Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

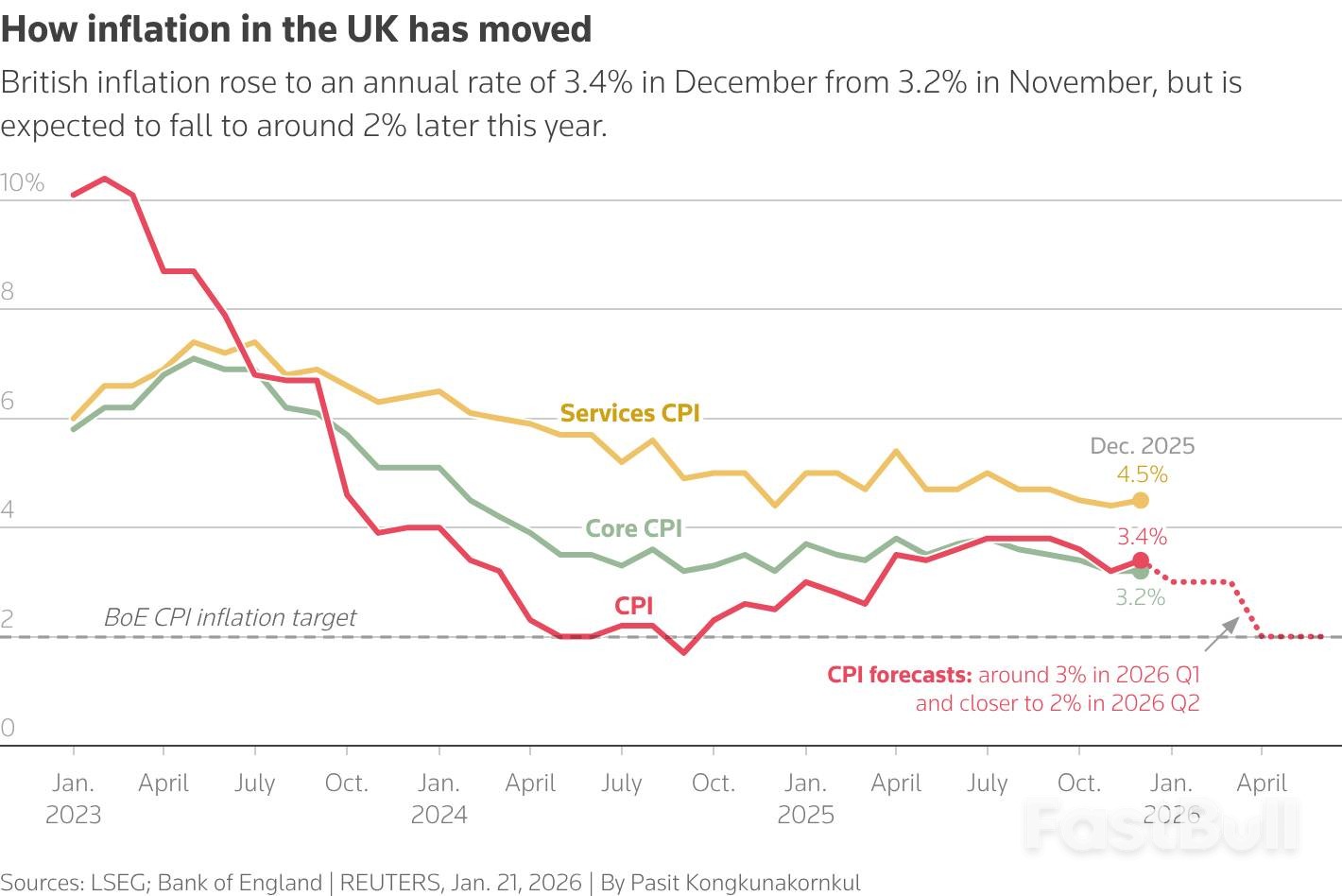

UK inflation unexpectedly rose to 3.4%, but rate cuts remain likely despite external geopolitical threats.

UK inflation unexpectedly climbed for the first time since July, hitting 3.4% in December and complicating the path toward price stability. Despite the increase, investors and economists largely believe the upward blip won't derail the Bank of England's plan to cut interest rates later this year.

Official data shows the Consumer Price Index (CPI) rose from 3.2% in November, surpassing the 3.3% that economists had forecasted.

Key takeaways from the latest report include:

• Headline Inflation: Reached 3.4% in December.

• Primary Drivers: Price hikes were mainly caused by increased tobacco duties and seasonal airfare costs.

• Market Reaction: Financial markets remained steady, with expectations for 2026 rate cuts unchanged.

• Services Inflation: A crucial metric for the central bank, services price inflation edged up to 4.5% from 4.4%, aligning perfectly with forecasts.

The primary forces behind the December inflation increase were higher prices for tobacco products, following a rise in duties, and the typical surge in airfares around the Christmas holiday period.

While the headline number was higher than expected, Adam Deasy, an economist at PwC, described the event as a "speed-bump, rather than an indication we are veering off course on the road to price stability."

This sentiment is shared across the market, as the underlying drivers are seen as temporary rather than a sign of persistent inflationary pressure.

Despite the uptick, the Bank of England (BoE) is widely expected to proceed with interest rate cuts in 2026. The central bank is focused on the broader trend, which still points toward a significant slowdown in price growth over the coming months.

BoE Governor Andrew Bailey has previously stated that he expects inflation to fall close to the bank's 2% target by April or May. Consequently, the latest data did little to move the pound or alter market bets on future monetary policy.

"The Bank of England will... not be worried by these numbers," noted Nicholas Crittenden, an economist from the National Institute of Economic and Social Research. He added, "We still predict one cut in Bank Rate in the first half of this year."

Financial markets are currently pricing in one or possibly two quarter-point rate cuts by the BoE in 2026. This reflects confidence that the disinflationary trend will overcome short-term volatility.

While the domestic inflation picture appears manageable, external factors pose a significant risk. Governor Bailey recently highlighted that the BoE is worried about how markets are reacting to geopolitical developments.

These concerns are materializing in energy markets. British natural gas futures have surged by approximately 25% in the last two weeks, partly due to deteriorating relations with the United States, a key supplier of liquefied natural gas. The tensions stem from President Donald Trump's threats of tariffs on European allies who oppose his Greenland takeover plan. An escalation could disrupt supply chains and push energy costs higher, complicating the BoE's inflation fight.

Even with the December surprise, Britain's consumer price and services inflation rates are running slightly below the BoE's own projections from its November forecasts. However, the UK continues to have the highest inflation rate in the Group of Seven, paired with sluggish economic growth.

Data on producer prices, which can be a leading indicator for consumer inflation, showed a sharp increase in the services sector during the fourth quarter, rising to 2.9% from 2.0%. Meanwhile, output price inflation for manufacturers remained stable.

The BoE's Monetary Policy Committee last cut the Bank Rate to 3.75% in December, but the decision was not unanimous. Nearly half of its members voted to hold rates steady, citing concerns about persistent inflation, a signal that the debate over policy easing is far from over.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up