Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Canada’s economy is likely in the early stages of a recession, according to forecasters, as unemployment rises and exports fall because of a trade war with the US.

Canada’s economy is likely in the early stages of a recession, according to forecasters, as unemployment rises and exports fall because of a trade war with the US.

Economists surveyed by Bloomberg say output will shrink 1% on an annualized basis in the second quarter and 0.1% in the third quarter, a technical recession.

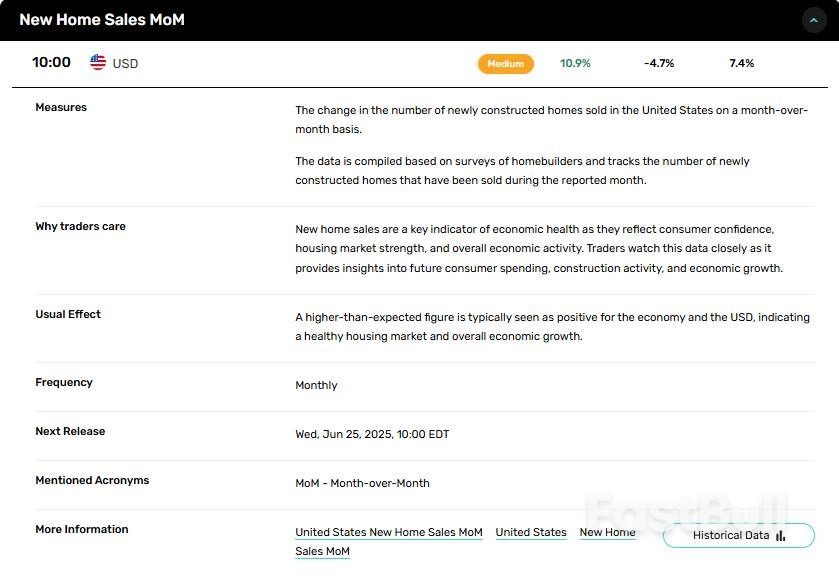

Exports are tumbling — they will drop 7.4% on an annualized basis in the current quarter, forecasters estimate, after President Donald Trump’s tariff threats caused US importers to pull forward their shipments earlier in the year. But exporters should be able stage a modest recovery, starting later in the year.

The trade dispute with Canada’s closest trading partner is hitting the labor market and household consumption. Economists now say unemployment will rise to 7.2% in the second half of the year before easing in 2026.

They expect inflation to run above the central bank’s target, at 2.1% in the third quarter and 2.2% in the fourth.

That puts the Bank of Canada in a difficult position, with now a less than 30% probability of a change to interest rates at its June meeting, according to Bloomberg’s World Interest Rate Probability.

“The more we can get uncertainty down, the more we can be more forward-looking as we move forward in our monetary policy decisions,” Bank of Canada Governor Tiff Macklem said on Thursday.

Businesses and consumers are waiting for more clarity on what the US relationship looks like before making major decisions. That uncertainty has contributed to a notable slowdown in the housing market, with home prices and sales falling. Economists say housing starts may be weaker in the second half of 2025 than in the second quarter.

“I know Canada is keen to sit down with the US and work through our differences and come to an agreement,” Macklem said. “If we can get that clarity, we can get back to growth. Clearly if things move in the other direction, yes, it will be worse.”

Prime Minister Mark Carney will get another chance to meet with Trump soon, with the US president set to make his first trip to Canada since returning to power when he attends the G-7 leaders’ summit in Alberta in June.

But Carney has warned that the long period of deepening integration between the two countries is over.

Economists see gross domestic product rising 1.2% in 2025 and 1% in 2026. Those figures are in line with the previous Bloomberg survey.

The survey of 34 economists was conducted from May 16 to May 21.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up