Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

EUR/USD is attempting a recovery wave from the 1.1500 zone. USD/CHF climbed higher above 0.8050 and might correct some gains.

EUR/USD is attempting a recovery wave from the 1.1500 zone. USD/CHF climbed higher above 0.8050 and might correct some gains.

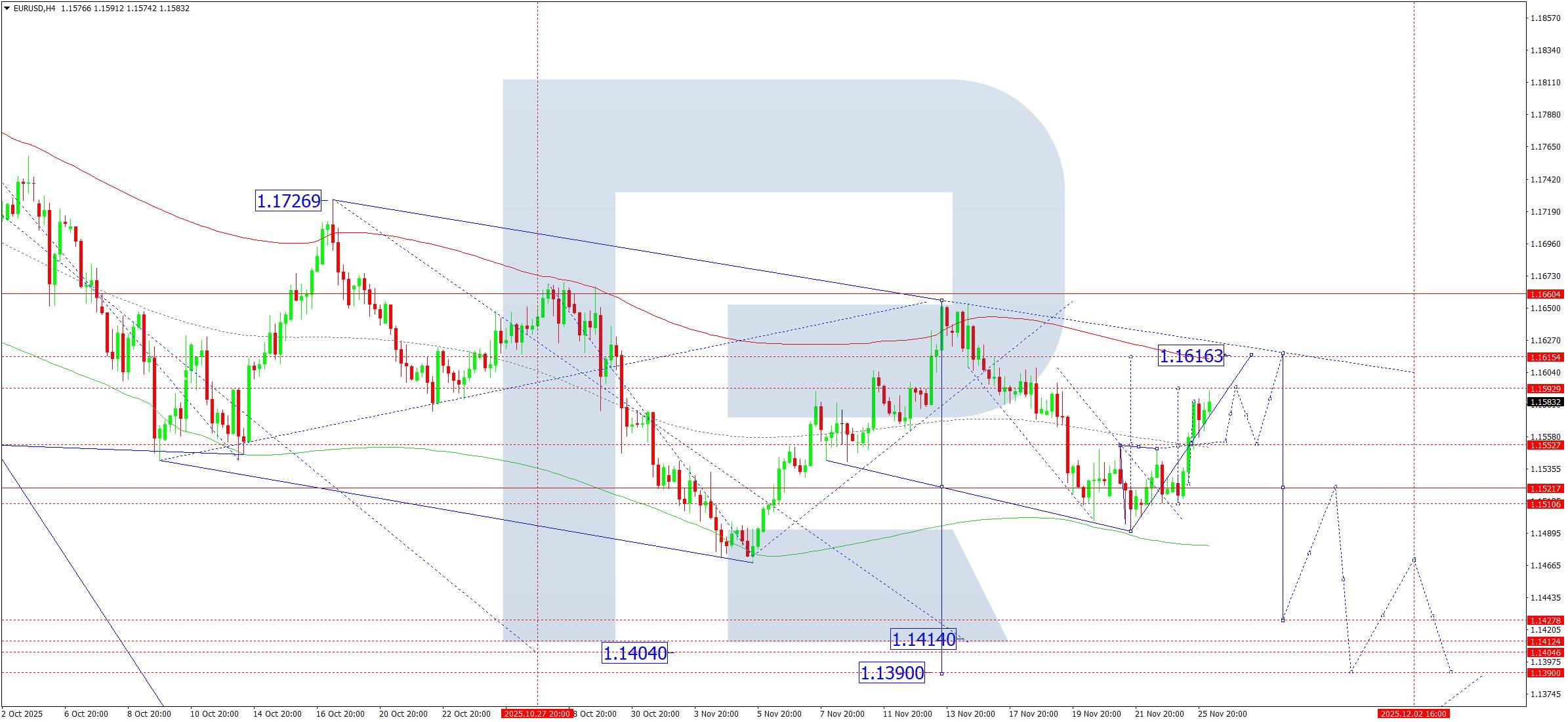

On the hourly chart of EUR/USD at FXOpen, the pair extended the decline below 1.1550. The Euro even declined below 1.1520 before the bulls appeared against the US Dollar.

The pair tested 1.1490 and recently started a recovery wave. There was a move above 1.1520 and 1.1550. The pair climbed above the 50% Fib retracement level of the downward move from the 1.1653 swing high to the 1.1491 low.

More importantly, there was a break above a major bearish trend line with resistance at 1.1530. The pair is now trading above 1.1575 and the 50-hour simple moving average. Immediate hurdle on the EUR/USD chart is near the 61.8% Fib retracement at 1.1590.

The first key breakout zone sits at 1.1615. An upside break above 1.1615 might send the pair toward 1.1655. Any more gains might open the doors for a move toward the 1.1700 zone. If there is a fresh decline, the pair might find bids near 1.1550.

The next major support is 1.1540. A downside break below 1.1540 could send the pair toward 1.1510. Any more losses might send the pair to 1.1490.

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from 0.7940. The US Dollar climbed above the 0.8000 handle against the Swiss Franc.

The bulls were able to pump the pair above the 50-hour simple moving average and 0.8050. Finally, the pair tested 0.8100. A high was formed near 0.8101 and the pair is now consolidating gains. The pair dipped below the 23.6% Fib retracement level of the upward move from the 0.7937 swing low to the 0.8101 high.

Besides, there was a break below a bullish trend line at 0.8085. On the downside, immediate support on the USD/CHF chart is near 0.8040. The first key area of interest might be near the 50% Fib retracement at 0.8020.

A downside break below 0.8020 might call for a drop to 0.7975. Any more losses may possibly open the doors for a move toward 0.7940.

On the upside, the pair could struggle near 0.8080. The first major barrier for bulls is 0.8100. If there is a clear break above 0.8100 and the RSI climbs above 50, the pair could start another increase. In the stated case, it could test 0.8150.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up