Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.K. Trade Balance Non-EU (SA) (Oct)

U.K. Trade Balance Non-EU (SA) (Oct)A:--

F: --

P: --

U.K. Trade Balance (Oct)A:--

F: --

P: --

U.K. Services Index MoMA:--

F: --

P: --

U.K. Construction Output MoM (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output YoY (Oct)A:--

F: --

P: --

U.K. Trade Balance (SA) (Oct)A:--

F: --

P: --

U.K. Trade Balance EU (SA) (Oct)A:--

F: --

P: --

U.K. Manufacturing Output YoY (Oct)A:--

F: --

P: --

U.K. GDP MoM (Oct)A:--

F: --

P: --

U.K. GDP YoY (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output MoM (Oct)A:--

F: --

P: --

U.K. Construction Output YoY (Oct)A:--

F: --

P: --

France HICP Final MoM (Nov)

France HICP Final MoM (Nov)A:--

F: --

P: --

China, Mainland Outstanding Loans Growth YoY (Nov)

China, Mainland Outstanding Loans Growth YoY (Nov)A:--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)A:--

F: --

P: --

India CPI YoY (Nov)

India CPI YoY (Nov)A:--

F: --

P: --

India Deposit Gowth YoYA:--

F: --

P: --

Brazil Services Growth YoY (Oct)

Brazil Services Growth YoY (Oct)A:--

F: --

P: --

Mexico Industrial Output YoY (Oct)

Mexico Industrial Output YoY (Oct)A:--

F: --

P: --

Russia Trade Balance (Oct)

Russia Trade Balance (Oct)A:--

F: --

P: --

Philadelphia Fed President Henry Paulson delivers a speech

Philadelphia Fed President Henry Paulson delivers a speech Canada Building Permits MoM (SA) (Oct)

Canada Building Permits MoM (SA) (Oct)A:--

F: --

P: --

Canada Wholesale Sales YoY (Oct)A:--

F: --

P: --

Canada Wholesale Inventory MoM (Oct)A:--

F: --

P: --

Canada Wholesale Inventory YoY (Oct)A:--

F: --

P: --

Canada Wholesale Sales MoM (SA) (Oct)A:--

F: --

P: --

Germany Current Account (Not SA) (Oct)

Germany Current Account (Not SA) (Oct)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)--

F: --

P: --

Canada Existing Home Sales MoM (Nov)--

F: --

P: --

Euro Zone Total Reserve Assets (Nov)--

F: --

P: --

U.K. Inflation Rate Expectations--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

Canada New Housing Starts (Nov)--

F: --

P: --

U.S. NY Fed Manufacturing Employment Index (Dec)--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)--

F: --

P: --

Canada Core CPI YoY (Nov)--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)--

F: --

P: --

Canada Core CPI MoM (Nov)--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)--

F: --

P: --

Canada CPI YoY (Nov)--

F: --

P: --

Canada CPI MoM (Nov)--

F: --

P: --

Canada CPI YoY (SA) (Nov)--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

The Malaysian unemployment rate remained steady in January, amid an improving labour market, according to a survey conducted by the Department of Statistics Malaysia (DOSM).

The Malaysian unemployment rate remained steady in January, amid an improving labour market, according to a survey conducted by the Department of Statistics Malaysia (DOSM).

In the latest Labour Force Survey released on Tuesday, the unemployment rate stood at 3.1%, representing 533,800 individuals.

Chief statistician Datuk Sri Dr Mohd Uzir Mahidin said the country's labour market was in an upward trend in January, reflecting an ongoing improvement in the nation's economic conditions, despite some challenges in trade and inflation.

The labour force improved further, growing by 0.3% month-on-month to 17.22 million persons, according to the survey.

The chief statistician said this positive trend was driven by an increase in employment, while the number of unemployed persons continued to decline, with the labour force participation rate remaining at 70.6% as in the previous month.

Meanwhile, employment growth was observed across key economic sectors, with the services sector demonstrating notable growth, particularly within accommodation and food and beverage services, wholesale and retail trade, and human health and social work activities.

Positive employment trends were also evident in manufacturing, construction, agriculture, and mining and quarrying.

Youth unemployment saw a slight decrease for ages between 15 and 24, and remained stable for ages between 15 and 30.

The survey noted that the youth unemployment rate, specifically for those aged 15 to 24, decreased by 0.1 percentage point to 10.3%, representing 299,300 individuals.

Whereas, for youths aged 15 to 30, the unemployment rate stayed at 6.3%, with 402,400 persons unemployed.

The number of individuals outside the labour force marginally declined by 0.3%, with housework/family and schooling/training remaining the primary reasons for non-participation.

The survey showed that housework or family responsibilities accounted for 43.6% of non-particication, followed by schooling or training at 41.8%.

Malaysia’s resilient economic position had a positive impact on the country's labour market, the DOSM's statement read.

This situation is supported by strong domestic demand, government initiatives, increased tourism activities, and ongoing investment activities in infrastructure projects and key sectors.

In line with the country's growing economic performance and strong growth in major sectors of the country's economy, the nation’s labour market is foreseen to remain in a stable growth momentum with increasing employment, while unemployment is declining, according to the statement.

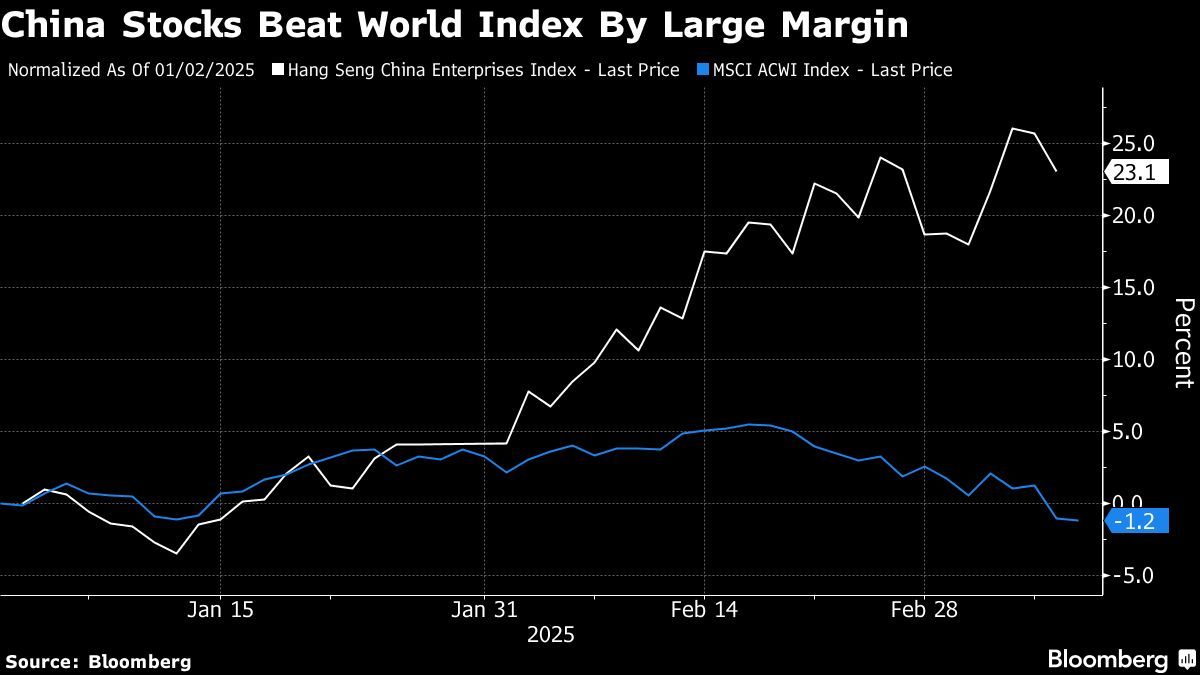

Global long-term investors are placing billions of dollars worth of orders in Chinese deals after years of largely shunning them.

In the past week in Hong Kong, deep-pocketed firms known as “long-only” investors — such as mutual funds — have bought shares in electric-car giant BYD Co and bubble-tea maker Mixue Group, as well as Baidu Inc bonds exchangeable into Trip.com Group Ltd stock, according to people familiar with the matter.

It’s a significant development because the return of such buy-and-hold investors is seen as crucial to laying the foundations for stable and sustainable gains in Chinese stocks. Long-term investors had stayed away from Chinese stocks over the past few years amid a prolonged market slump.

“Long-only investors have a longer investment horizon and are less likely to sell shares immediately after an IPO,” said Andy Wong, IPO leader at advisory firm SW Hong Kong. “Their participation in the market can provide stability to the company’s stock price in relatively volatile capital markets created by short-term investors.”

For now, those funds appear most visible in the biggest deals. They participated in BYD’s recent US$5.6 billion (RM24.82 billion) share sale, Hong Kong’s biggest one in nearly four years. Baidu’s US$2 billion offering of bonds exchangeable to Trip.com shares matched a record for that type of security by an Asian company.

Long-only investors snapped up at least US$1.5 billion of BYD’s shares, while in Baidu’s offering, they ordered enough to cover the entire deal, people familiar with the matter said.

“The scale of the transactions is reminiscent of 2021,” said Phyllis Wang, Goldman Sachs Group Inc’s head of equity capital markets syndicate for Asia excluding Japan, referring to recent Chinese deals broadly.

The return of long-term investors to these offerings coincides with the rally in Chinese stocks, triggered by DeepSeek’s artificial-intelligence breakthrough, which supercharged investors’ perceptions about Chinese technology companies. The gains added to positive sentiment from Beijing’s economic stimulus measures, which late last year also helped draw global investors back to deals in Hong Kong.

Despite this week’s global selloff, the market watchers continue to be bullish on the outlook for Chinese stocks. Citigroup Inc just raised its outlook for Chinese stocks to overweight, and the Hang Seng China Enterprises Index is up more than 18% this year.

Goldman Sachs strategists led by Kinger Lau recently noted that global long-only investors have become more engaged in Chinese IPOs and share sales lately and are increasingly motivated to buy more shares of Chinese companies due to volatility in the US stock market.

Ivy Hu, head of China ECM at UBS Group AG, which helped arrange BYD’s deal, said that offering showed that large investors from the US and Europe have begun returning to Chinese share sales. That’s a contrast to the post-2021 landscape where Asia-based investors were the dominant buyers, she said.

The outlook for Chinese IPOs appears robust, though the pace of deals may pick up after this month because many companies are in their so-called blackout periods ahead of their earnings releases, Hu said. Bloomberg Intelligence predicts Hong Kong’s IPO market will more than double to US$22 billion this year.

Still, the return of global investors appears to be limited to certain Chinese deals. In the broader equities market, mutual funds engaged in active stock picking continued to sell Chinese stocks despite the rally, according to data from Morgan Stanley.

Take Barry Wang, a portfolio manager at Oberweis Asset Management. He said he’s been looking into more deals this year, but they would still need to be priced attractively for him to pick them up.

“Overall sentiment is improving toward China,” Wang said. “But after a strong year-to-date rally, valuation and business fundamentals should be key factors in considering these deals.”

The risk-off sentiment that triggered the biggest US stock market selloff in months has spilled over into Asian markets, leading to broad declines across the region. The currency markets reflect this shift too, with traditional safe havens such as Japanese Yen and Swiss franc leading gains in Asia, while risk-sensitive currencies like the Australian and New Zealand Dollars face pressure.

Unlike previous bouts of risk aversion, Dollar is not benefiting from the current flight to safety. This time, the core of the problem originates from the US economy itself, where recession worries are intensifying. Rather than flocking to the greenback, investors appear to be diversifying into other safe havens or moving to the sidelines until the dust settles.

The uncertainty surrounding US trade policies has left businesses and consumers hesitant, potentially dragging economic growth lower. In response to the changing economic outlook, market participants are increasingly convinced that Fed will resume policy easing within the first half of the year. The only question is whether the next rate cut will arrive in May or June.

Another driver of Dollar weakness is the extending decline in yields since mid January. Technically, there is prospect for 10-year yield to draw support from 4.000 psychological level, which is slightly below 61.8% retracement of 3.603 to 4.809 at 4.063, to form a near term bottom. However, there is little prospect for 10-year yield to rebound strongly through 55 D EMA (now at 4.412). But at least, sideway movement in 10-year yield could help lift the pressure on Dollar.

Overall for the week so far, Yen is the best performer, followed by Euro, and then Swiss Franc. Aussie is the worst, followed by Loonie and then Kiwi. Dollar and Sterling are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -1.02%. Hong Kong HSI is down -1.02%. China Shanghai SSE is down -0.50%. Singapore Strait Times is down -2.02%. Japan 10-year JGB yield is down -0.063 at 1.509. Overnight, DOW fell -2.08%. S&P 500 fell -2.70%. NASDAQ fell -4.00%. 10-year yield fell -0.104 to 4.213.

US stock market correction deepens as recession fears take hold

The US stock market suffered its most significant setback in months, with the S&P 500 dropping -2.7%, its biggest one-day decline since December 18. NASDAQ also lost -4.0%, marking its worst single-day percentage loss since September 2022. Analysts widely point to mounting recession worries as the primary catalyst behind the selloff.

Initial concerns emerged over the past month following a series of weaker economic data points, believed by some to be early reactions to an increasingly contentious tariff policy. These worries intensified after recent remarks from the White House suggested a bumpy economic outlook ahead.

In an interview aired on Sunday, US President Donald Trump fueled apprehensions further by describing the economy as going through “a period of transition.” When pressed about an impending recession, he avoided a direct prediction but acknowledged potential “disruption.” His remarks—“Look, we’re going to have disruption, but we’re OK with that”—did little to reassure investors already on edge about growth prospects.

Adding further weight to recession fears, historical bond market indicators have been flashing warning signs. The 10-year to 2-year US yield curve inverted in mid-2022—a classic recession signal—and only turned positive again in September 2024. Historically, a U.S. recession tends to follow within months after the yield curve normalizes (i.e., turned positive again). If this trend holds true, the US economy could be inching closer to a downturn.

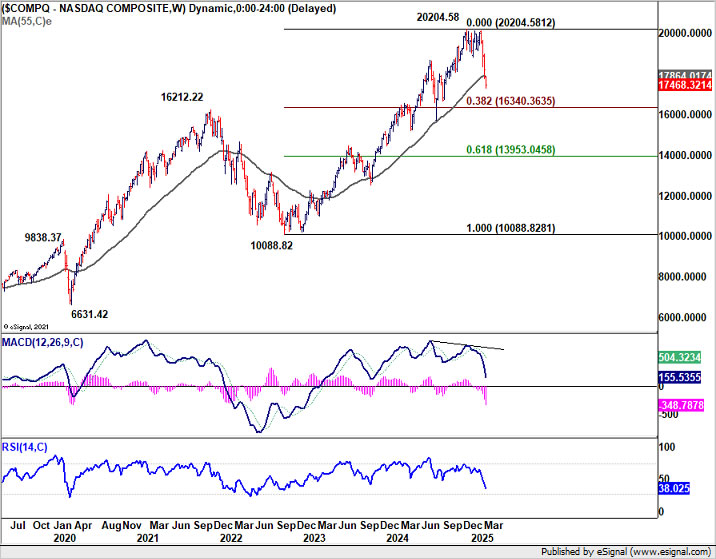

However, another view posits that tariffs are a distraction and that the real driver behind the US selloff is the recent surge in Japanese government bond yields, which have hit a 16-year high. As the carry trade unwinds—where investors borrow in low-yield currencies, often involving Japanese Yen, to fund investments in higher-yield or high-growth assets—capital is flowing out of big tech names, contributing to the NASDAQ’s outsized losses.

Technically, NASDAQ’s strong break of 55 W EMA (now at 17864.01) suggests that it’s already in correction to the up trend from 10088.82 (2022 low). Deeper fall should be seen to 38.2% retracement of 10088.82 to 20204.58 at 16340.36. Reaction from there will decide whether it’s merely in a medium consolidations phase or in an out-right bearish trend reversal.

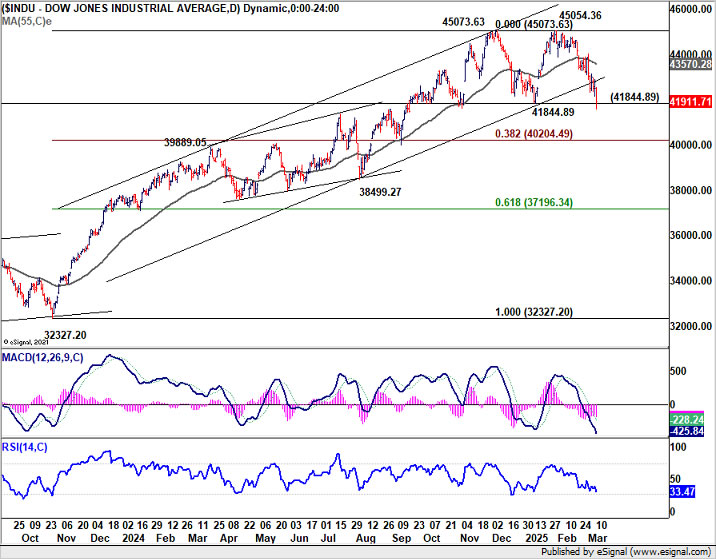

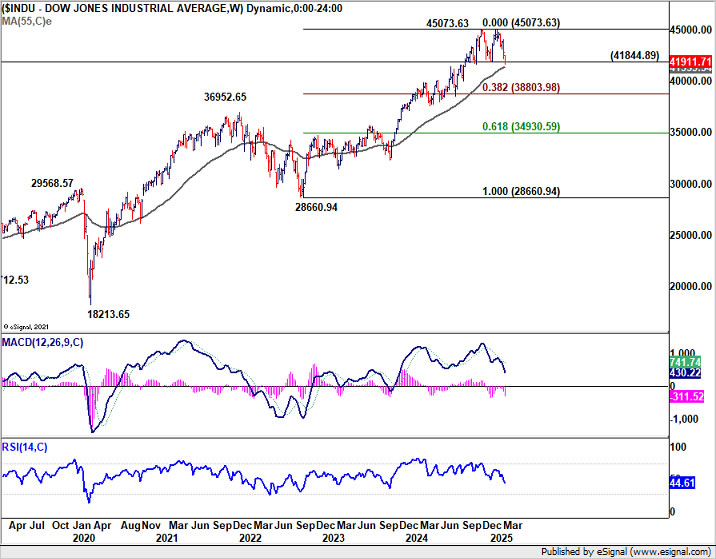

As for DOW, immediate focus is now on 41844.89 support. Firm break there will complete a double top reversal pattern (45073.63, 45054.36). That should set up deeper fall to 38.2% retracement of 32327.20 to 45073.63 at 40204.49 at least, even it’s just a correction to the rise from 32327.20.

Australia Westpac consumer sentiment jumps to 95.9, soft landing achieved

Australian consumer sentiment saw a strong rebound in March, with Westpac Consumer Sentiment Index jumping 4.0% mom to 95.9, the highest level in three years and not far from neutral 100 mark.

Westpac attributed the improvement to slowing inflation and February’s RBA interest rate cut which have lifted confidence across households. positive views on job security suggest that “soft landing has been achieved”. Nevertheless, “unsettling overseas news” continues to weigh on the broader economic outlook.

Looking ahead to RBA’s upcoming meeting on March 31-April 1, Westpac expects the central bank to keep the cash rate unchanged. RBA was clear that the 25bps cut in February “did not mean further reductions could be expected at subsequent meetings.”

Westpac added, “further slowing in inflation will give the RBA sufficient confidence to deliver more rate cuts this year with the next move coming at the May meeting”.

Australia’s NAB business confidence slips back into negative as cost pressures persist

Australia’s NAB Business Confidence fell from 5 to -1 in February, erasing last month’s gain and returning to below-average levels. While business conditions improved slightly from 3 to 4, the decline in confidence suggests that businesses remain cautious despite RBA’s recent rate cut and positive Q4 GDP data.

NAB Chief Economist Alan Oster noted that the lift in sentiment seen in January was not sustained, signaling ongoing uncertainty in the business environment. Persistent cost pressures and subdued profitability appear to be key factors weighing on sentiment, keeping confidence below long-term norms.

Within business conditions, trading conditions ticked up from 7 to 8, and profitability conditions rose slightly from -2 to -1, though still remaining in negative territory. Employment conditions, however, weakened from 5 to 4.

Cost pressures remain a concern, with purchase cost growth accelerating from 1.1% to 1.5% in quarterly equivalent terms. On the positive side, labor cost growth eased from 1.7% to 1.5%, indicating that wage price pressures are gradually cooling. Meanwhile, final product price growth slowed from 0.8% to 0.5%, though retail price inflation held steady at 1.0%.

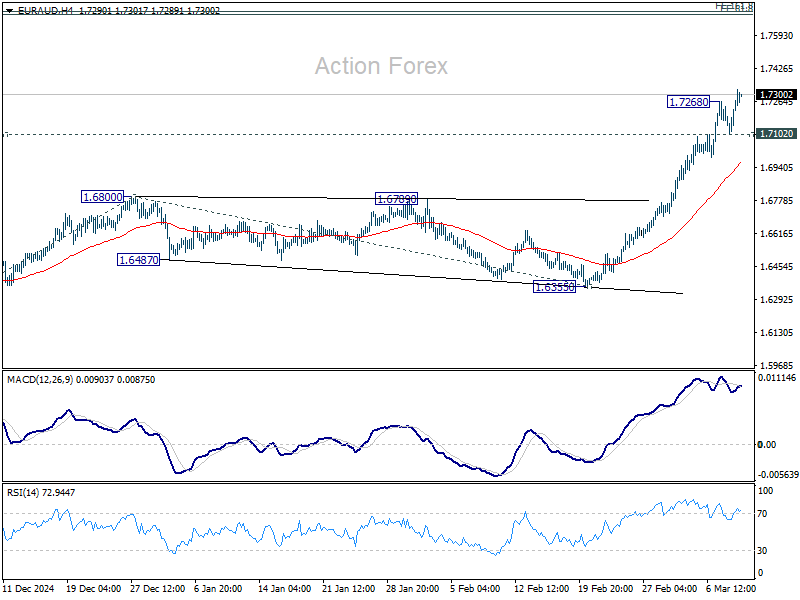

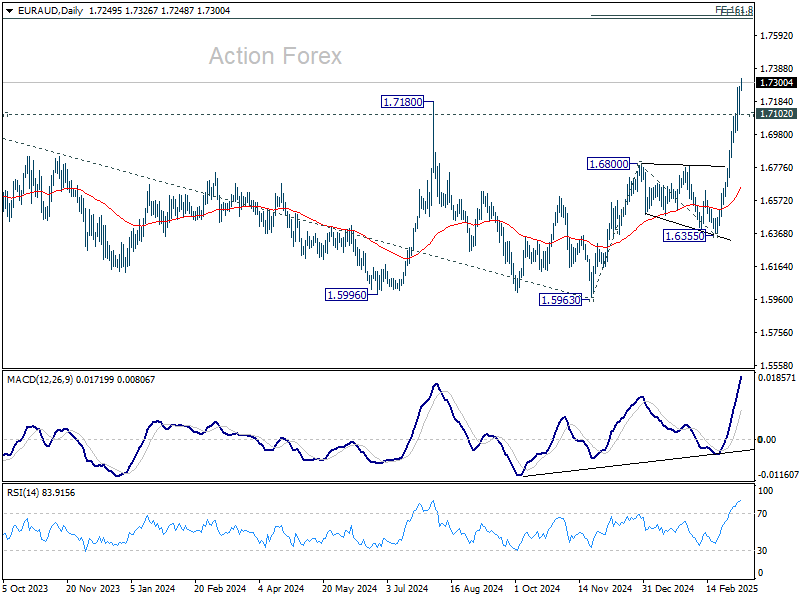

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7149; (P) 1.7213; (R1) 1.7320; More…

EUR/AUD’s rally resumed and brief consolidations and intraday is back on the upside. Rise from 1.6335 should now target 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next. On the downside, below 1.7102 minor support will turn intraday bias neutral again and bring consolidations, before staging another rally.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 key resistance will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6355 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q4 | 2.60% | -1.20% | 0.20% | |

| 23:30 | AUD | Westpac Consumer Confidence Mar | 4.00% | 0.10% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 0.80% | 3.60% | 2.70% | |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.60% | 0.70% | 0.70% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 2.90% | 2.80% | 2.80% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 1.20% | 1.40% | 1.30% | |

| 00:30 | AUD | NAB Business Confidence Feb | -1 | 4 | 5 | |

| 00:30 | AUD | NAB Business Conditions Feb | 4 | 3 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | 4.70% | |||

| 10:00 | USD | NFIB Business Optimism Index Feb | 101 | 102.8 |

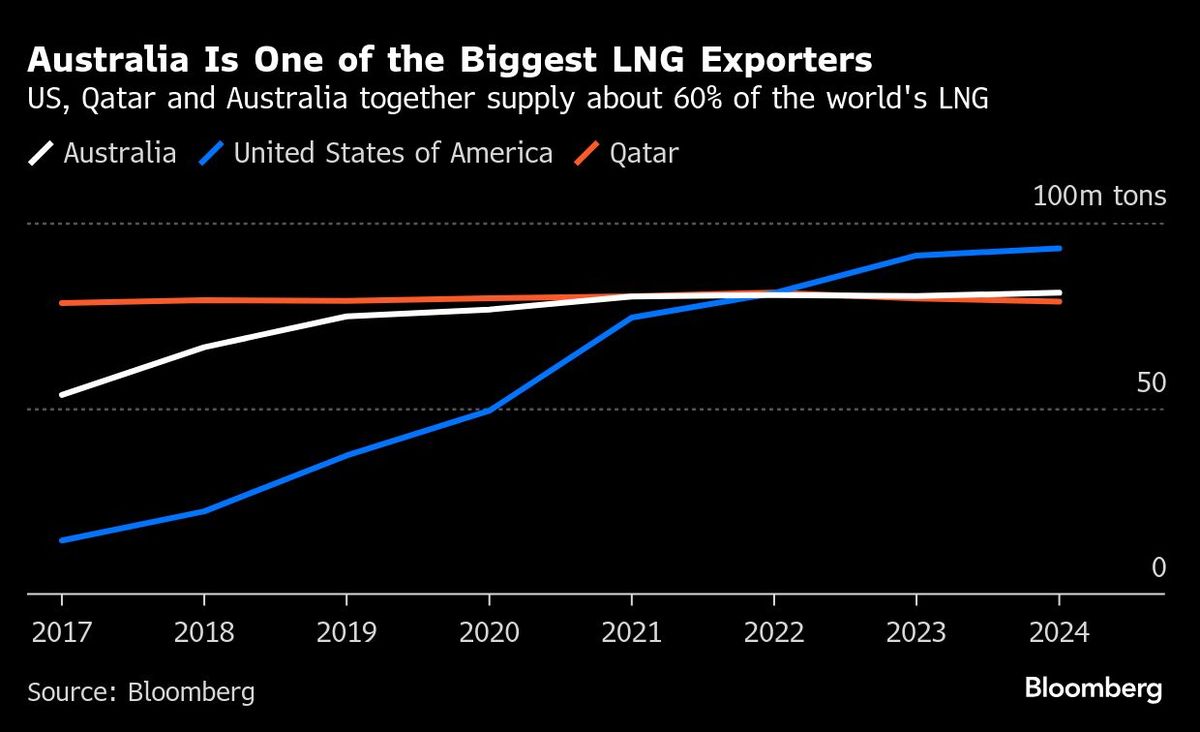

The lopsidedness of Australia’s fossil fuel endowment and demographic spread, coupled with insufficient infrastructure, means one of the world’s biggest exporters of liquefied natural gas will soon have to import the fuel.

Eastern Australia is facing an energy shortfall as older offshore gas fields are depleted, according to Rystad Energy. There’s limited pipeline capacity to ship LNG thousands of miles from major production hubs in the northwest of the country and the grid operator has repeatedly warned of potential shortages in the populous southeast as soon as 2027.

New South Wales, Victoria and Tasmania are already “testing their gas supply security for winter,” Kaushal Ramesh, Rystad Energy’s vice president for gas & LNG research, said in a note. That risks a repeat of an energy crunch three years ago, he said.

“Compared to the crisis year of 2022, these states now have severely diminished buffer capacity, which could trigger another price surge if multiple supply and demand shocks occur,” Ramesh said. “Even in our most optimistic scenario, LNG imports to Australia are looking like an inevitability.”

Energy policy is likely to take centre stage in elections due by mid-May, where the ruling Labour party’s target to generate 82% of electricity from renewables will face off against the opposition’s pledge to build nuclear reactors, the research group said.

The Victorian government will push for the Australian Energy Market Operator to become an anchor buyer of LNG at a meeting of state and federal energy ministers on Friday, according to a report Monday in The Australian newspaper. Companies including billionaire Andrew Forrest’s Squadron Energy, Viva Energy Group and Royal Vopak NV have proposed LNG import terminals.

Australia would not be the first gas exporter that would need to turn to imports, although countries including Egypt and Indonesia have mainly needed to do so to meet increasing domestic demand caused by rapid population growth.

“It is ridiculous that one of the world’s largest gas exporters is looking to import gas,” said Saul Kavonic, an energy analyst at MST Marquee. “There is still ample gas in Queensland, where the LNG export projects are, but pipeline and storage constraints can still limit gas capacity in the southern states when it is suddenly needed.”

Talks between the US and China on trade and other issues are stuck at lower levels, people familiar with the matter said, with both sides talking past each other and failing to agree on the best way to proceed.

While representatives of the two countries have had contact, officials in Beijing say the US hasn’t outlined detailed steps they expect from China on fentanyl in order to have the tariffs lifted, according to the people, who asked not to be identified. The second wave of duties imposed last week took working-level officials on both sides by surprise.

US President Donald Trump’s team rejects the assertion that it hasn’t given clear demands on fentanyl, pointing to messages the White House has sent to China through diplomats in Washington, including Ambassador Xie Feng, according to a person familiar with the matter.

Those included asking China to stop sending chemicals to produce the drug to Mexico, use the death penalty for smugglers and order the People’s Daily newspaper to run a front-page article condemning the fentanyl trade, the person said. The official mouthpiece of the Communist Party generally reserves that space for coverage of Chinese President Xi Jinping.

The disagreements between the two sides — including on whether clear demands have been given — represents a fundamental mismatch in how Trump and Xi do diplomacy. While the US leader has personally negotiated on trade with counterparts from Canada and Mexico, protocol in Beijing typically requires most details to be sorted out before Xi gets on the phone with Trump.

Xi and Trump haven’t spoken since both leaders pledged to retain “strategic communication channels” in a phone call days before the Republican took office, even though the US president said in early February that another conversation would soon take place. A person familiar with the White House thinking said no planning for an in-person meeting between the two leaders is currently taking place.

A White House official said the US has made its expectations clear to China. Treasury, and Commerce Department didn’t respond to requests for comment. China’s foreign, commerce and finance ministries didn’t reply to requests for comment.

China’s Commerce Minister Wang Wentao said last week that he’d written to his US counterpart Howard Lutnick in February, saying he hoped “both sides can meet at an appropriate time.” Treasury Secretary Scott Bessent held a call with Chinese counterpart He Lifeng last month, largely to trade complaints.

Chinese officials prefer to set up a communication channel between Foreign Minister Wang Yi and National Security Adviser Mike Waltz, similar to the arrangement during the Biden era.

When Wang visited New York last month for United Nations meetings, nobody from the Trump administration reached out to him, according to a person familiar with the situation, adding that China saw it as a lost opportunity for an important back channel.

The inability to establish trusted communication links is leading to frustration in Beijing, said Wu Xinbo, an adviser to the Foreign Ministry in Beijing, who last year led a group of Chinese experts connected to the government to meet politicians and business executives in the US.

“The Trump team hasn’t yet figured out exactly what they want to get from China,” said Wu, who is the director at Fudan University’s Center for American Studies in Shanghai. “There isn’t a coherent policy.”

Xi has told his lieutenants to stay “calm” and had been strategic with his retaliation to the US tariffs, deploying targeted measures like levies on soybeans that avoid blowback at home while inflicting pain on Trump voters. But that patience is being tested, with Wang using a high-profile briefing last week to brand US tariffs as “evil” and accuse Trump of “two-faced acts”.

China is agitated that its efforts to stem the fentanyl trade — one of the few areas of cooperation with the Biden administration — haven’t been acknowledged. This month, it published a white paper that details all the steps it has taken to control fentanyl-related substances, including expanding the list of controlled chemicals and cooperating with US law enforcement.

China is willing to take judicial action against companies and individuals engaged in illegal production of fentanyl precursors, but the US hasn’t provided concrete evidence, according to Da Wei, director of the Center for International Security and Strategy at Tsinghua University in Beijing, who frequently travels to the US for talks with policy makers. China also sees the US approach to fentanyl as “very one-sided” and wants consumption addressed as well, he added.

“Without addressing the consumption side, even if China stops exporting precursors, other countries will fill the gap,” Da said. “In fact, fentanyl precursors are not only sourced from China, Mexico, and Canada but also from several other countries.”

Tariff timing

The timing of Trump’s announcements has contributed to China’s annoyance, with the first tariffs landing in the middle of the biggest annual holiday, when almost all government officials were on leave. The second round fell on the eve of Beijing’s biggest annual political event, which was seen as sending a bad signal, according to a person familiar with the matter.

Trump himself has given mixed signals on his approach to China. He has released sweeping trade and investment policies that singled out China, yet he’s also said a deal is possible.

“We want them to invest in the US,” Trump said last month. He added that the US-China relationship “will be a very good one”.

While Xi is open to negotiating a deal, during Trump’s first term he resisted US attempts to force China to change its laws.

During the first trade war, China handed out a suspended death sentence for fentanyl smuggling to the US, which Chinese officials then touted as evidence of a “zero tolerance” policy. But the Trump administration now wants more.

“It’s a bit too much to ask a foreign government to change its legal system, especially when it affects people’s lives,” said John Gong, a former consultant to China’s Commerce Ministry who is now a professor at the University of International Business and Economics, referring to the request for harsher sentences.

In any talks with China, the US will want to address five main areas, according to a person familiar with the matter. Those are fentanyl, Beijing’s implementation of a trade deal struck during Trump’s first term, China’s help creating jobs in the American heartland, ensuring the centrality of the dollar in global trade, and Xi’s support in ending the war in Ukraine, the person said.

The fate of Chinese video app TikTok could also be on the agenda, with Trump saying Sunday he was negotiating with four different possible buyers. Beijing would need to approve any potential sale.

China understands it’ll need to show Trump what it’s willing to offer, such as pledging to increase purchases of American goods including energy and agriculture, one of the people said. It could also pledge to invest in American manufacturing and open up its services industry for US investment, the person added.

While the urgency for striking a deal is growing, with China facing more tariffs on steel and aluminum this week, Beijing has shown it is reluctant to be rushed into a situation that could backfire.

Trump’s showdown with Ukrainian President Volodymyr Zelenskiy left no doubt about the risks of meeting such an unpredictable leader, said Neil Thomas, a fellow for Chinese politics at the Asia Society Policy Institute’s Center for China Analysis.

“Chinese diplomats will want ironclad guarantees that no such humiliation will befall their leader,” he added. “The last thing that Xi wants is to be publicly attacked.”

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up