Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

A single word often makes a big difference in Chinese policy. In previous five-year economic development plans, for example, Beijing had always reiterated it wants to "prudently promote" yuan internationalisation. In an outline of the next 2026-2030 blueprint unveiled last month, the word "prudently" has been struck out.

A single word often makes a big difference in Chinese policy. In previous five-year economic development plans, for example, Beijing had always reiterated it wants to "prudently promote" yuan internationalisation. In an outline of the next 2026-2030 blueprint unveiled last month, the word "prudently" has been struck out. That signals bolder designs for the renminbi, though progress will be limited so long as economic planners keep tight control over capital flows.

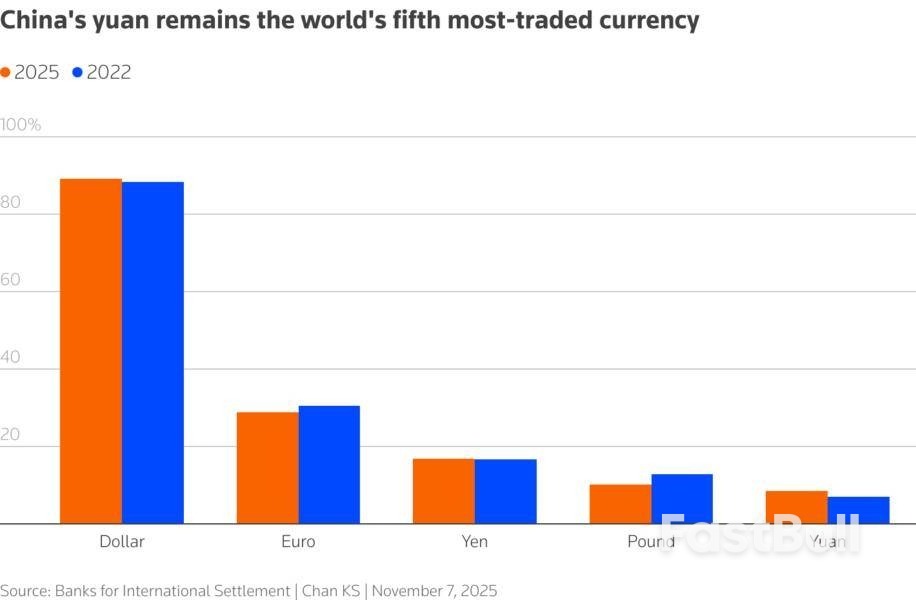

China's $20 trillion economy may be the second-largest in the world, but its currency was only the fifth most-traded last year, according to a September report from the Bank of International Settlements. Still, thanks to incremental policies, including currency swap deals with other central banks, the yuan now makes up 8.5% of global currency transactions, up from 7% in 2022.

For Beijing, trade settlement will probably be the next area of focus, given China's 15% share of $33 trillion of global trade by value. Notably, as part of a broader contract dispute, China's steel industry has stopped purchasing dollar-denominated iron ore from Australia's BHPsince October, according to Chinese media, citing sources, and has insisted the mining giant settle 30% of transactions in yuan going forward. Separately, Dutch chipmaker Nexperia's Chinese unit has demanded all transactions be settled in yuan, Reuters reported, citing sources, after The Hague seized control of the company's Netherlands-based parent in September, sparking a broader standoff.

These moves can have an immediate impact. Up to 12.4 trillion yuan ($1.7 trillion) of trade with China was paid in local currency last year, about 27% of the total, according to the country's central bank's yuan internationalisation report published last week. Settling 30% of imports from BHP can add another $39 billion worth of yuan-denominated transactions annually. And using renminbi will appeal to countries that want to reduce their reliance on the U.S. dollar. That includes Brazil and Russia, which exported $31 billion of soybeans and $50 billion of crude oil, respectively, to the People's Republic last year.

Chinese planners have long insisted that their plan is not to replace the greenback with a "redback". And it's unlikely they will allow the country's currency to flow freely across its borders. Still, Beijing's trade clout can help it chip away at the dollar's dominance.

Commodity news portal SteelOrbis reported on October 11 that BHP has agreed with China Mineral Resources Group to switch to yuan settlements for 30% of its spot ore trade with China, citing sources.

Separately, Dutch chipmaker Nexperia's Chinese unit has resumed supplying semiconductors to local distributors, but all sales to distributors must now be settled in yuan, Reuters reported on October 23, citing two people briefed on the matter.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up