Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Turkish Foreign Minister: We Hope Solution Can Be Found To Avoid Conflict And Isolation Of Iran

Turkish Foreign Minister: Spoke With USA Envoy Witkoff On Thursday, Will Continue Speaking To USA Officials On Iran

Iran's Araqchi Says Tehran Welcomes Talks With Regional Countries That Aims At Bringing Stability And Peace

Istanbul - Iran's Foreign Minister Araqchi Says Tehran 'Is Prepared For Resumption Of Talks With The US'

Istanbul - Iran's Foreign Minister Araqchi: Talks With His Turkish Counterpart Fidan Was Very 'Good And Useful'

Turkish Foreign Minister: Turkey Closely Following Integration Agreement Between Damascus-Sdf In Syria

Turkish Foreign Minister: Turkey Calling On US, Iran To Come To Negotiating Table To Resolve Issues

Turkish Foreign Minister: Turkey Opposes Foreign Intervention On Iran, We Tell Our Counterparts This

Turkish Foreign Minister: Iran's Peace And Stability Important For US, Turkey Saddened By Deaths During Protests

Chevron: Continue To Engage With The USA And Venezuelan Governments To Advance Shared Energy Goals

Japan Tokyo CPI YoY (Excl. Food & Energy) (Jan)

Japan Tokyo CPI YoY (Excl. Food & Energy) (Jan)A:--

F: --

P: --

Japan Retail Sales YoY (Dec)A:--

F: --

Japan Industrial Inventory MoM (Dec)A:--

F: --

P: --

Japan Retail Sales (Dec)A:--

F: --

P: --

Japan Retail Sales MoM (SA) (Dec)A:--

F: --

Japan Large-Scale Retail Sales YoY (Dec)A:--

F: --

P: --

Japan Industrial Output Prelim MoM (Dec)A:--

F: --

P: --

Japan Industrial Output Prelim YoY (Dec)A:--

F: --

P: --

Australia PPI YoY (Q4)

Australia PPI YoY (Q4)A:--

F: --

P: --

Australia PPI QoQ (Q4)A:--

F: --

P: --

Japan Construction Orders YoY (Dec)A:--

F: --

P: --

Japan New Housing Starts YoY (Dec)A:--

F: --

P: --

France GDP Prelim YoY (SA) (Q4)

France GDP Prelim YoY (SA) (Q4)A:--

F: --

P: --

Turkey Trade Balance (Dec)

Turkey Trade Balance (Dec)A:--

F: --

P: --

France PPI MoM (Dec)A:--

F: --

Germany Unemployment Rate (SA) (Jan)

Germany Unemployment Rate (SA) (Jan)A:--

F: --

P: --

Germany GDP Prelim YoY (Not SA) (Q4)A:--

F: --

P: --

Germany GDP Prelim QoQ (SA) (Q4)A:--

F: --

P: --

Germany GDP Prelim YoY (Working-day Adjusted) (Q4)A:--

F: --

P: --

Italy GDP Prelim YoY (SA) (Q4)

Italy GDP Prelim YoY (SA) (Q4)A:--

F: --

P: --

U.K. M4 Money Supply (SA) (Dec)

U.K. M4 Money Supply (SA) (Dec)A:--

F: --

U.K. M4 Money Supply YoY (Dec)A:--

F: --

P: --

U.K. M4 Money Supply MoM (Dec)A:--

F: --

P: --

U.K. Mortgage Lending (Dec)A:--

F: --

U.K. Mortgage Approvals (Dec)A:--

F: --

Italy Unemployment Rate (SA) (Dec)A:--

F: --

P: --

Euro Zone Unemployment Rate (Dec)

Euro Zone Unemployment Rate (Dec)A:--

F: --

P: --

Euro Zone GDP Prelim QoQ (SA) (Q4)A:--

F: --

P: --

Euro Zone GDP Prelim YoY (SA) (Q4)A:--

F: --

P: --

Italy PPI YoY (Dec)A:--

F: --

P: --

Mexico GDP Prelim YoY (Q4)

Mexico GDP Prelim YoY (Q4)--

F: --

P: --

Brazil Unemployment Rate (Dec)

Brazil Unemployment Rate (Dec)--

F: --

P: --

South Africa Trade Balance (Dec)

South Africa Trade Balance (Dec)--

F: --

P: --

India Deposit Gowth YoY

India Deposit Gowth YoYA:--

F: --

P: --

Germany CPI Prelim YoY (Jan)--

F: --

P: --

Germany CPI Prelim MoM (Jan)--

F: --

P: --

Germany HICP Prelim YoY (Jan)--

F: --

P: --

Germany HICP Prelim MoM (Jan)--

F: --

P: --

U.S. Core PPI YoY (Dec)

U.S. Core PPI YoY (Dec)--

F: --

P: --

U.S. Core PPI MoM (SA) (Dec)--

F: --

P: --

U.S. PPI YoY (Dec)--

F: --

P: --

U.S. PPI MoM (SA) (Dec)--

F: --

P: --

Canada GDP MoM (SA) (Nov)

Canada GDP MoM (SA) (Nov)--

F: --

P: --

Canada GDP YoY (Nov)--

F: --

P: --

U.S. PPI MoM Final (Excl. Food, Energy and Trade) (SA) (Dec)--

F: --

P: --

U.S. PPI YoY (Excl. Food, Energy & Trade) (Dec)--

F: --

P: --

U.S. Chicago PMI (Jan)--

F: --

Canada Federal Government Budget Balance (Nov)--

F: --

P: --

Brazil CAGED Net Payroll Jobs (Dec)--

F: --

P: --

U.S. Weekly Total Oil Rig Count--

F: --

P: --

U.S. Weekly Total Rig Count--

F: --

P: --

China, Mainland NBS Manufacturing PMI (Jan)

China, Mainland NBS Manufacturing PMI (Jan)--

F: --

P: --

China, Mainland NBS Non-manufacturing PMI (Jan)--

F: --

P: --

China, Mainland Composite PMI (Jan)--

F: --

P: --

South Korea Trade Balance Prelim (Jan)

South Korea Trade Balance Prelim (Jan)--

F: --

Japan Manufacturing PMI Final (Jan)--

F: --

P: --

South Korea IHS Markit Manufacturing PMI (SA) (Jan)--

F: --

P: --

Indonesia IHS Markit Manufacturing PMI (Jan)

Indonesia IHS Markit Manufacturing PMI (Jan)--

F: --

P: --

China, Mainland Caixin Manufacturing PMI (SA) (Jan)--

F: --

P: --

Indonesia Core Inflation YoY (Jan)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

China cuts whisky tariffs to 5%, a significant boon for UK exporters amid renewed diplomatic engagement.

China is set to cut its import tariff on whisky in half, a significant move that provides a major boost to the British whisky industry. The tariff will be lowered from 10% to 5%, with the new rate taking effect on February 2.

This decision comes directly after high-level talks between British Prime Minister Keir Starmer and Chinese President Xi Jinping, aimed at repairing diplomatic ties and strengthening economic cooperation.

The reduction is expected to deliver substantial financial benefits for UK-based exporters. According to the British Prime Minister's office, the deal is valued at approximately £250 million ($344.13 million) over the next five years.

The UK is the dominant player in China's whisky market. Customs data from 2025 shows that China imported $445.5 million worth of whisky, with a staggering 84% of that total originating from the United Kingdom. This market share underscores why the tariff adjustment is a critical win for the Scotch whisky sector.

The tariff change marks a reversal of a recent effective rate hike. While Beijing had previously set a provisional tariff of 5% on whisky in 2017, this provision was removed for 2025, causing the rate to revert to 10%. The new policy reinstates the lower 5% tariff.

The agreement was a key outcome of discussions between Starmer and Xi in Beijing. Beyond whisky tariffs, the two leaders also committed to pursuing greater cooperation in the broader fields of trade, investment, and technology.

The Spanish economy finished 2025 with significant momentum, posting 0.8% quarter-on-quarter growth in the final three months. This performance marked an acceleration from the 0.6% expansion seen in the third quarter and outpaced consensus forecasts by 0.2 percentage points.

While a minor downward revision to first-quarter data adjusted the full-year growth for 2025 to 2.6%, the key takeaway is clear: Spain entered 2026 on solid footing, powered by strong domestic demand.

The drivers behind the strong Q4 performance followed a familiar pattern. Household consumption was a major contributor, rising by a robust 1.0% for the third consecutive quarter. Investment also expanded by 1.7%, bolstered by a 2.7% surge in intellectual property investment.

However, the picture was not uniformly positive. Government consumption remained largely flat, and net exports continued to be a drag on growth, reflecting a difficult global economic environment.

From a production standpoint, all major sectors grew, but their trends diverged. Manufacturing output slowed for the second quarter in a row, expanding by just 0.1%. According to S&P Global PMI data, this weakness stems from declining output and shrinking order books amid intense competitive pressure. This trend contrasts with yesterday's more optimistic economic sentiment indicators, which appear to overlook the sharp drop in reported export orders.

In contrast, the services sector continued its robust expansion, although signs of a slowdown in tourism are becoming more visible. After several years of standout performance, growth in the tourism sector is expected to normalize.

The economic forces that shaped late 2025 will continue to guide Spain’s outlook in 2026. Growth is expected to normalize as several key drivers moderate.

• Government Consumption: With no new budget in place, government spending is expected to make a limited contribution.

• Private Consumption: After several quarters of strong growth, consumer spending is forecast to gradually return to a more normal pace.

• Net Exports: External demand is likely to remain subdued, partly due to a stronger euro. The real effective exchange rate of the euro has climbed 6.1% since January 2025, weighing on exports.

With other growth engines moderating, investment will become the critical factor for Spain's economy in 2026. Much of the country's recent growth has been quantitative, driven by an expanding labor force through migration. The government's plan to grant legal status to approximately 500,000 people—about 2% of the current legal labor force—continues this strategy. While this move offers social and labor market benefits, its macroeconomic impact may be more limited than previous labor supply expansions.

Meanwhile, a decline in productivity per hour worked in Q4 2025 highlights an urgent need for productivity-enhancing investments to foster more sustainable, structural growth.

A major source of potential upside comes from the EU Recovery and Resilience Facility (RRF). Spain has roughly €20 billion in RRF grants to disburse by the end of 2026, equivalent to about 6% of its annual investment spending. Favorable conditions for private investment also exist, with capacity utilization rising to 79.8% in Q4 2025. While the effects of these investments may not be immediate, they could initiate a gradual shift toward higher-quality, more productive growth, helping Spain continue to outperform its eurozone peers.

Reflecting these dynamics, our 2026 growth forecast has been revised upward to 2.4%, though this is primarily due to the strong carry-over from Q4 2025 rather than a change in the underlying quarterly growth profile.

Inflation data from January also points toward normalization. At 2.5% year-on-year, the figure was slightly higher than expected but still represented a 0.5 percentage point drop from December 2025. This decrease was driven by a 0.7% month-on-month fall in prices, largely due to a more moderate rise in electricity costs compared to the previous year. This data reinforces the broader trend of both the Spanish economy and its inflation profile returning to a more stable pattern.

AUDUSD extended rally for nearly two weeks and hit three-year high on Thursday (0.7093), before easing.

Weakening US dollar and Aussie tracking strong rise in precious metals, were mainly behind the latest rally (up over 6% since the move started on Jan 19).

Bulls broke and established above psychological 0.70 level, but faced strong headwinds on approach to 0.7100 resistance, as daily studies are overbought and overstretched 14-d momentum turned south.

Thursday's red daily candle with long upper shadow adds to signals of upside rejection and warning of pullback, as the US dollar jumps after steep fall in past four days.

Loss of initial supports at 0.70 zone (psychological / near Fibo 23.6% of 0.6667/0.7093) unmasks 0.6930 (Fibo 38.2%), with stronger acceleration lower to find solid ground at 0.6900/0.6880 zone (round-figure / 50% retracement) and mark a healthy correction before larger bulls regain control.

Caution on potential loss of 0.6880 handle, which may trigger deeper pullback and sideline bulls.

Res: 0.7015; 0.7093; 0.7157; 0.7207Sup: 0.6968; 0.6930; 0.6880; 0.6830

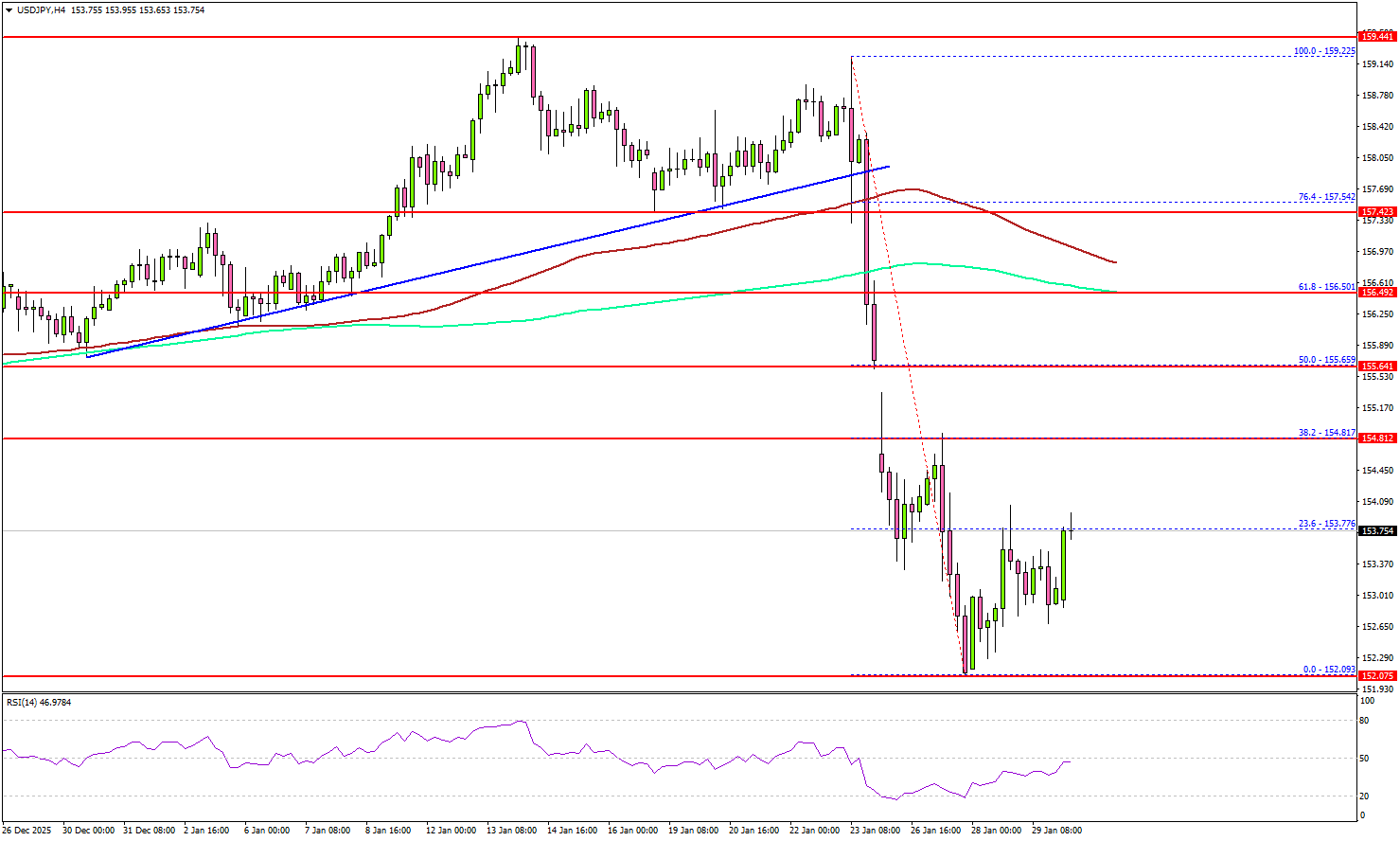

The US Dollar started a major decline below 158.00 against the Japanese Yen. USD/JPY settled below 157.00 to enter a bearish zone.

Looking at the 4-hour chart, the pair traded below a key bullish trend line with support at 158.00 to start the recent downtrend. It settled below 156.50, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour).

Finally, the pair dived below 153.50 and tested 152.00. A low was formed at 152.09, and the pair is now consolidating losses. Immediate resistance sits near 153.75.

The first key hurdle could be 154.00. The next stop for the bulls might be 154.80, where they could face hurdles. A close above 154.80 could open the doors for more gains. In the stated case, the bulls could aim for a move toward 156.50 and the 200 simple moving average (green, 4-hour).

If there is a fresh decline, the pair might find support near 152.40. The first major area for the bulls might be near 152.00. The main support sits at 150.00, below which the pair could accelerate lower. The next support could be 146.50.

Looking at EUR/USD, the pair extended gains and traded above 1.2000 before the bears appeared and pushed the pair to 1.1950.

We're coming toward the end of a geopolitically calm-ish week — no major threats, no major events — but with rising volatility in the metals markets. Yesterday was again marked by a strong rally in gold, silver and copper prices, followed this time by a sharp selloff.

Note that the impressive rally in LME copper was triggered by intense speculative trading in China. So metals markets are fuming right now.

Gold is down to around $5'230 per ounce at the time of writing after flirting with the $5'600 level at yesterday's peak. That's insane considering the week started near $5'000. And what was just as insane was the sharp selloff that followed. Gold wiped out around $2.5 trillion in market value in just 30 minutes, sending prices from above $5'500 to around $5'100.

Silver also traded past $121 an ounce before pulling back sharply, and is down again in Asia this morning — same story for copper.

Are we surprised? No, we're not. Price action in metals was impressive, but it could be expected just by looking at the rising stress through the lens of the gold volatility index.

A major spike there has been telling us a lot about the building stress behind such an impressive rally, which lately became driven more by speculation than fundamentals. That means we could see a meaningful pullback of 8–10%, toward the $4'600–4'800 per ounce range, to relieve some of that stress.

Price pullbacks, however, will likely be seen as opportunities to strengthen long positions, as the major drivers of the metals rally — unsustainable-but-still-rising G7 debt, waning appetite for the US dollar, trade and geopolitical uncertainties, the search for supranational assets able to preserve value in case of further geopolitical chaos, and potentially rising price pressures — remain fully in play.

Tensions between the US and Iran these days don't only push oil prices higher — US crude briefly spiked past $66 per barrel yesterday — they also point to potential disruptions in major trade routes in the region. So, demand for hard commodities and safe-haven assets is certainly not over. That said, a correction looks healthy at these strongly overbought levels.

Voilà — that's the take on metals: bullish in the longer run, cautious in the short run. Any geopolitical headline could disrupt the correction process and trigger a premature return to metals.

In currencies, the US dollar is consolidating early-week losses near four-year low levels. The USDJPY is unsurprisingly rising again and likely has room to run toward levels that would make Japanese authorities uncomfortable — namely the 160 level. The EURUSD is struggling as well, having failed to hold above 1.20.

Something notable happened this week: large bets were placed via Euribor options expiring in March and June, betting on a 25bp ECB rate cut before summer. That's clearly a contrarian trade, as markets are pricing a 25bp cut this year with 25% chance only. But it also suggests some investors are preparing for US-EU relations to worsen before improving, and for European economies to require ECB support.

What's sure is that, with or without stabilization in US relations, EU governments will likely have to deliver on defence and technology spending, implying meaningful fiscal support.

And we all know what the sweet combination of expansive fiscal and monetary policy means for equity markets: gains. As a result, stimulus expectations keep the Stoxx outlook positive, with defence names the first-line beneficiaries of fiscal flows.

Note that the Stoxx 600 fell yesterday, alongside major US peers. One of Europe's biggest tech names, SAP, tanked 16% after reporting disappointing earnings — notably a lower-than-expected cloud backlog, meaning revenues already committed by customers for future cloud services but not yet recognized. SAP said negotiations took longer than expected and that AI tools should eventually drive customer migration from on-premise servers to the cloud. That narrative hasn't convinced investors so far: the stock is down more than 40% since February 2025. Whether this is an opportunity or whether SAP's AI push turns into a flop remains to be seen.

In the US, Microsoft also had an ugly day — a very ugly one, its worst since the DeepSeek-triggered Nvidia selloff last year. Shares dropped around 10%, rebounding from a critical technical level near $423, corresponding to the 38.2% Fibonacci retracement of the past three-year AI rally.

That level matters: a break below would signal an end to the bullish trend and a return to a bearish consolidation zone, opening the door to deeper losses. If it holds however, the latest dip could offer an entry point for buyers at a more reasonable valuation than two months ago. It all comes down to whether massive AI spending is matching demand.

Microsoft's latest earnings warned of slowing cloud revenue, triggering yesterday's selloff. But is the slowdown temporary? Big Tech continues to pour money into AI infrastructure, AI companies and AI models — and all that data has to be stored somewhere. The question is: where?

Finally, a company that clearly missed the AI turn: Apple. Apple is nowhere to be found in the AI race. It has invested far less than peers, has no AI model, and opted instead to rely on Google's Gemini.

That didn't stop Apple from delivering strong holiday-quarter sales, which initially pushed the stock higher post-earnings in after-hours trading. But appetite faded quickly as investors worried that rising memory-chip prices could squeeze margins, regardless of Apple's pricing power.

On the other side of the memory-chip trade, SK Hynix is up again — nearly 7% at the time of speaking. European futures are higher, US futures lower, reinforcing the idea that the rotation from US to non-US markets may continue into the weekly close.

And next week — it's a new week.

In the euro area, we receive the first January inflation reports from Germany and Spain. Euro area inflation is expected to decline to 1.7% y/y from 1.94% y/y in December, driven by significant energy base effects despite higher energy prices in January. However, numerous one-offs and policy changes influencing the data warrant a more cautious interpretation than usual.

We also get the first estimate of euro area GDP for Q4 2025, which is likely to show that the euro area ended the year on a solid growth momentum, with strong PMIs for Q4. Preliminary GDP release from Germany showed growth of 0.2% q/q as industrial activity rebounded. Combining these pieces of information, we expect the euro area Q4 GDP growth will come in at 0.3% q/q. We also get the unemployment rate for December which we expect to show a stable unemployment rate of 6.4%.

In the US, the delayed December PPI report is due, following CPI data that came in slightly below expectations. Senate Democrats have slowed progress on the appropriations bill to fund the government. If unresolved today, a partial shutdown could occur, though such situations are often resolved last minute.

In Norway, December retail sales are released. After rising 1.3% in November, we estimate a 0.5% decline in December, partly due to seasonal adjustment issues related to Black Week shifting Christmas trade.

In Sweden, focus turns to December retail sales and November wage growth. Retail sales likely declined in December after November's sharp rise driven by Black Week shopping. Wage growth remains steady at 3.6% y/y and is expected to hold.

In China, the official PMI data from NBS will be released on Saturday. Manufacturing PMI rebounded above the 50-mark in December, and we expect it to remain broadly stable in January, supported by strong exports.

What happened overnight

In the US, Donald Trump announced that he will name a replacement for Jerome Powell as Chair of the Fed today, 30 January. There is significant focus on whether the pick would be more dovish and in alignment with Trump's administration. The shortlist reportedly includes Kevin Warsh, Kevin Hasset, Christopher Waller and Rick Rieder. While Rieder had been leading predictions in recent days, betting markets shifted yesterday, with Warsh now considered the favourite, holding a 92% probability on Polymarket.

Oil prices have increased lately with Brent crude benchmark trading at USD 69.75 this morning, after briefly reaching USD 70.75 overnight. The increase has been driven by weaker USD and markets increasingly pricing in a geopolitical risk premium, as tensions continue to build up in Iran. Yesterday, the EU agreed to hit Iran with sanctions, including the designation of its Islamic Revolutionary Guard Corps as a terrorist organisation. Additionally, overnight, Donald Trump signed an executive order to establish a process for imposing tariffs on goods from countries that supply oil to Cuba.

What happened yesterday

In Norway, the unemployment rate (SA) from NAV surprised by falling to 2.1% in December, despite a clear downward trend in employment throughout Q4. While a slight drop in the labour force contributed, it cannot fully explain the decline. Our seasonal adjustment shows that unemployment was approximately 2.15% in both November and December, so that most of the fall was due to rounding. For January, we expect the unemployment rate (SA) to remain unchanged at 2.1%, with a risk that it will rise to 2.2%.

In Sweden, the Riksbank left the policy rate unchanged at 1.75%, as widely expected. The Riksbank reiterated that "the rate is expected to remain at this level for some time to come", as it assesses that the current rate supports economic activity strengthening and stabilizes inflation around the target over the longer term. For more details, see Riksbank review: January 2026, 29 January. Meanwhile, the NIER survey weakened slightly but remained solid, with minor changes from the previous month. Household sentiment continues to drag the indicator lower, while the corporate outlook remains strong. Notably, recent hard data shows a pickup in consumption.

In Germany, data from the Ministry of Finance showed that public investments fell 25% short of the target in 2025. Total public investments amounted to EUR 86.8bn in 2025 which was 17% higher than in 2024 but at the same time 25% below the targeted EUR 115.6bn. Defence expenditures amounted to EUR 87.0bn in 2025 which was 18% more than in 2024 but 7% short of the EUR 94.0bn target. The failure to reach the targets is a slightly dovish signal for the ECB but not enough to cause a rate cut in 2026 as there is still a large increase in spending. For details, see German Fiscal Tracker, 29 January.

In the US, the Chicago Fed's latest unemployment rate 'nowcast' signals a potential dip to 4.3% in the upcoming January Jobs Report. High-frequency data has been generally positive as jobless claims continue to decline, ADP's weekly data indicates jobs growth during the reference period, and online job postings have modestly increased.

Equities: Thursday saw a reversal of some of this week's key trading themes. First, tech underperformed sharply, driven by Microsoft (-10%), with other software stocks also suffering, such as Zscaler and Strategy Inc. Semiconductors, however – which have been the outperformers lately – held up well in what was largely a software-related selloff. It is also worth adding that Meta jumped 10%. This was therefore not a broad-based tech selloff like last quarter, when AI capex was in focus. Again, remember that the previous tech selloff did not coincide with earnings reports but occurred a week later, so it is too soon to draw broad conclusions. As our readers know, we prefer riding the AI wave through Asia (the Kospi is up another 1% this morning) while remaining neutral on the global tech sector.

FI and FX: EUR/USD slid through the night and is currently trading in the low 1.19's. NOK had a strong first half of yesterday's session, under a lot of volatility. As SEK trading was muted on the back of an undramatic Riksbank, with the Swedish Krona holding steady we saw NOK/SEK edge higher through the day. The sharp rally in the oil market continued yesterday, with Brent trading at the highest levels since last summer. Yesterday also saw wild swings in the metals space, with copper rising 11% whilst the price of Gold saw a sudden and dramatic fall at 16:00 CET, before eventually recouping some of the losses. Finally, reports have it that Kevin Warsh is likely to be Trump's nominee as the next Fed chair, due to be announced today.

Key insights from the week that was.

In Australia, all eyes were on the Q4 CPI print ahead of next week's RBA decision. In the event, inflation printed above our expectations on both a headline and trimmed mean basis, rising 0.6%qtr / 3.6%yr and 0.9%qtr / 3.4%yr respectively. There were a number of subplots in the detail: strong seasonal demand for domestic holiday travel (9.6%yr), rising gold and silver prices boosting accessories (11.4%yr), and rebate-driven volatility in electricity prices (21.5%yr). Policy changes and administered price increases also buoyed inflation across childcare, education, water rates and property charges. There was some evidence of disinflation too, mainly in home-building costs and rents where inflation looks to have peaked. Overall though, it appears services inflation remains 'sticky' well above target (4.1%yr) and that goods inflation is no longer providing a disinflationary offset (3.4%yr).

Following the CPI report, Chief Economist Luci Ellis issued a change of rate call, with Westpac now anticipating the RBA to lift the cash rate by 25bps to 3.85% at next week's meeting. The RBA laid the groundwork for such a move in their communications over recent months in case of an upside surprise; and with two disappointing quarterly prints now received, there is little reason wait. How the policy outlook will evolve beyond February is set to depend on the response to the change in policy expectations and the economy's capacity, particularly labour market participation. The RBA's updated forecasts will shed more light on their baseline expectations and view of key risks; they are likely to continue to hold a relatively conservative view on supply and a cautious approach to communicating on the policy outlook.

The latest NAB business survey meanwhile reported a solid finish to 2025, the conditions and confidence indexes edging higher in December, consistent with other evidence of strengthening consumer demand. That said, the future path for inflation and interest rates is a clear threat to confidence in early-2026. Worthy of note too, perspectives differ across industries. In our latest Quarterly Agriculture Report, we discuss prospects for farm GDP following a bumper 2025.

In the US, the FOMC maintained its monetary policy stance at the January meeting as expected in a 10-2 vote, with Miran and Waller preferring to cut the fed funds rate by 25bps. The Committee's assessment of the economy was positive for growth (characterising it as "solid") notwithstanding weakness in housing; sanguine on the labour market ("the unemployment rate has shown some signs of stabilization") despite job gains having "remained low"; and cautious on inflation ("remains somewhat elevated").

The characterisation of risks was balanced, the statement simply noting that "Uncertainty about the economic outlook remains elevated", the "Committee is attentive to the risks to both sides of its dual mandate" and "prepared to adjust the stance of monetary policy as appropriate". In the press conference, Chair Powell made it clear that policy will be determined on a meeting-by-meeting basis on incoming data and did not show material concern over the potential evolution of conditions. Instead, risks were judged to have diminished.

Recent weakness in the US dollar was a key topic during the Q&A. Chair Powell made clear market movements do not dictate monetary policy, nor does the FOMC seek to manage the currency, with full employment and inflation-at-target their mandated focus. Chair Powell did not comment on recent tensions between the Administration and the Federal Reserve but took the opportunity to affirm the long-standing success of central bank independence and monetary / fiscal collaboration globally.

We expect one further cut from the FOMC in March to mitigate the lingering downside risks the labour market faces. But if activity growth proves stronger than expected at the beginning of 2026, the FOMC may skew their focus towards inflation risks, holding off on a further reduction in the fed funds rate.

Further north, the Bank of Canada also kept rates steady at 2.25%, maintaining an accommodative stance to support the economy as it navigates excess capacity and trade uncertainty. Governor Macklem noted that the "current policy rate remains appropriate, conditional on the economy evolving broadly in line with the [forecast] outlook …The Canadian economy is adjusting to the structural headwinds of US protectionism…[and] uncertainty makes it difficult to predict the timing or direction of the next change in the policy rate." We anticipate the Council will keep policy accommodative while headwinds persist.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up