is Canada's new trade strategy?

Canada is now focused on diversifying its trade relationships. This includes strengthening existing deals like CETA (with the EU) and the CPTPP, finalizing a new agreement with the UK, engaging more with ASEAN countries, and boosting domestic innovation.

Could Canada restart FTA talks with China later?

While possible, experts believe that structural geopolitical factors make a comprehensive trade deal with China unlikely for Canada in the medium term, regardless of who is in office in the United States.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up