Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

U.S. President Donald Trump on Wednesday imposed a 25% tariff on goods imported from India starting August 1, as well as an unspecified penalty for buying Russian arms and oil - moves that could strain relations with the world's most populous democracy.

U.S. President Donald Trump on Wednesday imposed a 25% tariff on goods imported from India starting August 1, as well as an unspecified penalty for buying Russian arms and oil - moves that could strain relations with the world's most populous democracy.

The U.S. decision singles out India more severely than other major trading partners, and threatens to unravel months of talks between the two countries, undermining a key strategic partner of Washington’s and a counterbalance to China.

"While India is our friend, we have, over the years, done relatively little business with them because their Tariffs are far too high, among the highest in the World, and they have the most strenuous and obnoxious non-monetary Trade Barriers of any Country," Trump wrote in a Truth Social post.

"They have always bought a vast majority of their military equipment from Russia, and are Russia’s largest buyer of ENERGY, along with China, at a time when everyone wants Russia to STOP THE KILLING IN UKRAINE — ALL THINGS NOT GOOD!"

In response, the Indian government said in a statement that it was studying the implications of Trump's announcements and remained dedicated to securing a fair trade deal with the U.S.

"India and the U.S. have been engaged in negotiations on concluding a fair, balanced and mutually beneficial bilateral trade agreement over the last few months. We remain committed to that objective," it said.

The White House had previously warned India about its high average applied tariffs - nearly 39% on agricultural products - with rates climbing to 45% on vegetable oils and around 50% on apples and corn.

Russia continued to be the top oil supplier to India during the first six months of 2025, making up 35% of overall supplies.

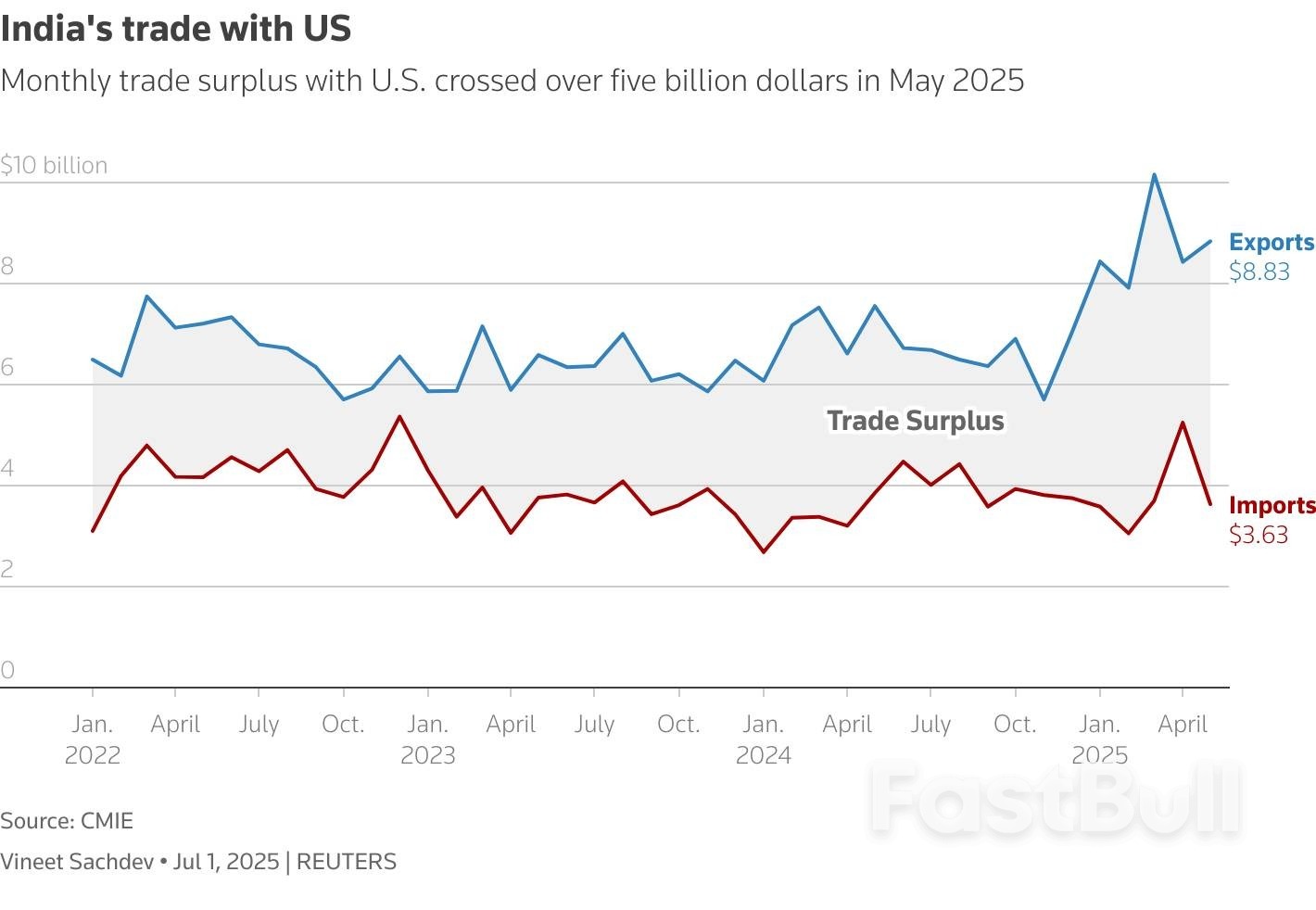

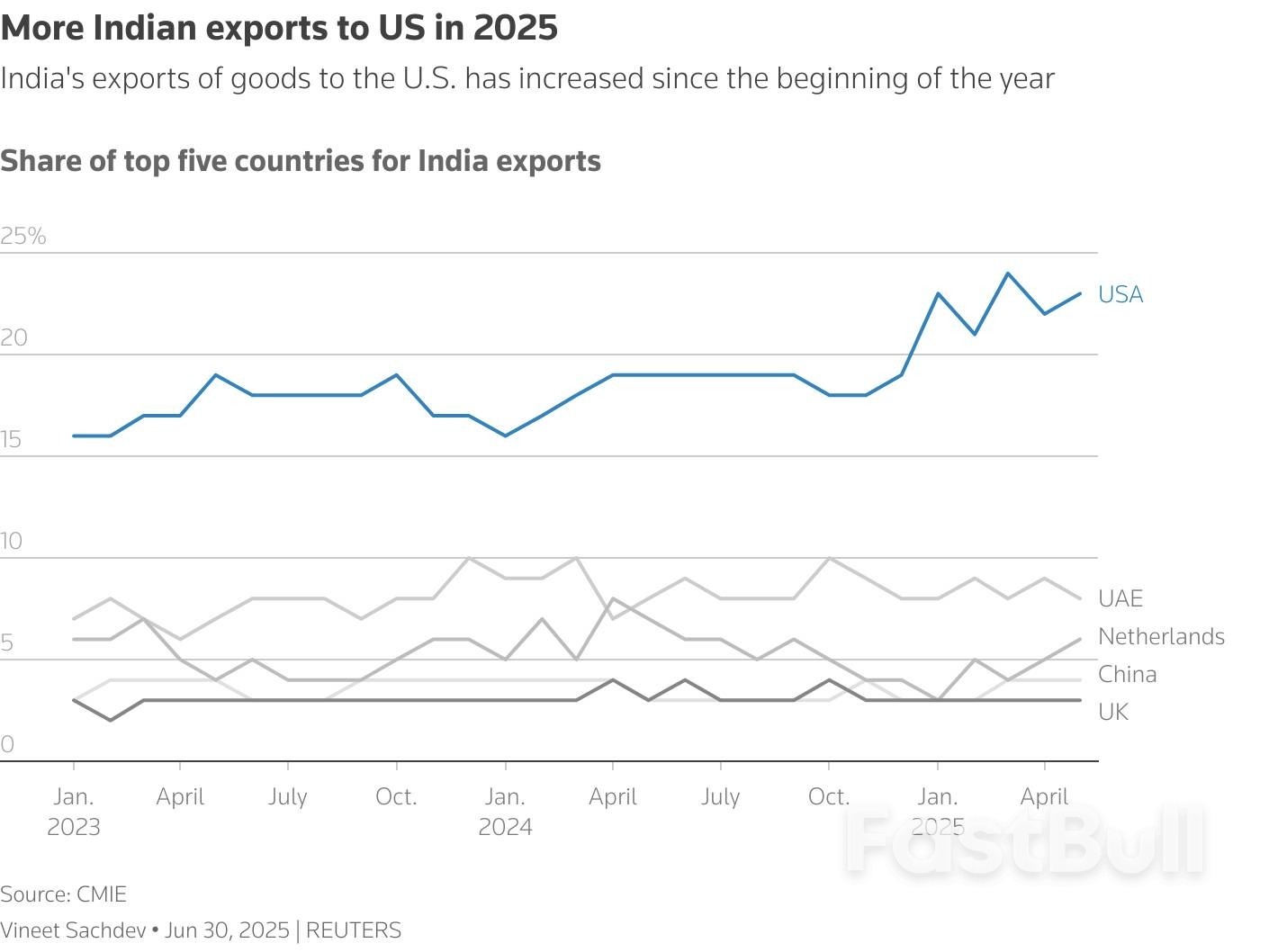

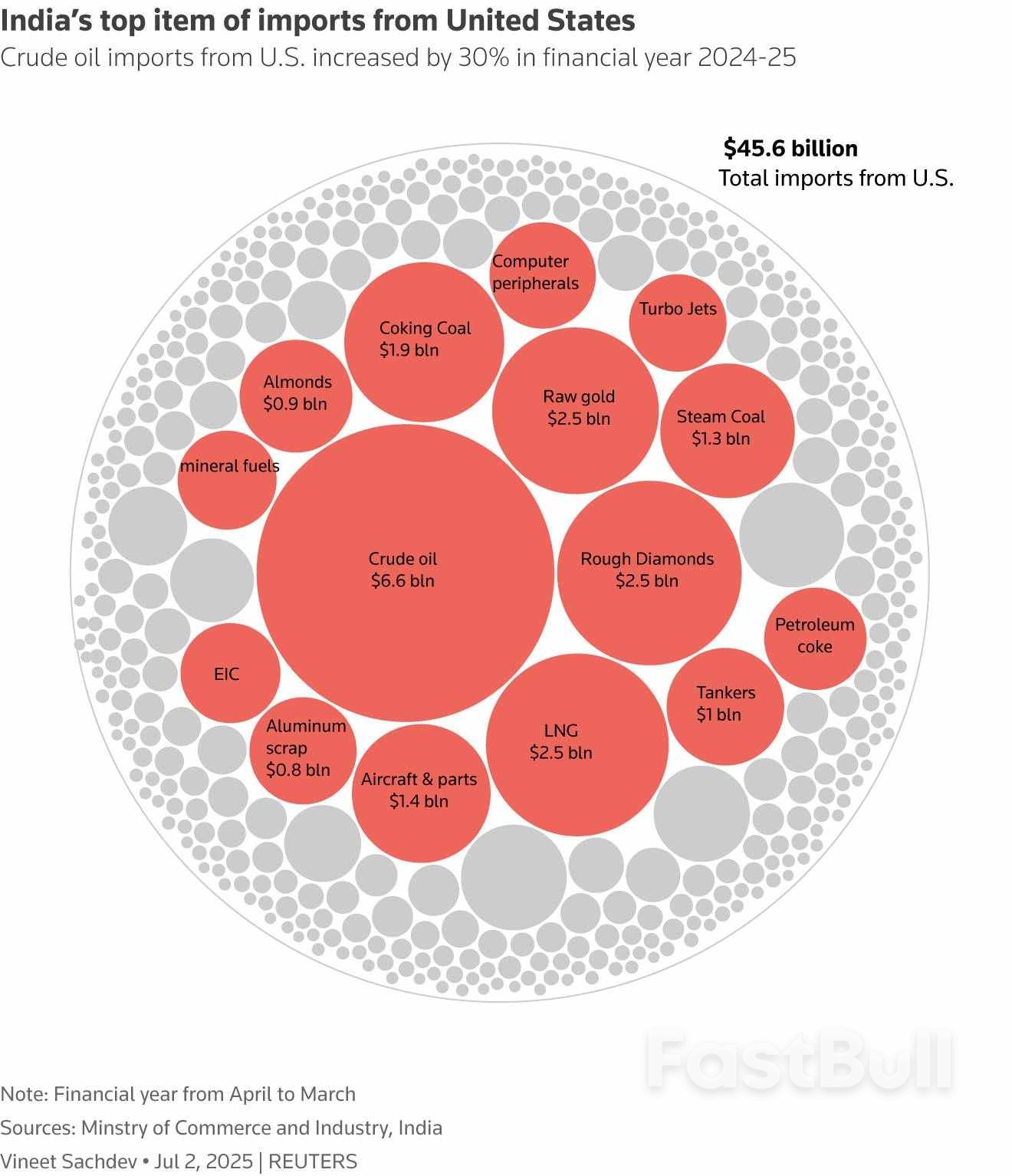

The United States, the world's largest economy, currently has a $45.7 billion trade deficit with India, the fifth largest.

White House economic adviser Kevin Hassett said Trump has been frustrated with the progress of trade talks with India and believed the 25% tariff announcement would help the situation. Hassett said more information on the additional penalty would be made "shortly."

The new U.S. tax on imports from India would be higher than many other countries that struck a deal with the Trump administration recently. Vietnam's tariff is set at 20% and Indonesia's at 19%, while the levy for Japan and the European Union is 15%.

"This is a major setback for Indian exporters, especially in sectors like textiles, footwear and furniture, as the 25% tariff will render them uncompetitive against rivals from Vietnam and China," said S.C. Ralhan, president of the Federation of Indian Export Organisation.

The news pushed the Indian rupee down 0.4% to around 87.80 against the U.S. dollar in the non-deliverable forwards market, from its close at 87.42 during market hours. Gift Nifty futures were trading at 24,692 points, down 0.6%.

U.S. and Indian negotiators have held multiple rounds of discussions to resolve contentious issues, particularly over market access into India for U.S. agricultural and dairy products.

In its latest statement, India said it attached the utmost importance to protecting and promoting the welfare of its farmers, entrepreneurs and small businesses.

"The government will take all steps necessary to secure our national interest, as has been the case with other trade agreements," it said.

The setback comes despite earlier commitments by Prime Minister Narendra Modi and Trump to conclude the first phase of a trade deal by autumn 2025 and expand bilateral trade to $500 billion by 2030, from $191 billion in 2024.

Since India's short but deadly conflict with arch South Asian rival Pakistan, New Delhi has been unhappy about Trump's closeness with Islamabad and has protested, which cast a shadow over trade talks.

"Politically the relationship is in its toughest spot since the mid-1990s," said Ashok Malik, partner at advisory firm The Asia Group. "Trust has diminished. President Trump's messaging has damaged many years of careful, bipartisan nurturing of the U.S.-India partnership in both capitals."

Besides farm products access, the U.S. had flagged concerns over India's increasingly burdensome import-quality requirements, among its many non-tariff barriers to foreign trade, in a report released in March.

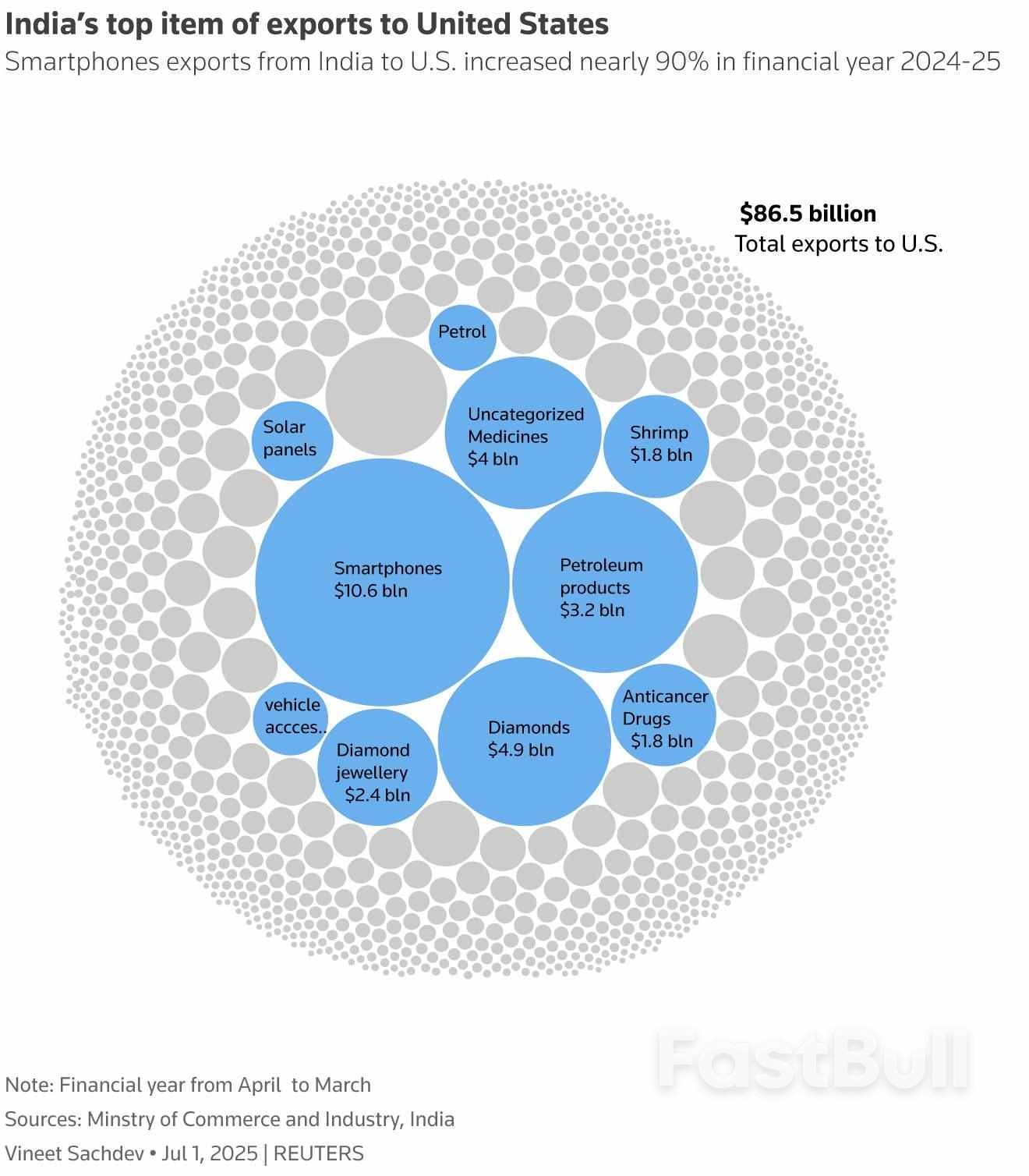

The new tariffs will impact Indian goods exports to the U.S., estimated at around $87 billion in 2024, including labour-intensive products such as garments, pharmaceuticals, gems and jewelry, and petrochemicals.

Reporting by Susan Heavey, Katharine Jackson in Washington, Manoj Kumar and Aftab Ahmed in New Delhi; editing by Doina Chiacu, Bernadette Baum and Mark Heinrich

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Daily Light Crude Oil Futures

Daily Light Crude Oil Futures