Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Crypto's sharp pullback isn't just about digital assets - it's signalling a wider shift in global risk appetite. Here's what the move really tells us about markets today.

In a matter of weeks, crypto has swung from new highs and headlines about institutional adoption to renewed talk of a "crypto winter". Bitcoin has given back a meaningful part of its recent rally, with ethereum falling even further in percentage terms. The entire crypto market has dropped sharply, and many listed crypto-related equities have followed.

For investors, the key question is no longer just why crypto is down, but what this move reveals about risk appetite. Crypto is increasingly behaving less like a niche asset and more like a high-beta gauge of global liquidity and market mood.

A useful way to view today's market is to treat crypto as a liquidity canary.

Crypto trades around the clock, reacts faster than most asset classes, and attracts both retail and institutional capital. That makes it highly sensitive to shifts in financial conditions. When liquidity is plentiful, capital flows in quickly. When it tightens, crypto is often the first place where it shows.

Over recent years, bitcoin's correlation with high-growth tech stocks has strengthened. At the same time, crypto typically struggles when the US dollar strengthens or when real yields rise – two classic risk-off signals in global markets. In practice, moves in bitcoin now say as much about macro conditions as they do about crypto itself.

For multi-asset investors, watching crypto levels has therefore become a way to gauge broader risk appetite in real time, rather than treating it as an isolated market.

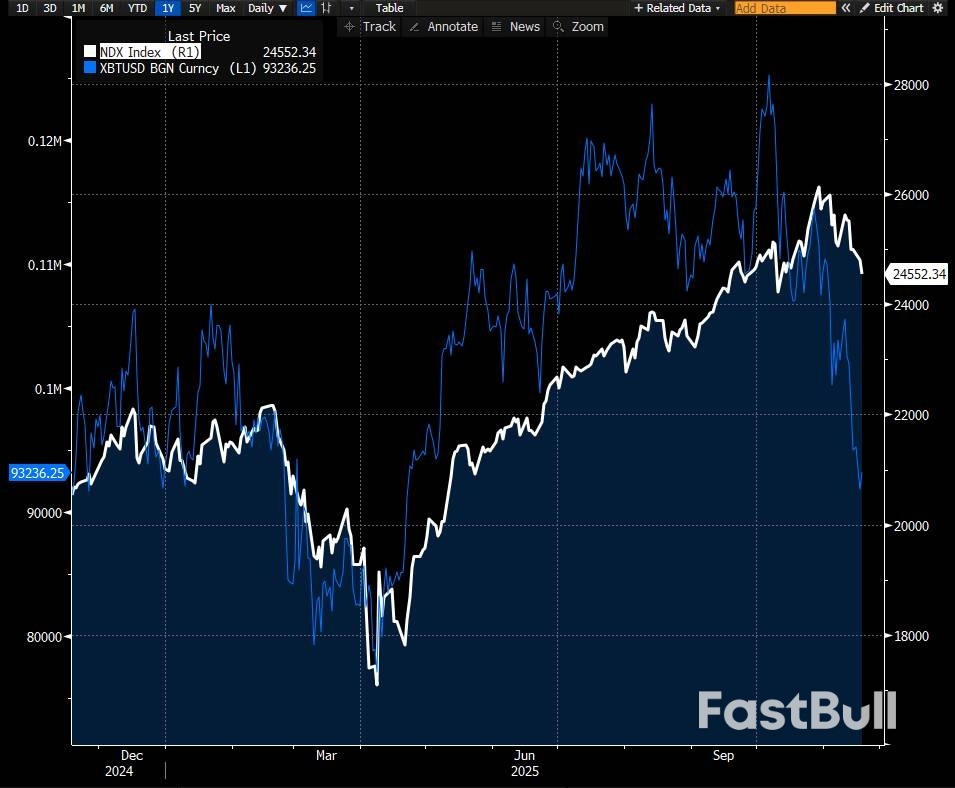

Bitcoin and the Nasdaq 100 have moved broadly in step over the past year, with crypto amplifying equity swings. Source: Bloomberg, Saxo.

Bitcoin and the Nasdaq 100 have moved broadly in step over the past year, with crypto amplifying equity swings. Source: Bloomberg, Saxo.The current sell-off is closely tied to a shift in the macro backdrop.

Markets have dialled back expectations for rapid interest-rate cuts, and real yields – nominal yields adjusted for inflation – have moved higher. For assets with no cash flows, such as bitcoin and ethereum, a higher real cost of capital is a clear headwind.

At the same time, high-growth technology and AI-linked stocks have also pulled back, and overall positioning in risk assets has become more cautious. Crypto, sitting at the high-beta end of that spectrum, naturally reacts more sharply.

Market structure amplifies the move. Crypto markets remain heavily influenced by leverage. When widely watched price levels break, forced liquidations can accelerate selling, especially when liquidity is thin. Earlier inflows into crypto vehicles have also softened, removing one of the tailwinds that supported prices earlier in the year.

Price is only part of the story. Volatility is offering its own signal.

Implied volatility on bitcoin and ethereum has risen meaningfully as the sell-off unfolded. Typically, this comes with two features:

Even for investors who never trade derivatives, these shifts are informative. Rising crypto volatility alongside rising equity or credit volatility often points to a broader risk-off environment. When volatility rises sharply in crypto but remains contained elsewhere, stress may be more localised.

The message is simple: volatility has become an asset class of its own, and it can reveal changes in sentiment earlier than price alone.

How this fits into previous crypto cycles

Viewed over a longer horizon, the current pullback fits a familiar pattern.

Previous crypto cycles have tended to feature strong rallies followed by sharp interim corrections – sometimes 20–40% – before either resuming the uptrend or shifting into a deeper downturn once liquidity fades. Large swings are a structural feature of the asset class.

The current cycle has new characteristics: regulated investment products, greater institutional participation and a more developed derivatives market. The macro backdrop is also different, with higher inflation and higher real yields than in earlier cycles.

Yet two themes remain constant:

Ethereum often experiences larger percentage swings than bitcoin, highlighting the higher risk profile of non-bitcoin exposures.

What this means for investors

This article does not attempt to forecast where bitcoin or ethereum will trade next. The more helpful question is simpler:Is this a moment for panic or euphoria?And the honest answer: neither.

Instead, the latest move offers a clearer framework for thinking:

In short: this is not a moment to panic or to celebrate.It's a moment to think, stay aware of the backdrop, and keep crypto in context – as one piece of a much larger risk picture.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Price Technical Outlook: $4000/oz Holds Firm As FOMC Minutes And Labor Data Releases Lie Ahead_1")

Price Technical Outlook: $4000/oz Holds Firm As FOMC Minutes And Labor Data Releases Lie Ahead_2")

Price Technical Outlook: $4000/oz Holds Firm As FOMC Minutes And Labor Data Releases Lie Ahead_3")