- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The U.S. Treasury intervened to buoy the yen amid global bond turmoil, offering brief calm as deeper economic pressures persist.

On Friday, the U.S. Treasury took a decisive step to halt the Japanese yen's sharp decline against the dollar. Treasury Secretary Scott Bessent initiated a "rate check," a clear signal that the U.S. government is preparing to intervene in currency markets.

The move came as turmoil in the Japanese bond market began to affect U.S. Treasury yields. Acting as the Treasury's agent, the New York Fed contacted its primary dealers to ask what exchange rates they could offer if it were to begin purchasing yen.

The market reacted instantly. The signal of potential intervention caused the U.S. dollar to fall sharply against the yen. The exchange rate, which had hit 159.2 yen per dollar, reversed course, strengthening the yen to 155.7 by Friday evening.

The yen's weakness was rooted in Japan's domestic bond market, which experienced a meltdown earlier in the week. The trigger was Prime Minister Sanae Takaichi's call for increased government spending combined with tax cuts.

This announcement spooked investors, leading to a rapid sell-off in Japanese Government Bonds (JGBs).

• The 30-year JGB yield spiked by 42 basis points in just two days, reaching 3.91%—its highest level since its introduction in 1999.

• The key 10-year JGB yield surged by 15 basis points over the same period.

This instability in Japan quickly spilled over into U.S. markets. On Wednesday, Bessent directly blamed the Japanese bond crisis for the surge in long-term U.S. Treasury yields.

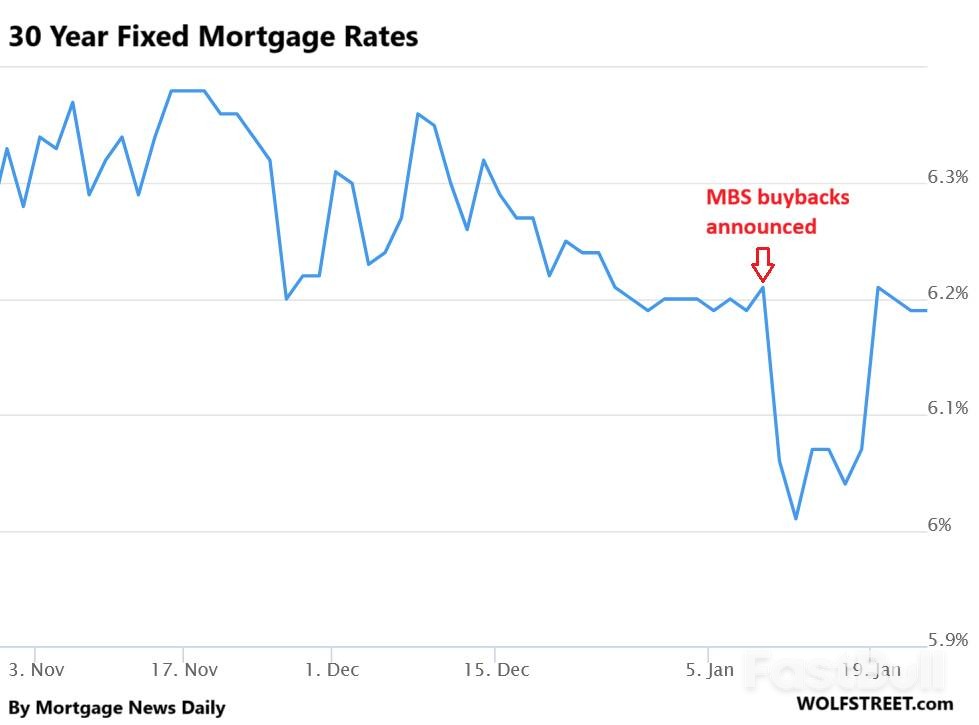

The 10-year U.S. Treasury yield had climbed to 4.30% by Wednesday morning, an increase of 17 basis points in a week. This rise complicated the Trump administration's efforts to lower mortgage rates, which typically track the 10-year yield.

As a result, 30-year fixed mortgage rates, which had recently fallen, jumped back to 6.20% from 6.01%, according to Mortgage News Daily.

Bessent addressed the issue on Fox News, stating, "It's very difficult to disaggregate the market reaction from what's going on endogenously in Japan." He noted that he had contacted Japanese officials and was confident they would take steps to calm their markets.

This jawboning, combined with Friday's "rate check," successfully pushed the 10-year U.S. Treasury yield down from its peak of 4.30% to 4.23%.

Separately, the administration has been trying to directly influence mortgage rates. In a move that began in 2025, government-sponsored enterprises Fannie Mae and Freddie Mac started buying back mortgage-backed securities (MBS) they had issued.

On January 8, President Trump directed them to buy back $200 billion in MBS, the maximum allowed under current law. However, the plan faced a practical hurdle: Fannie and Freddie lack the available cash for such a large purchase and would likely need to issue new bonds, which could add more pressure to the bond market.

Despite this, the announcement provided a temporary boost. Mortgage rates plunged by a combined 20 basis points on January 9 and 12. The effect was fleeting. By January 20, rates had returned to their January 8 levels, completing a U-shaped pattern on the chart.

While Bessent pointed to Japan, his jawboning conveniently sidesteps pressing domestic issues that are weighing on the bond market. The ballooning U.S. deficit requires a constant flood of new bonds that investors must absorb. At the same time, inflation continues to accelerate, worrying investors who see it eroding the purchasing power of their bond holdings.

Bond yields are meant to compensate investors for this loss of purchasing power, but current long-term yields appear too low to cover the risk of hotter inflation ahead. Government policies of high deficit spending, coupled with pressure on the Fed to cut short-term interest rates, are creating an environment where inflation can thrive.

For now, the bond market remains surprisingly calm despite these ripples. But market confidence built on official statements rather than economic fundamentals may not last long.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up