Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

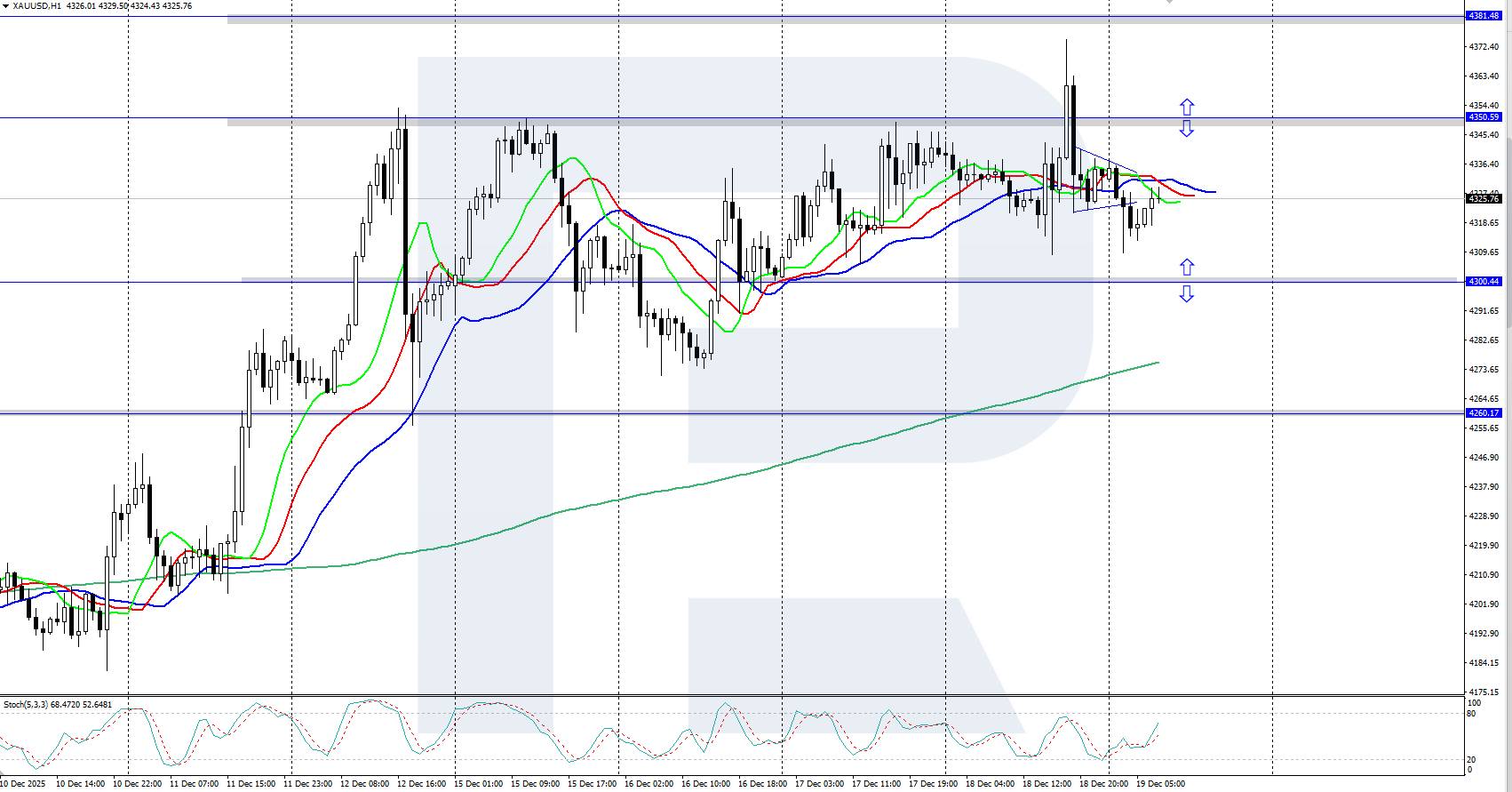

The price of XAUUSD declined toward the 4,300 USD area during a downward correction after an unsuccessful attempt to renew the all-time high, following the release of US inflation data.

The price of XAUUSD declined toward the 4,300 USD area during a downward correction after an unsuccessful attempt to renew the all-time high, following the release of US inflation data.

Gold (XAUUSD) has returned to a consolidation range of 4,260–4,350 USD per ounce, remaining close to record highs. An attempt to renew the all-time high at 4,381 USD after weaker-than-expected US inflation data proved unsuccessful.

US inflation slowed to 2.7% in November, below the 3.1% forecast, while core CPI came in at 2.6% — the lowest reading since March 2021. This has strengthened expectations of a potential Federal Reserve rate cut in 2026.

Geopolitical tensions continue to support the precious metal. Confrontation between the US and Venezuela persists, military action in Ukraine continues, and there has been no clear progress in peace negotiations so far.

XAUUSD quotes corrected toward the 4,300 USD area. The daily trend, confirmed by the Alligator indicator, remains upward, indicating the possibility of a continuation of the bullish move once the current correction is complete.

Within the short-term price forecast for XAUUSD, if bulls manage to regain control, another attempt to break the all-time high at 4,381 USD may follow. If bears succeed in extending the decline and secure prices below 4,300 USD, a deeper correction toward support at 4,260 USD may develop.

Gold is undergoing a moderate correction after failing to renew the all-time high at 4,381 USD. Slowing US inflation and ongoing geopolitical tensions continue to support the precious metal. Once the correction phase is complete, the upward movement may resume.

EURUSD 2026-2027 forecast: key market trends and future predictions

EURUSD 2026-2027 forecast: key market trends and future predictionsThis article provides the EURUSD forecast for 2026 and 2027 and highlights the main factors determining the direction of the pair's movements. We will apply technical analysis, take into account the opinions of leading experts, large banks, and financial institutions, and study AI-based forecasts. This comprehensive insight into EURUSD predictions should help investors and traders make informed decisions.

Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysis

Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysisDive deep into the Gold (XAUUSD) price outlook for 2026 and beyond, combining technical analysis, expert forecasts, and key macroeconomic factors. It explains the drivers behind gold's recent surge, explores potential scenarios including a move toward 4,500 to 5,000 USD per ounce, and highlights why the metal remains a strong hedge during global uncertainty.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up