Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Amid personal financial optimism, record job market anxiety and rising inflation challenge the Federal Reserve.

A new report from the New York Federal Reserve reveals a growing disconnect in the American economy: while households feel better about their personal finances, anxiety over the U.S. job market has climbed to a record high. The December survey also showed a notable increase in near-term inflation expectations.

According to the New York Fed’s Survey of Consumer Expectations, Americans' confidence in finding a new job if they become unemployed has fallen to its lowest level since the survey began in 2013. This concern was most pronounced among households earning less than $100,000 per year.

The December data painted a complex picture of the labor market. While fewer people expected the overall unemployment rate to rise compared to November, the perceived probability of personally losing a job actually increased. At the same time, the likelihood of voluntarily leaving a job declined, suggesting workers are becoming more cautious.

Households are bracing for rising prices in the near future. The survey showed that one-year inflation expectations rose to 3.4% in December, up from 3.2% in November. This uptick coincides with price pressures linked to the Trump administration's tariffs.

However, longer-term inflation outlooks remained stable, with both three-year and five-year expectations holding steady at 3%. Federal Reserve officials typically place more emphasis on these long-term projections, as they are considered a more reliable indicator of public confidence in the central bank's ability to control inflation.

New York Fed President John Williams commented in late December that future inflation projections "remain well-anchored," adding that he watches this data closely because it is "critical to ensuring low and stable inflation."

The survey’s findings highlight the challenge facing the Federal Reserve. Last month, the central bank cut its benchmark interest rate to a range of 3.50%-3.75% in an effort to shield the job market from risks while inflation remains significantly above its 2% target.

Fed officials anticipate that the unemployment rate, which stood at 4.6% in November, will decline slightly this year. They also forecast that inflation will moderate but stay above the target level. Many officials believe the price impact from tariffs will fade over the year, but they are monitoring inflation expectations for any signs that the public is losing faith.

The U.S. Labor Department is set to release its official December employment report on Friday, which will provide a clearer picture of the job market's health.

Despite widespread job market fears, the survey found that households were generally more optimistic about their current and future financial situations in December.

However, this optimism was tempered by other concerns:

• Tighter Credit: Respondents reported that it is becoming more difficult to access credit.

• Debt Worries: The expected probability of missing a debt payment rose to its highest level since the early days of the pandemic in April 2020.

• Income vs. Spending: While expectations for income growth saw a slight increase, forecasts for spending and earnings growth both declined.

Looking ahead, the path for Fed policy in 2026 remains uncertain. Philadelphia Fed President Anna Paulson recently stated that if the economy performs as she expects, "some modest further adjustments to the (federal) funds rate would likely be appropriate later in the year."

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

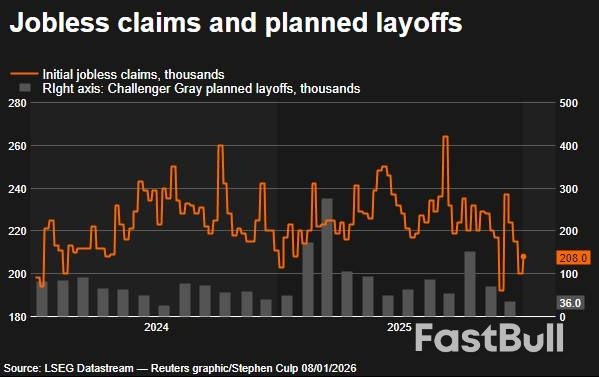

Initial jobless claims and Challenger Gray layoffs

Initial jobless claims and Challenger Gray layoffs